Fixed Income in Focus:

The week opened with a c.₦956bn liquidity surplus. The CBN issued about ₦827bn in OMO bills across tenors, clearing in a 21.73%–22.8% yield range on solid participation. Ahead of the mid-week NTB sale, profit-taking tilted bills bearish, with the 8-Oct trading near 15.60%. At auction, the long end cleared c.+37bps versus prior stops on roughly 1.50× cover; post-auction, unmet demand turned tone bullish, lifting long executions to c.15.70%. In bonds activity concentrated on the mid-segment (’31s/’32s/’33s), but sentiment stayed broadly bearish into the close ahead of next week’s supply. Despite a bearish week close system liquidity remained firm at c.₦3.1tn.

Nigerian Equities:

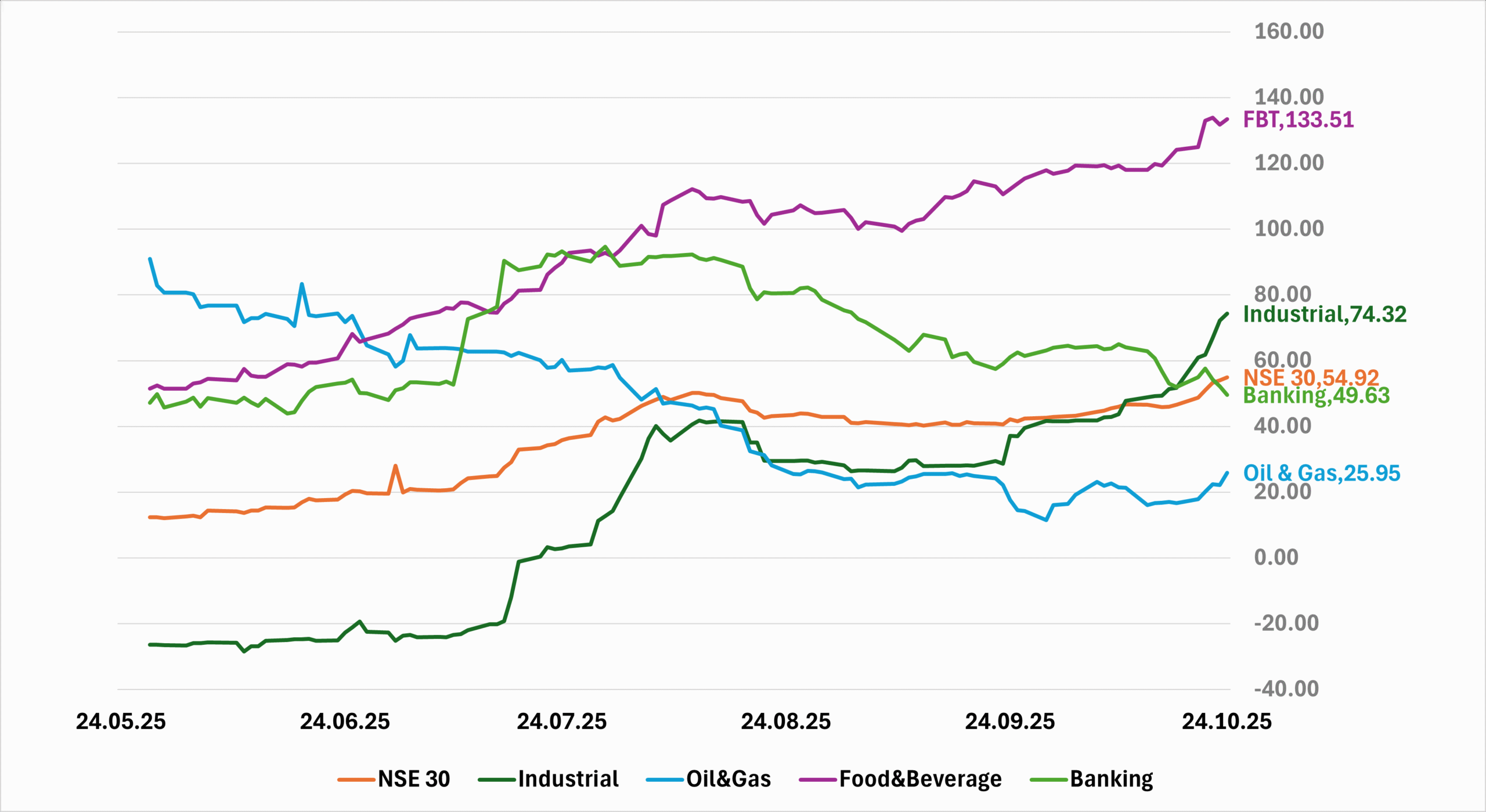

The Nigerian Exchange Limited (NGX) All-Share Index continued its bullish run, advancing 4.48% to close at 155,645.05 , led by Industrials at 10.61% and Oil & Gas at 9.13%, while the Insurance and banking sector lagged slightly. Key drivers included heavy-cap rallies and renewed investor optimism. We expect momentum to remain skewed toward Industrials and Oil & Gas, with financials staying under watch.

