Fixed Income in Focus:

The market opened the week with a surplus of ₦7.12tn, as activity remained mixed across segments, with attention on the bond auction. The auction cleared bearish across tenors, with the 2033s attracting the bulk of demand (1.39x bid-to-cover) and trading slightly firmer post-auction, while the 2032s (1.09x bid-to-cover) and 2030s (1.01x bid-to-cover)weakened into the close. In the T-bills segment, activity was mixed, with flows concentrated on the March maturities, closing around 16.00%–16.10%.

OMO activity featured two short-dated auctions — 70/140-day and 75/138-day offers — as demand remained skewed to the longer tenors (bid-to-cover: 0.22x/4.11x and 0.12x/4.82x). Stop rates printed within the 19.90%–19.92% range, with the 138-day clearing at 19.91%, while the shorter tenor in the latter auction saw no sale. Overall, demand remained skewed to the long end, driving a firm close, with liquidity closing in surplus at c.₦5.4tn.

Nigerian Equities:

The ASI advanced 0.39% WoW, reflecting modest gains in a holiday-shortened week. Banking (+0.71%) provided support alongside Oil & Gas (+0.02%), while Insurance (-4.25%) lagged. Market activity remained subdued, with selective positioning across large caps and limited follow-through in prior out performers.

Bond Auction Result

| Aug 2030s | Jun 2032s | May 2033s | |

| Sales (₦‘bn) | 88.797 | 63.997 | 332,706 |

| Stop Rates | 16.00% | 16.15% | 16.64% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.30 | 16.40 | (10) |

| May-33 | 16.30 | 16.40 | (10) |

| Feb-34 | 16.15 | 16.25 | (10) |

| Jan-35 | 16.22 | 16.30 | (8) |

| Jun-53 | 14.70 | 15.00 | (30) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 25-Mar-27 | 16.05 | 16.00 | 18.93 |

| 18-Mar-27 | 16.10 | 16.05 | 18.93 |

| 11-Feb-27 | 16.10 | 16.05 | 18.86 |

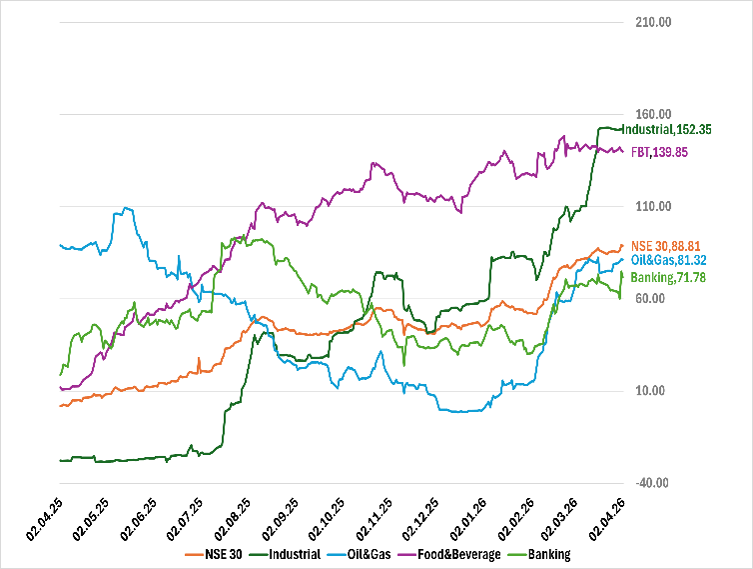

Indices Watch 1-Yr Performance %

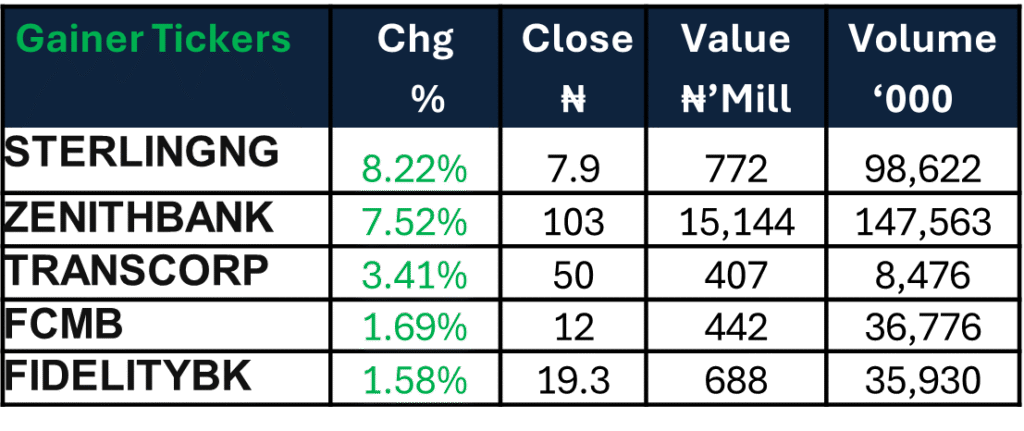

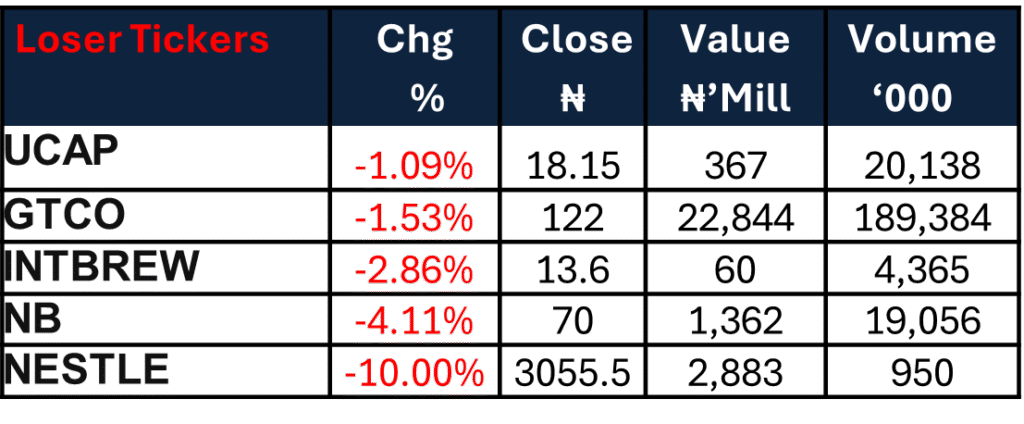

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens ahead of a scheduled Treasury bill auction, with the DMO set to issue ₦700bn against ₦356bn maturing. Liquidity is expected to remain supportive, driven by an expected ₦2.79tn in OMO maturities. In the absence of key macro data, activity in the week is likely to be guided by the auction outcome and investor positioning around it.

For the equities market, We expect selective bargain hunting to persist in quality names, while profit-taking may continue to cap upside in extended counters, keeping flows rotational rather than directional in the near term.