Fixed Income in Focus:

The week opened on a cautious note despite supportive liquidity, with bonds initially trading bearish as mid-tenors weakened ahead of the NTB auction. Sentiment in the bond space turned bullish mid-week, with demand concentrated across the 2031s–2035s and yields compressing by c.5–9bps into the latter sessions.

In the T-bills segment, activity was mixed early on, as participants positioned ahead of the auction. The newly issued 364-day bill later cleared 5bps lower on a robust 4.06x bid-to-cover, driving bullish post-auction flows, with the 06-May bill settling around 16.00/15.90%.OMO activity was initially muted, despite the CBN’s early-week auction, where the 134-day paper cleared at 19.97% on a 2.13x bid-to-cover. Flows firmed into the close, with Sept papers compressing c.7–10bps. Liquidity stayed supportive, peaking at c.₦6.96tn before closing at c.₦5.67tn.

Nigerian Equities:

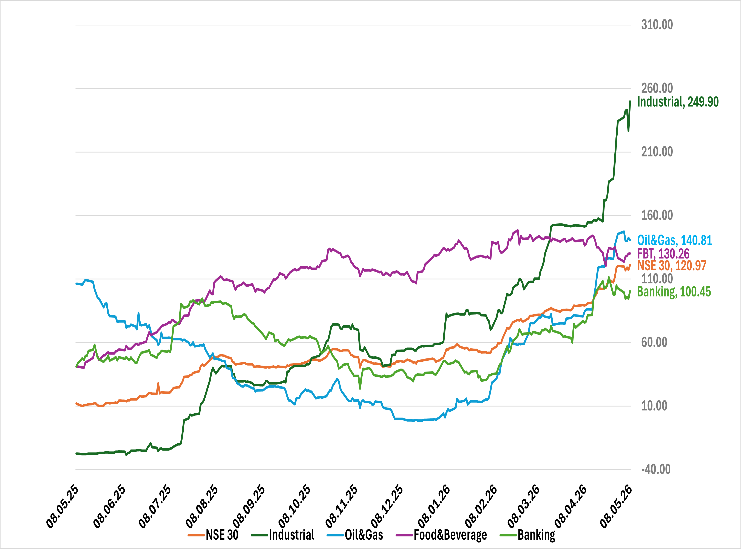

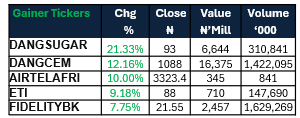

The ASI advanced 1.03% WoW, extending the market’s positive momentum. Industrials led gains while Oil & Gas lagged on profit-taking; Banking and Food & Beverage also closed positive. The move was supported by continued strength in DANGCEM and DANGSUGAR, while market sentiment remained underpinned by ongoing Q1 earnings.

NTB Auction Result

| 91-day | 182-day | 364-day | |

| Sales (₦‘bn) | 63.579 | 67.677 | 600.493 |

| Stop Rates | 115.949% | 16.14% | 16.15% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.80 | 16.80 | – |

| May-33 | 16.85 | 16.80 | 5 |

| Feb-34 | 16.70 | 16.65 | 5 |

| Jan-35 | 16.85 | 16.60 | 25 |

| Jun-53 | 14.80 | 14.83 | (3) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 06-May-27 | 15.90 | 15.90 | 18.87 |

| 22-Apr-27 | 16.05 | 15.90 | 18.73 |

| 18-Feb-27 | 16.10 | 16.20 | 18.54 |

Indices Watch 1-Yr Performance %

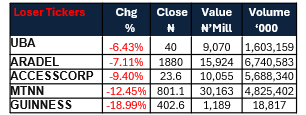

NSE 30 : Gainers and Losers

The Week Ahead…

The week is set against no scheduled primary market auction, with expected inflows of c.₦1.3tn from coupons on the 19.89% May 2033s and NGOMO maturities supporting liquidity. Attention turns to Friday’s CPI inflation print, with market activity likely to be shaped by early positioning ahead of the data release and expectations of a possible CBN OMO auction.

We expect ongoing Q1 earnings releases to remain the primary market driver for equities, particularly across banking and industrial names .However, recent weakness in Oil & Gas suggests profit-taking may persist in previously outperformed counters, keeping positioning selective across sectors.