Fixed Income in Focus:

The week opened with heavy activity across local fixed income: the CBN issued about ₦3.2tn in OMO bills across tenors, closing in a 21.16%–21.54% yield range, driven by reinvestment demand and supported by ample liquidity. Attention shifted mid-week to the NTB auction, where the DMO brought its largest 364-day supply in weeks; stops fell ~100bps versus the prior auction on aggressive long-end bids, with secondary levels holding into week-end around 18.17%. In the bond market, yields consolidated early (c. 15.75%–15.80%) before tilting slightly bearish into the close. Amidst robust market participation, system liquidity remained firm at a ₦3.38tn surplus.

Nigerian Equities:

The ASI advanced 2.37 % to close at 146,988.04, maintaining bullish momentum led by Industrials at 4.23 % and Insurance at 3.69 %, while Banking declined by 0.41%. Overhang came from the ongoing capital gains tax debate and optimism from strong showings in MTN,SEPLAT and DANGOTE CEMENT. Financials with 60 % of trades, led in volume and we expect momentum to favor industrials.

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 25.374 | 41.327 | 503.298 |

| Stop Rates | 15.00% | 15.25% | 15.77% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 15.90 | 16.00 | (10) |

| Feb-31 | 15.75 | 16.05 | (30) |

| Jun-32 | 15.75 | 15.85 | (10) |

| May-33 | 15.70 | 15.85 | (15) |

| Jun-53 | 15.40 | 15.20 | (20) |

| NTB | Bid | Ask | Effective Yield |

| % | % | % | |

| 08-Oct-26 | 15.50 | 15.40 | 18.17 |

| 17-Sep-26 | 15.30 | 15.50 | 18.12 |

| 03-Sep-26 | 15.40 | 15.20 | 17.59 |

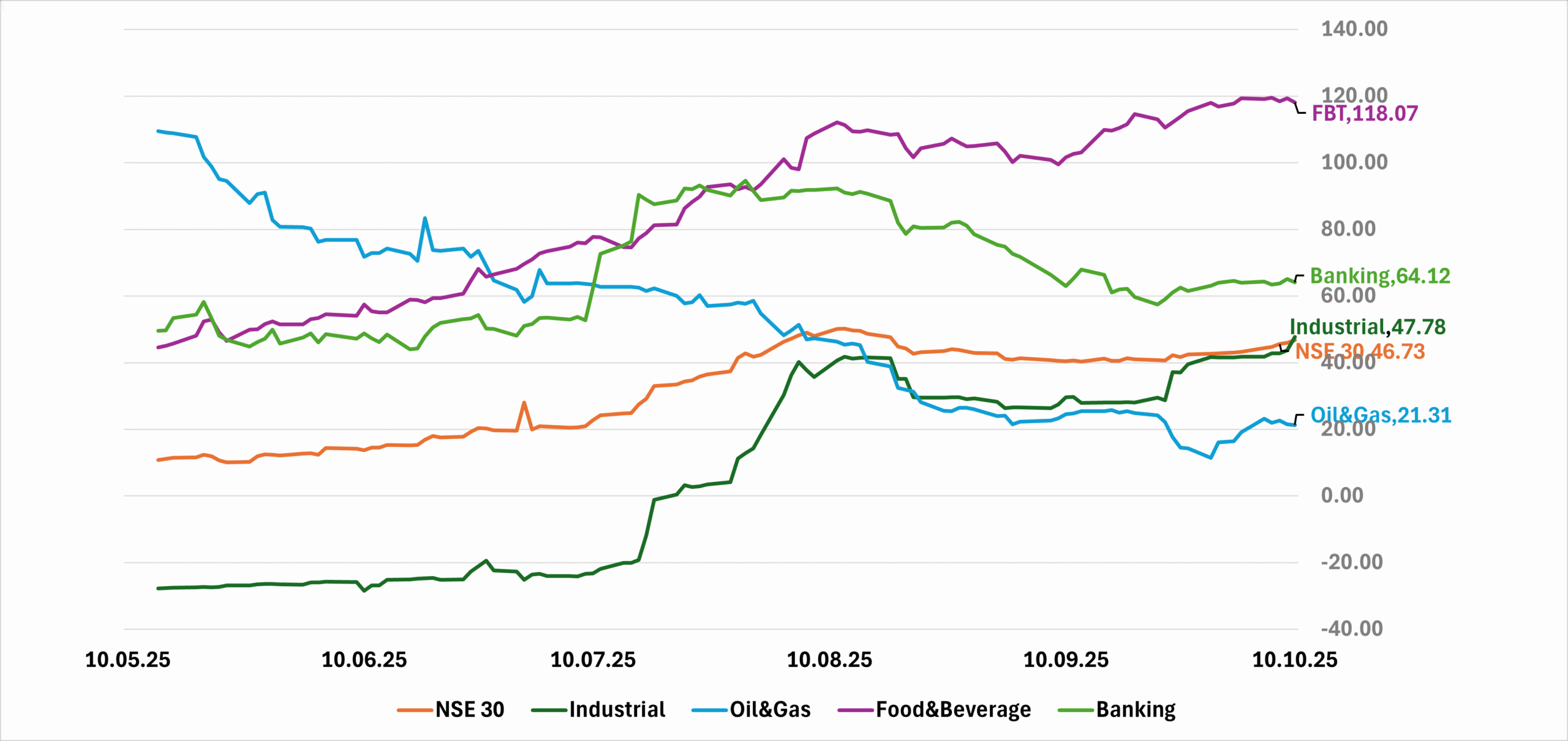

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

The week opens with focus on the September CPI release, no auctions scheduled, and about ₦600bn in inflows from OMO maturities and coupons on FGN 2029s and FGNSK 2033s, adding to already positive system balances.

Dovish CPI sentiment could spur early-week buying across bills and bonds, while neutral sentiment may keep trade steady amid strong liquidity. A hawkish tone could prompt mild profit-taking toward the long end, but overall market direction will hinge on the prevailing inflation narrative.