Fixed Income in Focus:

The week opened with c.₦3.8tn in system surplus liquidity. In the NTB market, demand was skewed to the long end, with October and November bills trading below 15.50%. In the bond market, activity was broad-based, with bullish interest in the mid-tenor 33s, 32s, and 31s, which printed around c.15.20–15.50% from early to mid-week. OMO activity strengthened mid-week, with executions between 18.20–18.60% on the 21-April and 23-June papers, followed by a long-dated CBN OMO auction that attracted strong demand, achieving a 5.15x bid-to-cover and clearing at 20.59%–20.70% across tenors. Post-auction, the newly issued bills traded about c.65bps below their auctioned stop rates, with executions recorded at 19.75% on the 5-May and 20.00% on the 14-April papers, while system liquidity remained firm at c.₦6.1tn.

Nigerian Equities:

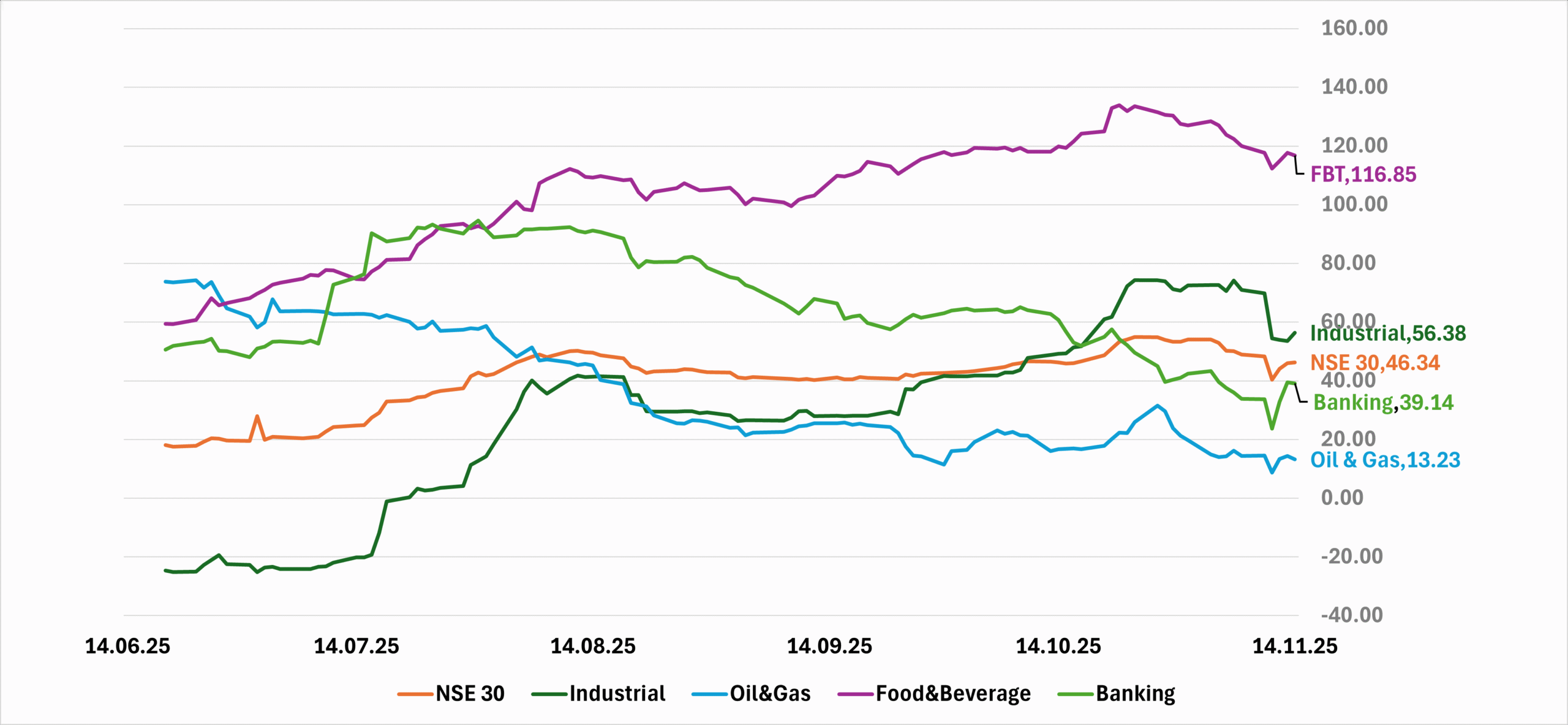

The ASI slipped 1.68% to close at 148,977.64, reflecting a cautious week as tax-policy anxieties and profit-taking edged into the market. Insurance gained 2.42% while Industrials eased about -1.09%, and Banking slid -3.85%. Sentiment was supported by fiscal-policy reassurance, yet weighed by weakness in key large-cap names. We expect flows to remain selective, with emphasis on mid-caps as investors await clearer catalysts

