Fixed Income in Focus:

The week opened quietly ahead of the October inflation print, with system liquidity surplus at c.₦1.3tn. Trading opened with mid-tenor bonds rallying after headline inflation fell to 16.08% (-197bps m/m), though profit-taking later in the week saw yields retrace by c.25bps into the close. In the T-bills market, activity was bullish ahead of the mid-week auction, which cleared at prior levels with an overall bid-to-cover of 1.85x; the 364-day paper was briefly pressured by excess supply (2.73x cover), backing up c.25bps before recovering to close c.15.80%. The OMO space was active, with an early-week auction clearing in the 20.45–20.54% band at 1.63x cover and secondary trading mixed around 20.20% yield, while liquidity firmed to c.₦3.9tn by close.

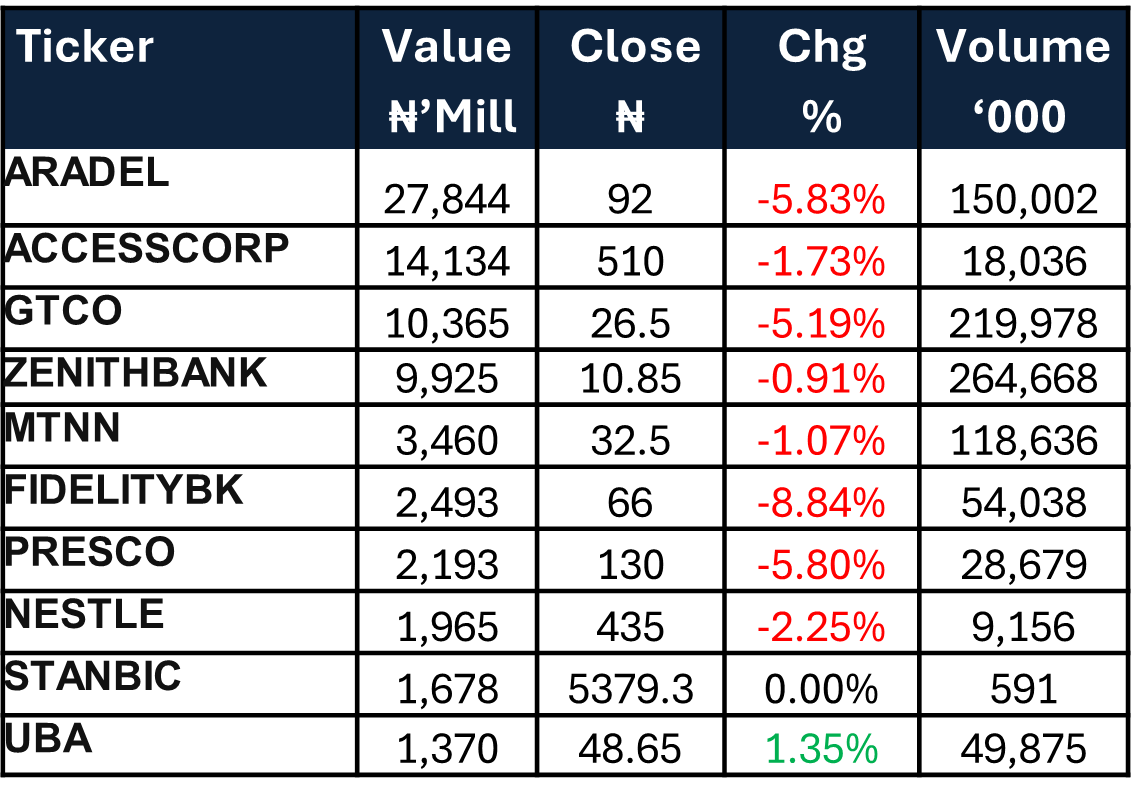

Nigerian Equities:

The ASI slipped 2.24% to 143,722.62, marking a fourth straight weekly decline as risk aversion mounted. Insurance (-7.05%) and Industrials (-4.50%) led the downturn. Heavy-cap sell-offs in ACCESSCORP and Dangote Cement added to the drag. Liquidity remained tight as the CBN’s OMO/NTB cycle effectively absorbed system inflows. We expect sentiment to stay defensive with rotation into cleaner mid-caps while large-cap pressure persists

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 33.808 | 26.414 | 1,029.79 |

| Stop Rates | 15.30% | 15.50% | 16.04% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 15.40 | 15.60 | (20) |

| Feb-31 | 15.30 | 15.60 | (30) |

| Jun-32 | 15.25 | 15.60 | (35) |

| May-33 | 15.25 | 15.55 | (30) |

| Jun-53 | 14.30 | 14.40 | (10) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 19-Nov-26 | 16.00 | 15.80 | 18.73 |

| 05-Nov-26 | 15.10 | 15.40 | 18.04 |

| 22-Oct-26 | 15.25 | 15.35 | 17.85 |

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

The week opens ahead of an FGN bond auction, where the DMO is expected to reopen c.₦250bn across the 17.945% Aug 2030 and 17.95% Jun 2032, alongside c.₦503bn in inflows from maturing NG OMOs and coupons on the May 2029 and Nov 2028 bonds supporting a net positive liquidity balance.

The 303rd MPC meeting is also scheduled early in the week. Given the continued disinflation trend, the latest CPI print and the market’s recent dovish positioning, we see room for a c.100bps cut in the MPR and a modest corridor adjustment, with trading likely to be driven largely by the MPC outcome.t unless OMO sizes or yields surprise to the upside.