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 7.613 | 67.418 | 316.556 |

| Stop Rates | 15.30% | 15.50% | 16.14% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 15.90 | 16.25 | (35) |

| Feb-31 | 15.65 | 16.05 | (40) |

| Jun-32 | 15.65 | 16.10 | (45) |

| May-33 | 15.70 | 16.00 | (30) |

| Jun-53 | 14.85 | 15.00 | (15) |

| NTB | Bid | Ask | Effective Yield |

| % | % | % | |

| 22-Oct-26 | 15.85 | 15.70 | 18.60 |

| 08-Oct-26 | 15.40 | 15.50 | 18.19 |

| 03-Sep-26 | 15.40 | 15.70 | 18.12 |

Indices Watch 1-Yr Performance %

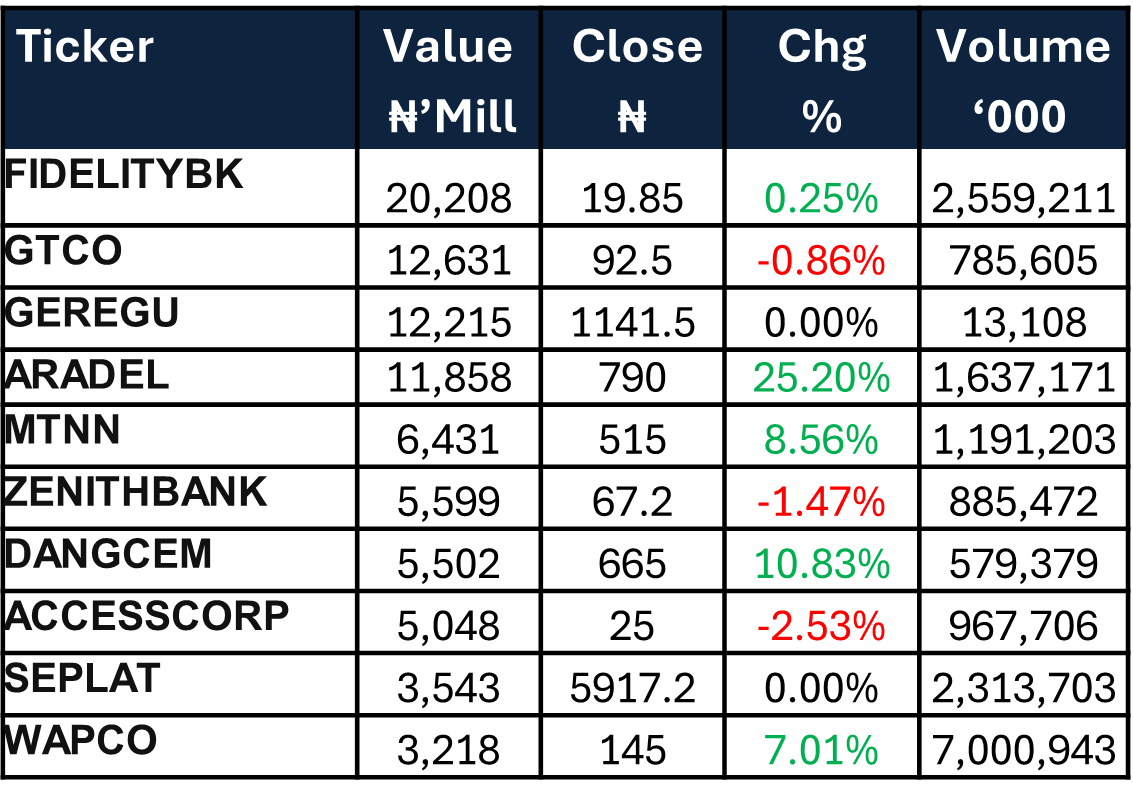

This Weeks Market Movers NGX

The Week Ahead…

The week opens with a scheduled FGN bond auction, where the DMO is expected to re-open ₦260bn across the 17.945% FGN AUG 2030 and 17.950% FGN JUN 2032 papers. This comes alongside an estimated ₦260bn in coupon inflows from the FGN APR 2029s, 2049s, and 2032s, which should help sustain system liquidity.

With no major macro data releases expected, market sentiment will largely hinge on the bond auction outcome. Following last week’s bearish close, we expect a cautious tone to persist, with stop rates projected within the 16.09%–16.29% range; shaping market activity throughout the week