Fixed Income in Focus:

The market opened quietly ahead of the scheduled FGN bond auction. The sale cleared with marginal rates on the reopened 2030s and 2032s down 195 bps and 180 bps from the previous auction respectively, as aggressive bidding (bid-to-cover ratio: 6.5x) sparked a bullish move across the curve. Treasury and OMO bills followed, with the new-issue 364-day bill down 80 bps and the 17-Feb OMO lower from the week’s open. A late-week CBN OMO auction attracted strong demand, leading to a slight market pullback to end the week. System liquidity remained positive, closing at ₦5.8 trillion

Nigerian Equities:

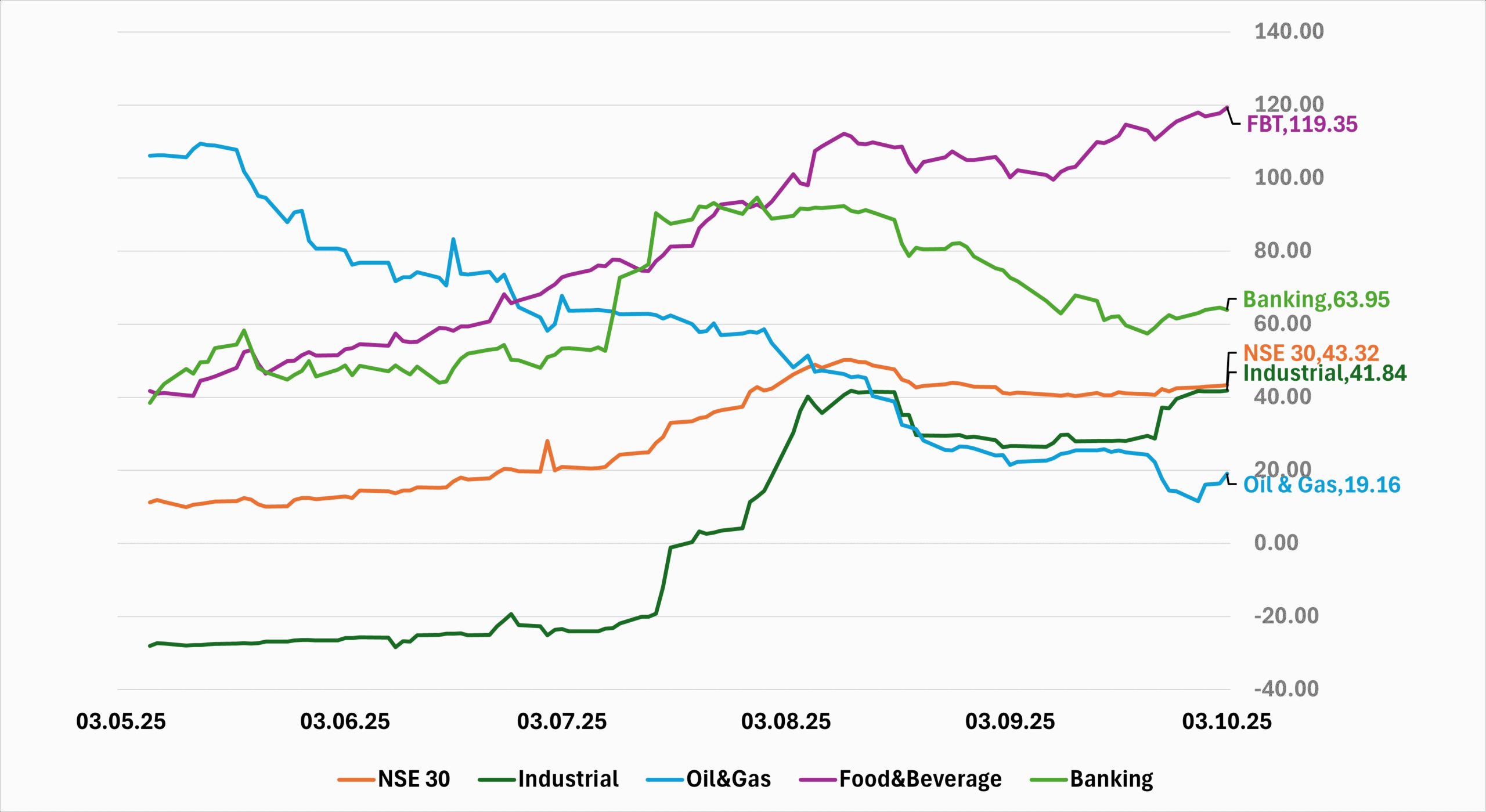

The ASI gained 1.02 % to close at 143,584.04 , maintaining its bullish momentum. Oil & Gas at 5.68 % and Industrial Goods at 1.66 % led advances as energy sentiment was sustained by interest in Aradel after Capital Alliance’s divestment. Insurance declined by 2.02% on profit-taking in mid-caps. Institutional flows remained strong, with Chapel Hill Denham executing ₦53.82 billion approximately 65% of weekly volume. We expect sentiment to stay positive in energy and industrial names.

Bond Auction Result

| 17.945% 2030 | 17.95%2032 | |

| Sales (₦‘bn) | 87.798 | 488.826 |

| Marginal Rates % | 16.00% | 16.20% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 16.55 | 15.90 | 65 |

| Feb-31 | 16.50 | 15.75 | 75 |

| May-33 | 16.55 | 15.75 | 80 |

| Jan-35 | 16.30 | 15.70 | 60 |

| Jun-53 | 15.70 | 15.60 | 10 |

| NTB | Bid | Ask | Effective Yield |

| % | % | % | |

| 17-Sep-26 | 16.00 | 15.30 | 17.90 |

| 03-Sep-26 | 16.10 | 15.40 | 17.92 |

| 20-Aug-26 | 16.20 | 15.80 | 18.97 |

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

In anticipation of the NTB Q4 auction calendar and with no key macro data due, the week is set to open on a muted note as focus turns to an expected ₦1.135tn inflows from NTB and OMO maturities, and the possibility for a mid week NTB auction.

Last week’s OMO auction, the first in weeks, suggests the CBN may continue with multiple issuances to mop up surplus liquidity. Bullish sentiment persists at current yield levels; however, additional OMO supply from here could temper further upside and prompt a near-term pullback.