Fixed Income in Focus:

The week opened on a mixed note across the curve, with system liquidity firm at ₦7.3tn; however, price action pointed to weak underlying demand. Treasury bill activity carried a bearish tilt, with pockets of demand concentrated in the long Jan–Apr papers, which traded between 15.80%–16.00% by the close.

In the bond segment, activity was initially cautious ahead of the March inflation print (+32bps YoY vs prior). Thereafter, selling pressure intensified, with flows concentrated in the mid-tenors (2031s, 2032s, 2033s, 2034s and 2035s) as yields rose by an average of 23bps into the close. The OMO segment maintained a bearish tone from the open, with participation skewed to the long end, particularly the 01-Sep and 25-Aug papers, where flows settled around the 19.95% level by the close. Liquidity remained supportive, closing the week at ₦3.8tn

Nigerian Equities:

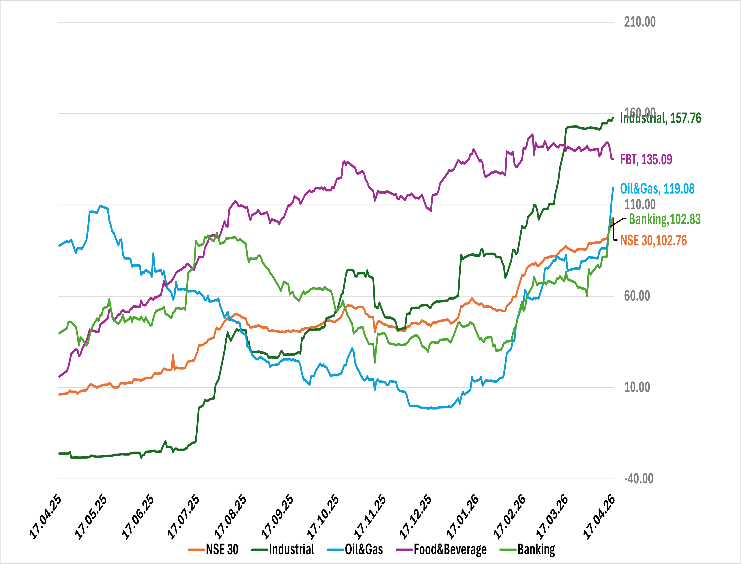

The ASI advanced 6.57% WoW, driven by strong momentum in Banking (+11.85%) and Oil & Gas (+17.59%), with Consumer goods (+3.39%) also closing positive. The rally was underpinned by firm crude prices supporting energy names and continued positioning in banks ahead of Q1 earnings and corporate developments, with market breadth expanding on renewed risk appetite.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.30 | 16.55 | (25) |

| May-33 | 16.34 | 16.56 | (22) |

| Feb-34 | 16.15 | 16.45 | (30) |

| Jan-35 | 16.20 | 16.35 | (15) |

| Jun-53 | 14.70 | 14.35 | 35 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 08-Apr-27 | 15.80 | 15.85 | 18.73 |

| 11-Mar-27 | 15.85 | 15.90 | 18.53 |

| 18-Feb-27 | 15.95 | 16.00 | 18.47 |

Indices Watch 1-Yr Performance %

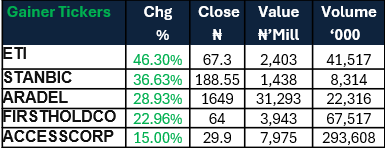

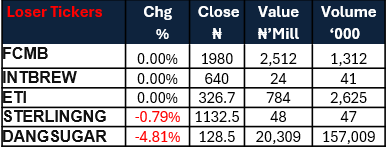

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens ahead of a mid-week NTB auction, with the DMO set to issue ₦750bn against c.₦758bn maturing. Liquidity remains robust, supported by c.₦1.85tn in OMO maturities and coupon inflows from the FGN 16.2499% Apr-2037s. Market direction will likely be dictated by the auction outcome and broader geopolitical developments

For equities, we expect selective follow-through in energy and banking names after the strong breakout, while profit-taking may begin to emerge in extended counters. With the move largely momentum-driven, flows are likely to remain tactical, with attention shifting toward Q1 earnings releases.