Fixed Income in Focus:

The week opened on a bullish tone following softer August inflation data, which set expectations for a dovish tilt at next week’s policy meeting. Sentiment carried into the NTB auction mid-week, where the stop rate on the 364-day bill dropped 91bps to 16.78% (20.15% eff.), confirming strong demand. Yields compressed across the curve, with the bond market seeing concentrated activity in the mid-tenor segment (’31s, ’32s, and ’33s). The OMO market sustained the bullish tone, led by strong demand in the 7-April issue into the week’s close. Despite active participation, liquidity remained ample, finishing at ₦1.66tn.

Nigerian Equities:

The ASI rose 0.92% to close at 141,845.35, building on last week’s bullish momentum. Performance was led by Consumer Goods at 5.48% and Oil & Gas at 2.79%,while Insurance declined with 4.67%.Tier 1 banks also weighed on sentiment as profit-taking pressured prices, while consumer names like Guinness drove demand. We expect flows to remain selective, with focus on energy and consumer sectors.

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 30.321 | 42.276 | 272.499 |

| Stop Rates | 15.00% | 15.30% | 16.78% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 16.60 | 16.45 | 15 |

| Feb-31 | 16.65 | 16.30 | 35 |

| Jun-32 | 16.75 | 16.35 | 40 |

| May-33 | 16.40 | 16.25 | 15 |

| Jun-53 | 15.80 | 15.80 | – |

| NTB | Bid | Ask | Effective Yield |

| % | % | % | |

| 17-Sep-26 | 16.00 | 15.90 | 18.88 |

| 03-Sep-26 | 17.10 | 16.15 | 19.09 |

| 07-Apr-26 | 19.80 | 19.20 | 21.44 |

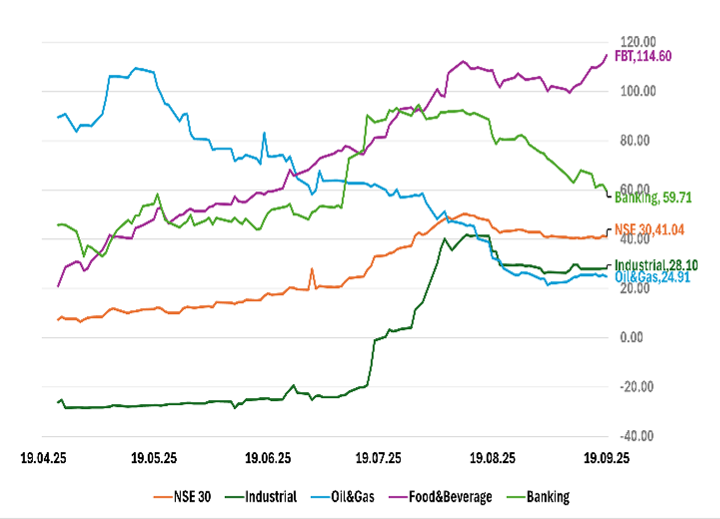

Indices Watch 1-Yr Performance %

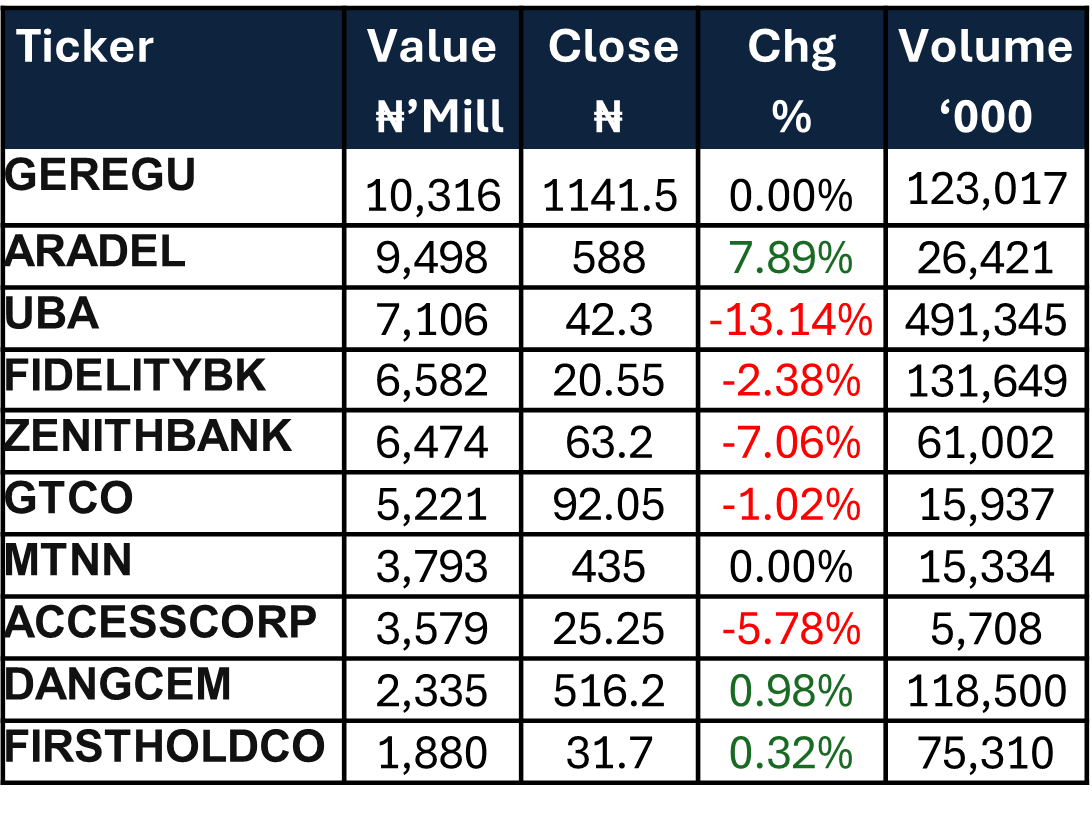

This Weeks Market Movers NGX

The Week Ahead…

The week opens with the Monetary Policy Committee (MPC) meeting, where policymakers will decide on key macro rates. Recent secondary market activity, alongside broader global market dynamics, points to expectations for a dovish outcome, likely fueling a continued bullish rally across fixed-income instruments.

We also expect inflows from NG OMO and T-Bill maturities mid-week, totaling ₦455bn, adding to already positive liquidity conditions. With no auctions scheduled, sentiment will hinge primarily on the MPC’s decision and accompanying guidance.