Fixed Income in Focus:

The fixed income market traded on a bearish note through the week, shaped largely by the bond auction outcome and sustained pressure across the belly of the curve. The reopened 2035s and 2037s cleared at 18.34% and 18.35%, respectively, ▲129bps and ▲135bps above prior stop rates, reinforcing the bearish tone across mid-tenors. The 2030s–2037s segment saw yields back up by an average of ▲82bps from Monday open to Friday close, with the sharpest repricing seen on Thursday, marking the largest intra-day move in over a month. The Treasury bills segment followed a similar tone, led by bearish activity on the benchmark 17-Jun bill, though late-week demand supported mild compression on the 17-Jun and 03-Jun papers.

In the OMO space, activity was shaped by CBN auctions, with the 03-Nov paper clearing at 20.40% early in the week before attention shifted to the 10-Nov bill. System liquidity remained positive but uneven, closing the week at ₦4.10tn.

Nigerian Equities:

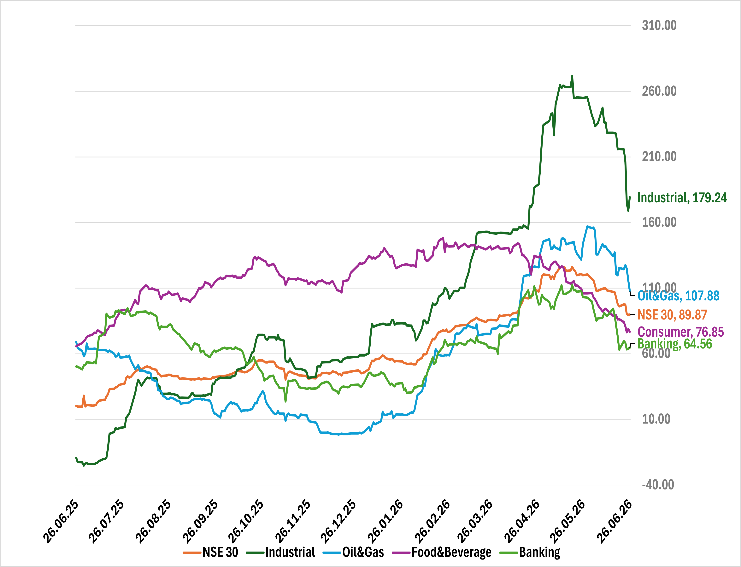

The ASI declined 1.65% WoW as the market entered a corrective phase, driven by broad-based profit-taking.Banking (+3.50%) was the only sector to close positive, while Oil & Gas (-9.86%) and Industrials (-8.21%) led losses amid sharp selloffs in ARADEL, DANGCEM and BUACEMENT. The pullback reflected investors locking in gains following the market’s strong YTD performance.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 17.80 | 18.50 | (70) |

| May-33 | 17.80 | 18.80 | (100) |

| Feb-34 | 17.80 | 18.75 | (95) |

| Jan-35 | 18.00 | 18.87 | (87) |

| Apr-37 | 18.00 | 18.77 | (77) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 17-Jun-27 | 17.05 | 17.35 | 20.86 |

| 03-Jun-27 | 16.90 | 17.30 | 20.62 |

| 22-Apr-27 | 15.90 | 16.95 | 19.67 |

Indices Watch 1-Yr Performance %

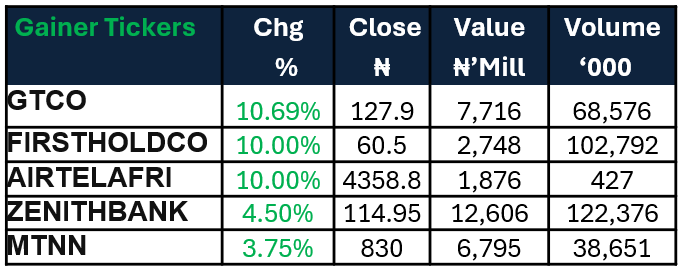

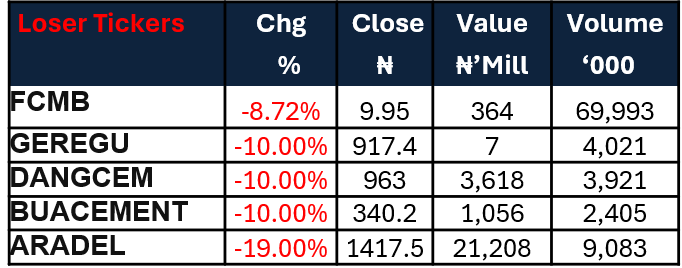

NSE 30 : Gainers and Losers

The Week Ahead…

The week is set against no scheduled primary market auction or key macroeconomic data print, with expected inflows of c.₦2.33tn from the 13.00% FGNSK Dec 2031s coupon and OMO maturities likely to support liquidity. With no incoming supply, activity is expected to be driven by renewed interest across the curve, though sentiment may remain cautious following last week’s bearish repricing.

For equities, we expect selective bargain hunting to emerge in fundamentally strong names, while attention shifts to H1 earnings expectations and macro developments, particularly oil price movements and domestic liquidity conditions, which are likely to shape near-term market direction.