Fixed Income in Focus:

The week opened on a bearish tone despite robust liquidity, with early flows concentrated in the bond segment as mid-tenors (2031s–2035s) weakened on soft auction expectations. The DMO auction, however, cleared lower than anticipated at 16.30%–16.59% (3.43x bid-to-cover), though selling pressure persisted, with yields trending higher by c.7bps–20bps across the week.

In the T-bills segment, activity was mixed, with flows largely skewed to the long end, while Apr bills saw brief demand before reversing into the close. The OMO segment saw an early-week auction with demand concentrated at the extremes, particularly the 140-day paper (4.86x bid-to-cover at 19.91%), with post-auction flows centered on the 15-Sep paper amid otherwise muted activity. Liquidity remained elevated (peaking c.₦7.78tn; closing c.₦4.96tn), with the week defined by auction-driven repricing, sustained pressure on mid-tenors, and a cautious tone into the holiday-shortened close.

Nigerian Equities:

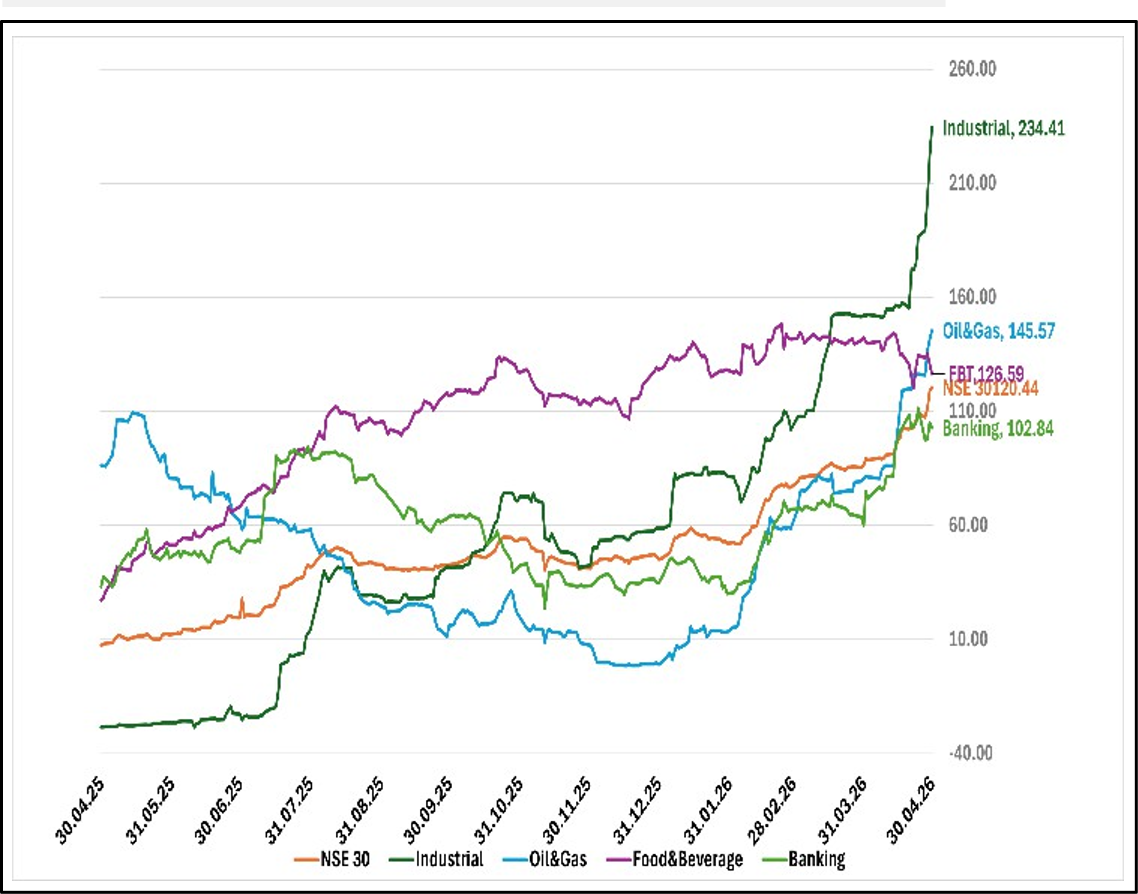

The ASI advanced 7.33% WoW to 242,277.81, extending the rally to a fifth straight week. Industrials (+16.89%) and Oil C Gas (+14.37%) led gains, while Banking (-5.52%) lagged. The move was driven by concentrated buying in large-cap industrial and energy names, supported by Q1 earnings releases, with flows rotating from banks.

Bond Auction Result

| FGN Bonds | Aug 2030s | Jun 2032s | May 2035s |

| Sales (₦‘bn) | 48.835 | 18.718 | 211.238 |

| Stop Rates | 16.30% | 16.50% | 16.59% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.85 | 16.80 | 5 |

| May-33 | 16.75 | 16.85 | (10) |

| Feb-34 | 16.70 | 16.70 | – |

| Jan-35 | 16.70 | 16.85 | (15) |

| Jun-53 | 14.70 | 14.80 | (10) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 22-Apr-27 | 16.00 | 16.00 | 18.94 |

| 08-Apr-27 | 16.05 | 15.95 | 18.73 |

| 18-Feb-27 | 16.10 | 16.20 | 18.60 |

Indices Watch 1-Yr Performance %

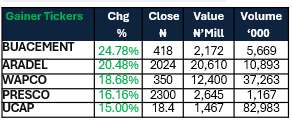

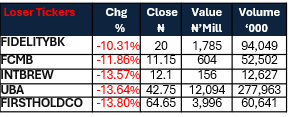

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens ahead of a scheduled NTB auction, with the DMO set to issue ₦700bn against ₦556bn maturing. Additional inflow of c.₦2.7tn is expected from OMO maturities, amplifying liquidity conditions. Market direction is likely to be driven by the auction outcome, alongside evolving global macro risks tied to the ongoing conflict.

For equities, we expect constructive but more selective trading, with Industrials and Oil C Gas likely to retain support from earnings momentum and firm crude prices. Banking may consolidate further as investors digest Q1 numbers, while follow-through will depend on whether flows broaden beyond the current large-cap leadership.