Fixed Income in Focus:

The week opened with surplus system liquidity of c.₦3.4tn amid muted trading and no update on the Q1 auction calendar. Early flows were mixed, with the 17-Dec, 10-Dec and 19-Nov NTBs trading around 16.30–16.60%. Mid-week, the DMO issued an auction notice indicating a 65.2% increase in supply versus the prior auction, triggering a bearish repricing across the curve. At the NTB auction, the 364-day cleared 97bps above the previous stop, while secondary trading firmed post-auction, with yields tightening into the close. Bonds tracked the move, selling on supply expectations before easing late week. In OMO, activity was muted post the mid-week auction (c.4.52x cover), with focus on the 04-Aug and 21-Jul bills trading around 19.10–30.% into the close. Liquidity remained supportive, ending the week at c.₦1.4tn.

Nigerian Equities:

The ASI rose 3.71% to close at 162,298.08, extending the early-year rebound on improving risk sentiment, led by Insurance +6.82%, Industrials +4.74% and Oil & Gas +4.70%.Market tone remained supportive with expectations of policy stability into Q1.Momentum looks constructive, with focus shifting to earnings positioning and stock-specific rotation.

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 108.170 | 48.230 | 987.784 |

| Stop Rates | 15.80% | 16.50% | 18.47% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 17.10 | 18.00 | 90 |

| Feb-31 | 17.05 | 17.95 | 90 |

| Jun-32 | 17.05 | 17.95 | 90 |

| May-33 | 17.00 | 17.90 | 90 |

| Jun-53 | 15.00 | 15.85 | 85 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 07-Jan-27 | 18.10 | 17.90 | 21.75 |