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 15.65 | 15.40 | 25 |

| Feb-31 | 15.65 | 15.30 | 35 |

| Jun-32 | 15.65 | 15.25 | 40 |

| May-33 | 15.55 | 15.25 | 30 |

| Jun-53 | 14.60 | 14.30 | 30 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 05-Nov-26 | 15.60 | 15.10 | 17.69 |

| 22-Oct-26 | 15.50 | 15.25 | 17.78 |

| 08-Oct-26 | 15.60 | 15.30 | 17.72 |

Indices Watch 1-Yr Performance %

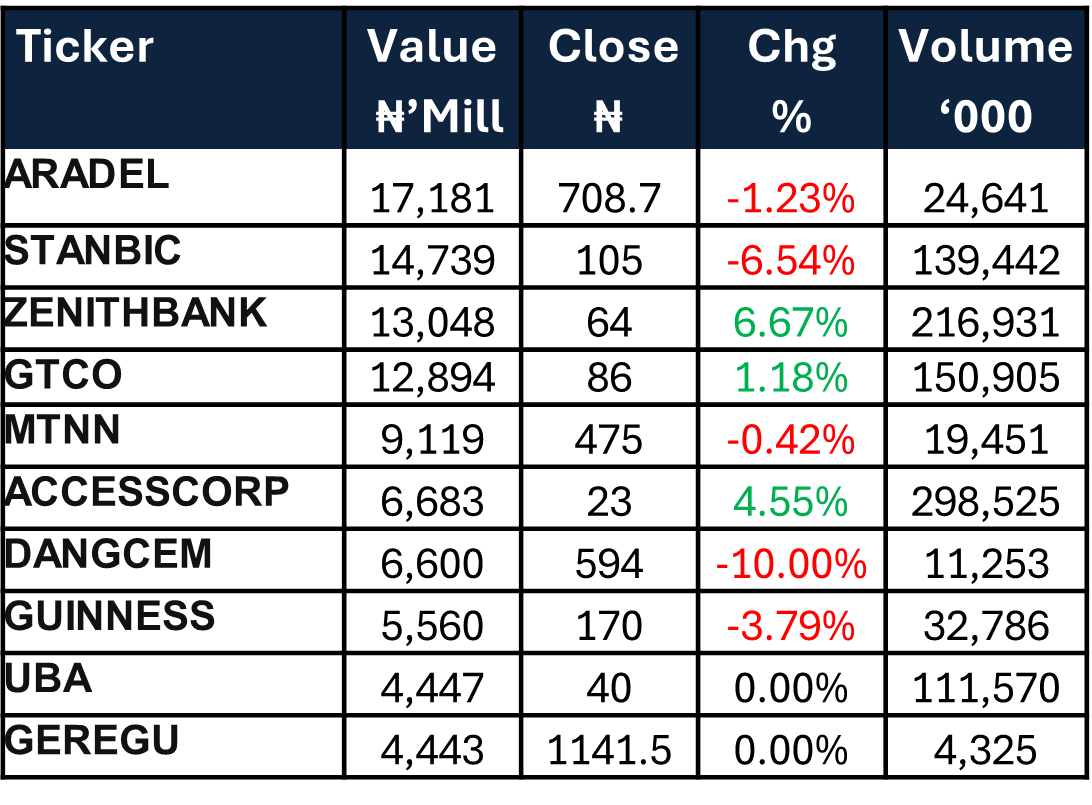

This Weeks Market Movers NGX

The Week Ahead…

The week opens with attention on the scheduled NTB auction, where the DMO plans to issue ₦700bn across tenors against c.₦689bn maturing. System liquidity is further supported by coupon payments: c.₦8.57bn in Nov-29s , c.₦251bn in May-33s and ₦117.5bn in OMO maturities.

With October CPI inflation data in view, the tone of the week is likely to be set by the inflation print, the strength of demand and stop rates at the auction, and subsequent secondary-market flows. We anticipate a relatively dovish inflation outcome, which should support a mildly bullish bias across the curve.