Fixed Income in Focus:

The market opened the week with a surplus of c.₦8.15tn amid mixed activity across segments. The money market saw mild early-week demand for T-bills, with participants positioning ahead of the scheduled auction, compressing yields slightly. Auction stops cleared c.19bps below previous levels on the long end (364-day), attracting strong demand (13.63x bid-to-cover). Post-auction, demand strengthened, with yields c.38bps lower as flows settled at 16.05%. OMO bills witnessed two auctions in the week — (8 & 113-day) and (33, 75 & 96-day) — both attracting duration-focused demand and trading bullish into the close.

In the capital market segment, FGN bonds were largely offered, as participants took profit and positioned ahead of next week’s auction, with activity concentrated in the mid-tenor segment (32s, 33s, 34s, and 35s). Overall, executions printed around 16.15%, while liquidity remained firm to close at c.₦5.93tn

Nigerian Equities:

The ASI declined 0.12% WoW to close at 201,913.00, sustaining consolidation above the 200,000 level. Oil & Gas and Insurance led gains +1.93% and +2.22% respectively, while Banking lagged at -2.47%. The market traded mixed with profit-taking in energy and consumer names, while flows rotated into tier-1 banks on positioning ahead of earnings.

NTB Auction Result

| 91-day | 182-day | 364-day | |

| Sales (₦‘bn) | 97.752 | 28.044 | 394.875 |

| Stop Rates | 15.95% | 16.42% | 16.43% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.05 | 16.30 | (25) |

| May-33 | 16.05 | 16.30 | (25) |

| Feb-34 | 15.95 | 16.15 | (20) |

| Jan-35 | 15.95 | 16.22 | (27) |

| Jun-53 | 14.45 | 14.70 | (35) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 25-Mar-27 | 16.05 | 16.05 | 19.08 |

| 18-Mar-27 | 16.15 | 16.10 | 19.08 |

| 11-Feb-27 | 16.45 | 16.10 | 19.01 |

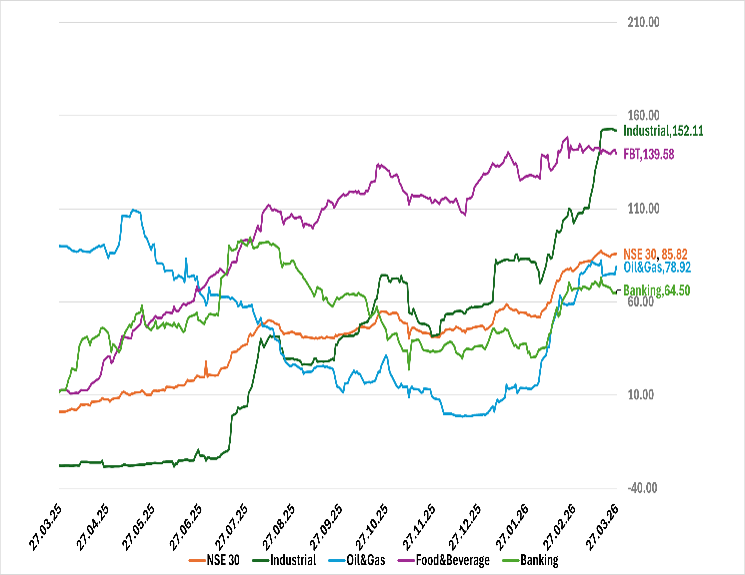

Indices Watch 1-Yr Performance %

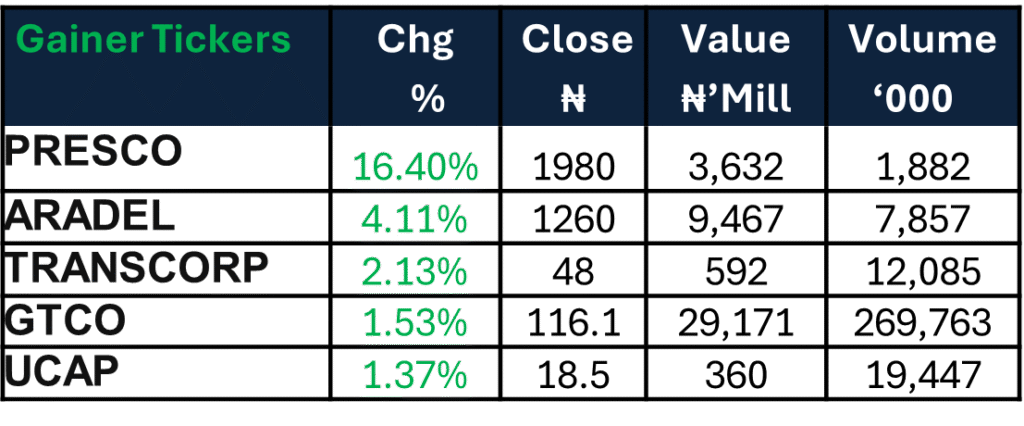

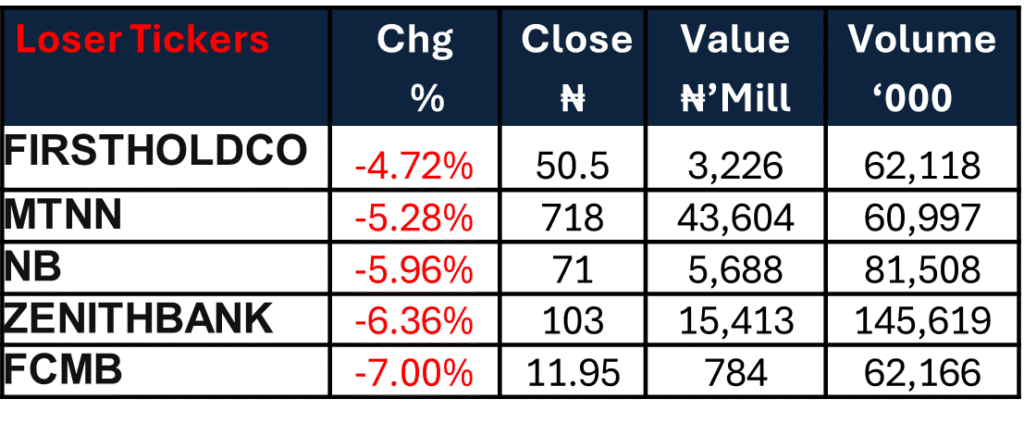

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens ahead of a scheduled FGN bond auction, where the DMO plans to issue ₦750bn across re-opened papers (30s, 32s, and 33s), set against c.₦1.019tn OMO maturities. Despite the liquidity backdrop, the bearish secondary market tone is expected to persist, with auction stops likely to clear c.15bps above secondary levels, implying marginal prints across papers in the 16.25%–16.55% range.

For equities, we expect flows to remain selective, with attention on results from tier-1 banks to guide direction. While energy names may retain support, banking weakness and softer breadth suggest continued consolidation, with follow-through dependent on earnings outcomes and sustained liquidity.