| 17-Dec-26 | 16.30 | 17.15 | 20.41 |

| 19-Nov-26 | 16.60 | 16.90 | 19.75 |

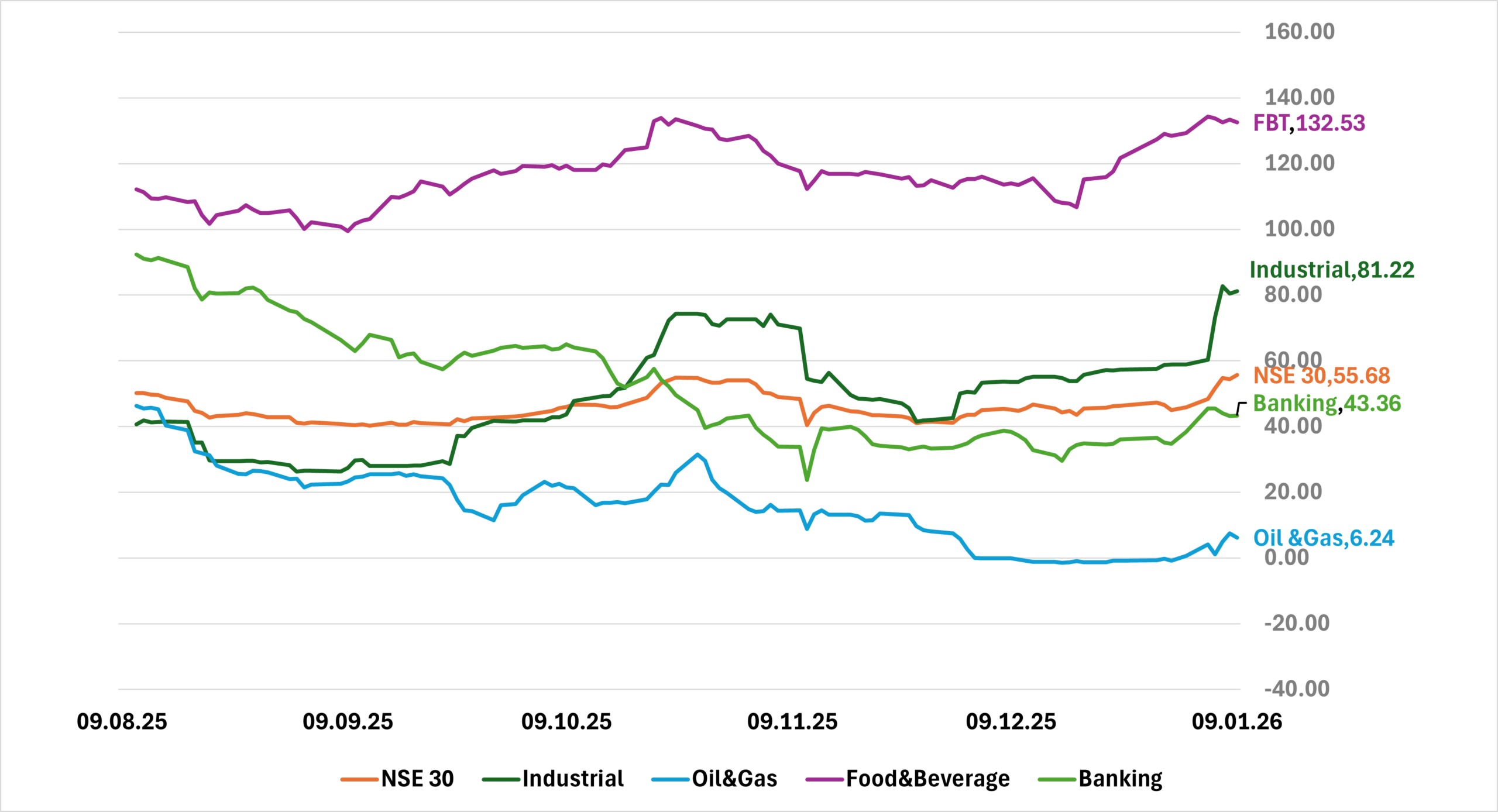

Indices Watch 1-Yr Performance %

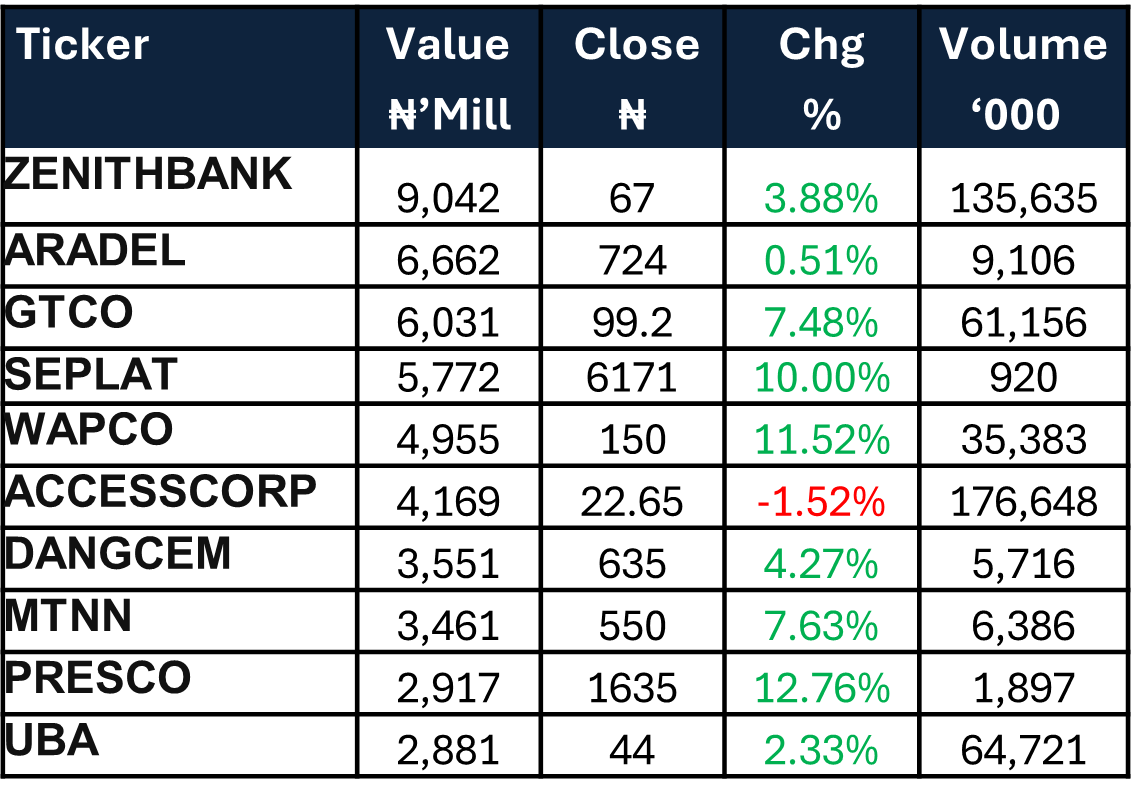

This Weeks Market Movers NGX

The Week Ahead…

The week is set against a quiet primary auction schedule, as attention turns to the December CPI inflation report due this week. The market will also be watching for any re-basing effects in the CPI outcome. Liquidity is likely to remain supportive, underpinned by an expected inflow of c.₦500bn from OMO bill maturities. In this context, the DMO may still consider an OMO auction to manage system liquidity, while the market continues to await guidance from the bond circular.

Overall, trading direction should be driven by the CPI outcome and the secondary market response, with a data-led repricing likely to set the tone through the week.