Fixed Income in Focus:

The week opened on a quiet note, with bulk activity in the OMO market early on as investors positioned ahead of the MPC policy decision. The Committee cut the MPR by 50 bps to 27.00%, though the bond market showed little reaction as the move had largely been priced in beforehand. By midweek, bearish sentiment emerged, with mid-tenor bonds (’31s, ’32s, and ’33s) and September Treasury bills retreating in yield as firm bids signaled weakness and a preference for higher returns into the week’s close. This shift came despite a liquidity surplus of ₦4.02tn, highlighting the market’s sensitivity to yield expectations over funding conditions.

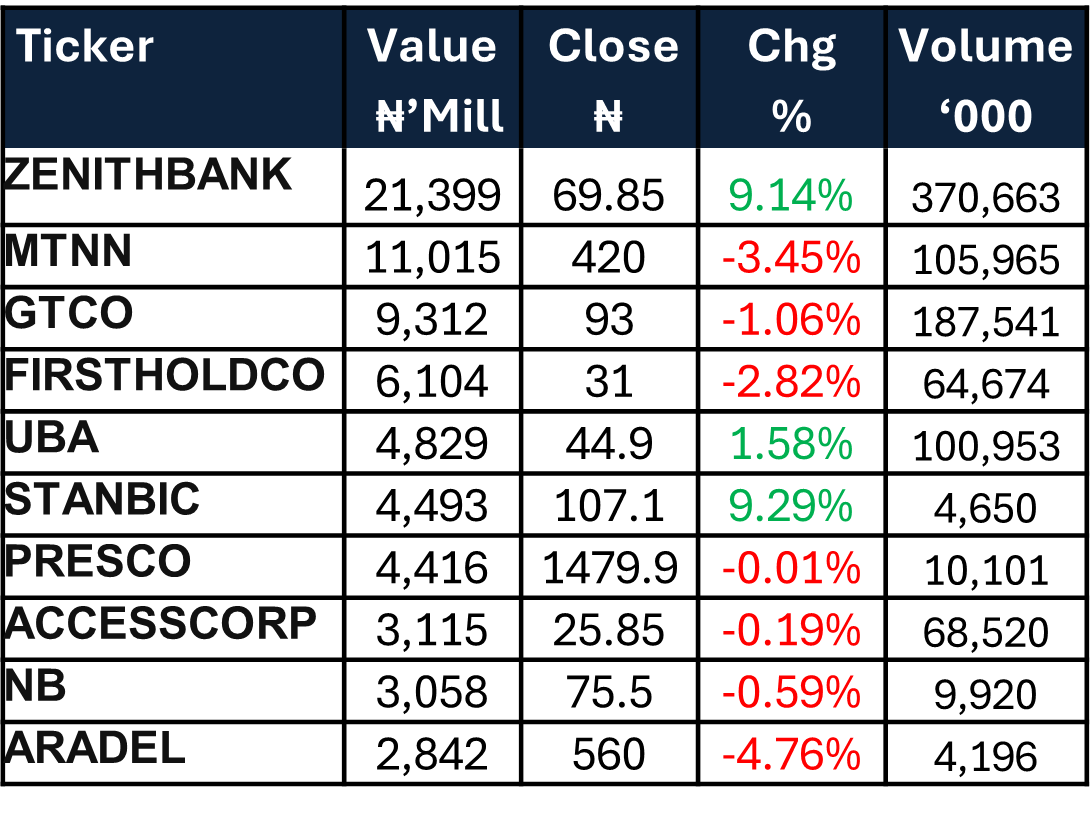

Nigerian Equities:

The ASI gained 0.20% to close at 142,133.03, marking a third straight weekly advance. Industrials led with 1.33% as Lafarge and Dangote Cement firmed, while Banking rose 1.19% on strong tier-1 demand, led by Zenith and Stanbic. Oil & Gas slipped despite Capital Alliance’s ₦387bn divestment of its 15% stake in Aradel. Investors are positioning for Q3 result releases as impressive earnings are expected from industrials and consumers.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 16.55 | 16.55 | – |

| Feb-31 | 16.35 | 16.50 | (15) |

| May-33 | 16.30 | 16.55 | (25) |

| Jan-35 | 16.25 | 16.30 | (5) |

| Jun-53 | 15.75 | 15.70 | 5 |

| NTB’s & OMO | Open | Close | Effective Yield |

| % | % | % | |

| 17-Sep-26 | 15.90 | 16.00 | 18.94 |

| 03-Sep-26 | 16.05 | 16.15 | 19.01 |

| 07-Apr-26 | 18.60 | 18.30 | 20.24 |

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

Monetary Policy Rate Expectation

MPC Policy View:

As at the 302nd Monetary Policy Committee (MPC) Meeting held on September 22nd–23rd 2025, the Committee cut the Monetary Policy Rate (MPR) by 50 basis points, from 27.50% to 27.00%. Other parameters were adjusted as follows: the Cash Reserve Ratio (CRR) for commercial banks was reduced by 500 basis points, from 50% to 45%, while the CRR for merchant banks was retained at 16%. A new CRR of 75% was introduced on non-TSA public sector deposits. The Asymmetric Corridor was narrowed from +500/-100 bps to +250/-250 bps, and the Liquidity Ratio was maintained at 30%.

Nigeria’s headline inflation eased to 20.12% in August 2025, down 176 bps from 21.88% in July, marking the fifth straight monthly decline. Yet pressures persist, with food inflation at 21.87%, core inflation at 20.33%, and Month-on-Month inflation rising 74 bps (0.74%). With inflation on a steady downward path and the 302nd MPC already signaling the start of a cutting cycle, can expect a bullish rally in the coming weeks as yields compress across all tenors.

The Week Ahead…

The week is set to open with a bond auction, where the DMO on behalf of the FGN will reopen ₦200bn of the FGN Jun ’32s and FGN Aug ’30s. Also, inflows of about ₦896bn are expected early in the week from FGN Mar ’35 and FGN Mar ’50 coupon payments, as well as NG OMO maturities. With no key macro data releases scheduled, market activity will likely hinge on the auction outcome. Should the DMO choose to over-issue and the CBN move to absorb liquidity with an early-week OMO, yields could push higher, sustaining the bearish momentum across the curve; conversely, restraint on both fronts would allow for a bullish reversal.