Fixed Income in Focus:

The week opened quietly with September CPI in view, and system liquidity sitting at ₦2.08tn. OMO bills set the early tone, with the 10-Mar and 21-Apr lines trading around 18.75% – 19.00%. Attention then shifted to NTBs as traders leaned for a softer CPI print; the 8-Octbill firmed to 15.55% ahead of the release. CPI printed 18.02% YoY, down from 20.12% in August (-210 bps),marking a sixth straight monthly decline, and executions on 8-Oct tightened to c.15.35% post-CPI. In the bond space, the Q4 issuance circular kept sentiment cautious at first, with mid-tenor executions around 16.00%–16.25%. Post-CPI, tone improved and mid-tenor yields fell 20–45 bps. The week closed with a well subscribed, CBN OMO auction recording bid-to-cover ratios of 2.40× and 4.68× on the 193-day and 249-day bills respectively, as liquidity firmed around ₦1.8 trillion.

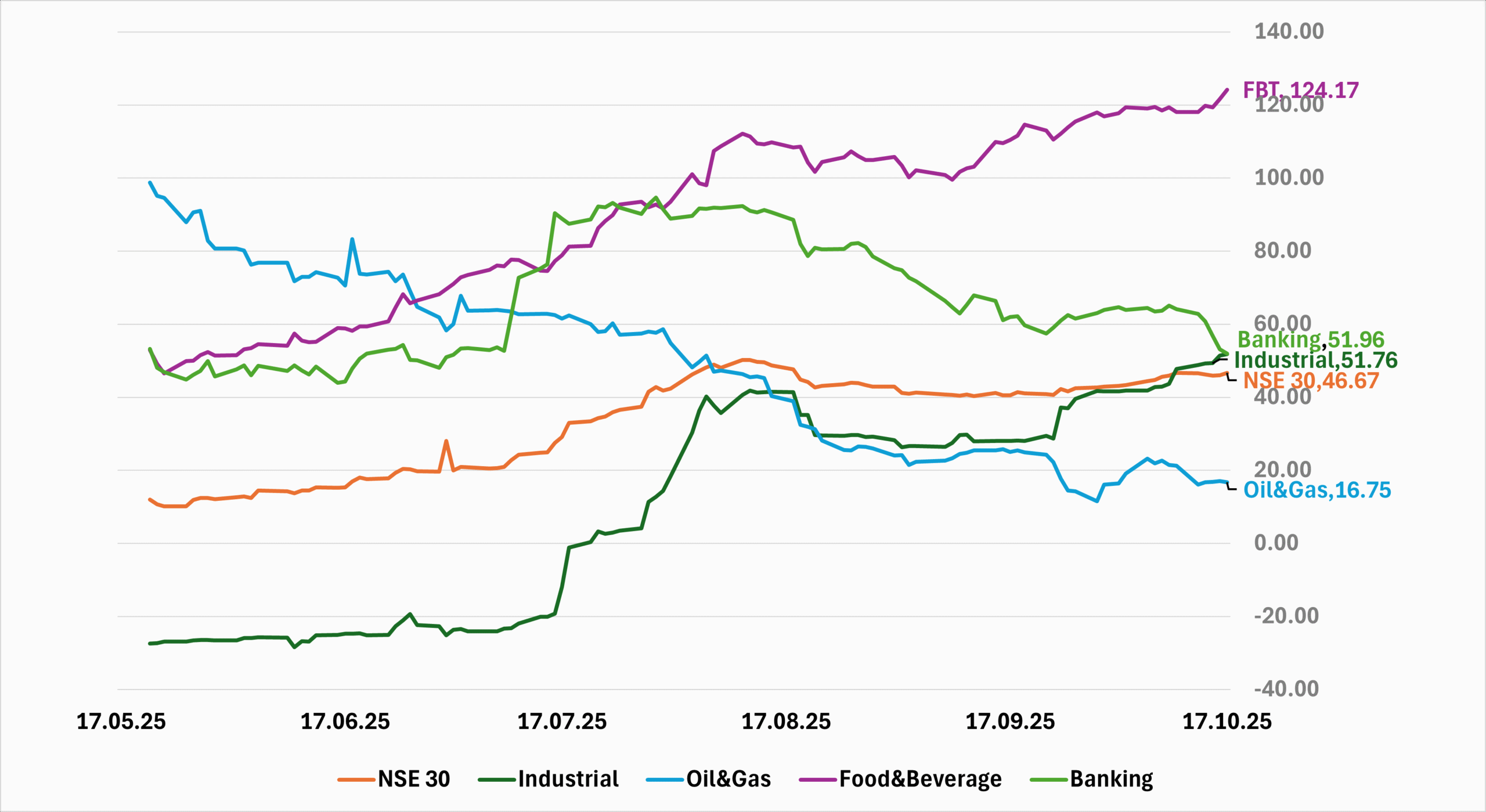

Nigerian Equities:

The ASI advanced 1.35% to close at 148,977.64, maintaining its bullish uptrend. Performance was led by Industrials and Insurance with 2.79% and 2.56% respectively, while Banking slipped slightly by -0.13%. Sentiment was underpinned by renewed interest in large-caps and cooler September inflation encouraging risk appetite. We expect flows to tilt towards industrials and consumables

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 16.00 | 15.90 | 10 |

| Feb-31 | 16.05 | 15.65 | 40 |

| Jun-32 | 15.85 | 15.65 | 20 |

| May-33 | 15.85 | 15.70 | 15 |

| Jun-53 | 15.20 | 14.85 | 35 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 08-Oct-26 | 15.55 | 15.40 | 18.10 |

| 23-Jul-26 | 15.75 | 15.50 | 17.57 |

| 23-Apr-26 | 16.00 | 15.55 | 16.88 |

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

The week opens with attention on the scheduled NTB auction, where the DMO plans to issue ₦650bn across tenors against c.₦378bn maturing. With no major macro releases due, the tone should be set by pre-auction positioning and, ultimately, by participation and stop rates after sale.

A key swing factor is a potential OMO announcement. If the CBN offers another set of long-dated papers, bids could split between OMO and NTBs, creating a relative-value trade that shapes market tone for the rest of the week.