Fixed Income in Focus:

The fixed income market opened the shortened four-day trading week on a bearish note, with Friday declared a public holiday for Democracy Day. Sell pressure was sustained across bonds and treasury bills, particularly around the belly and long end of the curve, with bearish momentum peaking on Tuesday as benchmark bonds backed up by as much as 20–23bps. Sentiment improved from Wednesday, with selective demand returning across long-tenor NTBs and benchmark bonds, driving a mild recovery into Thursday’s close.

In the OMO segment, activity was initially subdued but improved slightly post-auction, with newly issued papers quoted around 19.95/19.80 and the 20-Oct paper trading with a slight bullish tilt.

Overall, despite the late-week recovery, the market closed the shortened week broadly bearish, with yields still higher across most benchmark bonds and treasury bills compared with Monday’s opening levels.

Nigerian Equities:

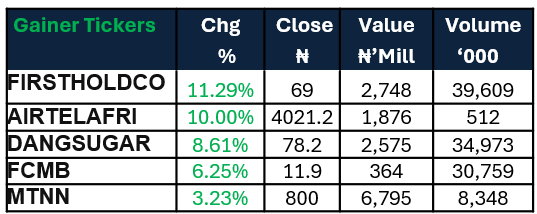

The ASI advanced 0.56% WoW to close at 244,738.74, extending the market’s positive momentum. Insurance led gains (+1.63%), followed by Banking (+0.96%). The advance was driven by strong buying interest in AIRTELAFRI (+10.00%), FIRSTHOLDCO (+11.29%), MTNN (+3.23, supporting the benchmark despite mixed sector performance.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 17.30 | 17.40 | (10) |

| May-33 | 17.30 | 17.40 | (10) |

| Feb-34 | 17.25 | 17.40 | (15) |

| Jan-35 | 17.30 | 17.50 | (20) |

| Apr-37 | 17.30 | 17.40 | (10) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 03-Jun-27 | 16.20 | 16.44 | 19.56 |

| 22-Apr-27 | 15.60 | 15.90 | 18.40 |

| 07-Jan-27 | 16.30 | 16.50 | 18.20 |

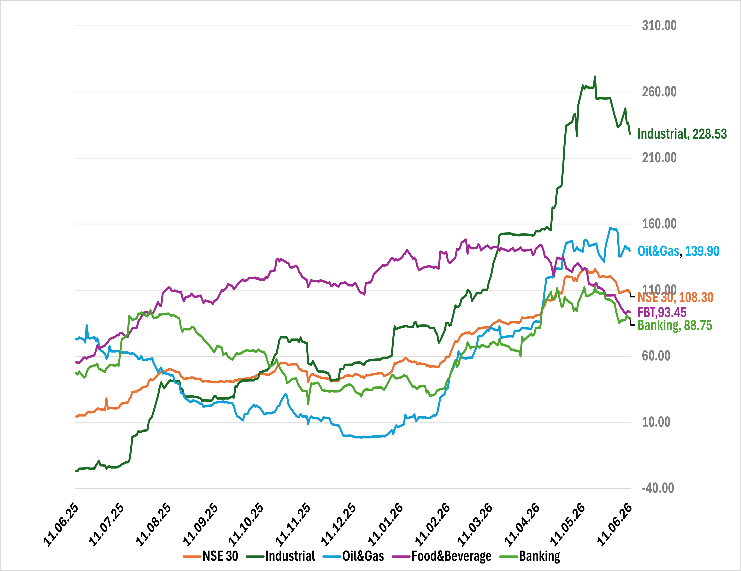

Indices Watch 1-Yr Performance %

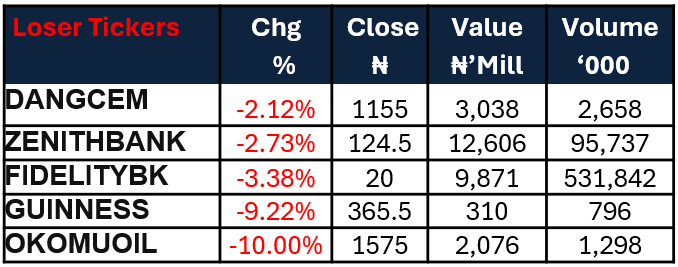

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens with focus on Monday’s CPI inflation print, ahead of the mid-week Treasury bill auction where the DMO is scheduled to offer ₦1.0tn against about ₦185bn in maturities. Liquidity should remain supported by ₦2.96tn in inflows from maturing OMO bills and coupon payments on the FGNSK Jun-2027s. Activity this week will be dictated by the CPI outcome and the result at the auction.

For equities , We expect investors to remain selective, focusing on fundamentally strong names following the recent moderation in prices, while market direction remains dependent on the sustainability of flows into large-cap names.