Fixed Income in Focus:

The week opened with surplus liquidity amid subdued activity, though with a bearish undertone. The bond market led early trading, with flows skewed to the mid-tenors (2031s, 2032s, 2033s, 2034s and 2035s), which recorded an average c.21bps (week open vs close) uptick in yields as selling pressure intensified into the week, further driven by the bond auction circular

Mid-week, the NTB auction cleared at previous levels, with the 364-day (22-Apr) bill trading bullish post-auction, before Apr bills reversed and backed up into the close amid muted participation. In the OMO segment, the CBN conducted an early-week auction, with demand firmly skewed to the long end, where the 140-day (08-Sep) paper printed a strong 6.2x bid-to-cover, clearing at 19.91%, with post-auction flows mildly bullish at 19.90/80% into the session. Liquidity held firm at c.₦3.97tn by close, rounding off a week defined by sustained selling pressure and cautious flows.

Nigerian Equities:

The ASI advanced 3.94% WoW to 225,724.33, with Industrials leading at (+7.70%), followed by Banking (+6.81%) and Food & Beverage (+5.25%).The rally was driven by strong buying interest in BUAFOODS, DANGCEM and WAPCO, alongside continued rotation into outperforming sectors, as Q1 earnings releases began to support sentiment.

NTB Auction Result

| 91-day | 182-day | 364-day | |

| Sales (₦‘bn) | 64.480 | 76.235 | 735.447 |

| Stop Rates | 15.95% | 16.19% | 16.199% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.55 | 16.75 | (20) |

| May-33 | 16.56 | 16.75 | (19) |

| Feb-34 | 16.45 | 16.70 | (25) |

| Jan-35 | 16.35 | 16.70 | (35) |

| Jun-53 | 14.35 | 14.70 | (35) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 22-Apr-27 | 15.80 | 16.00 | 19.01 |

| 08-Apr-27 | 15.85 | 16.05 | 18.94 |

| 18-Feb-27 | 16.00 | 16.10 | 18.54 |

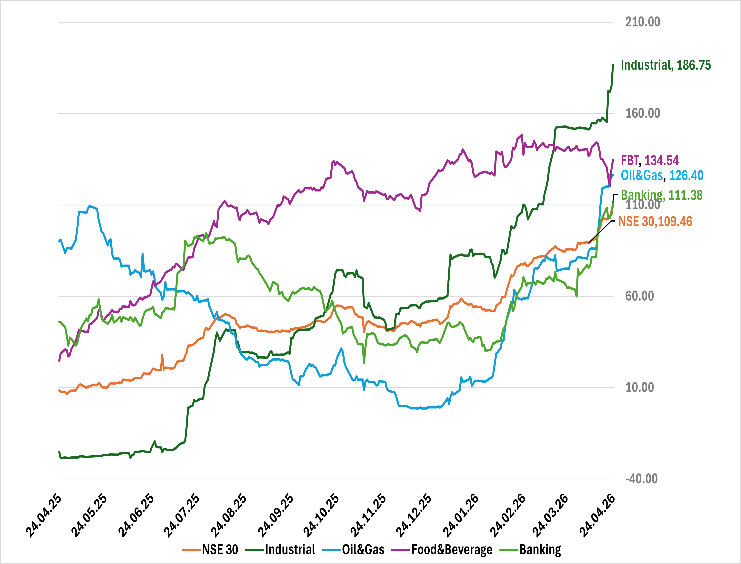

Indices Watch 1-Yr Performance %

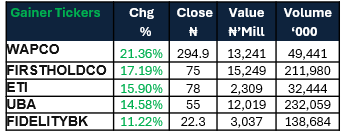

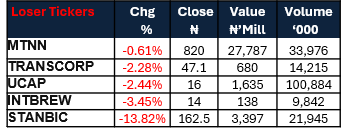

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens against a scheduled bond auction, where the DMO is set to issue ₦700bn across re-opened 5-, 7-, and 10-year tenors. This comes against a net expected inflow of c.₦1.12tn from coupons on the 14.55% Apr 2029s, 14.80% Apr 2049s, and 12.50% Apr 2032s, alongside OMO maturities, supporting liquidity. Market direction will likely hinge on auction demand and broader macro cues.

For equities, We expect market sentiment to be driven by ongoing Q1 earnings releases, while the extension of trading hours may support liquidity and price discovery. Flows are likely to remain selective, with follow-through dependent on earnings strength across sectors.