Fixed Income in Focus:

The week opened with dampened demand across the curve, due to negative liquidity, and CBN’s MPC meeting. NTB activity increased as investors repositioned before the midweek auction. The benchmark 365-day bill extended its bearish trend, shedding 42bps as the CBN stuck to its planned issuance size. Activity in the bond market focused on short- to mid-tenors, supported by a circular hinting at a smaller upcoming offer. In the OMO space, buy-side interest picked up later in the week, particularly on the Jan OMO’s, as system liquidity improved, closed at ₦1.345 trillion.

Nigerian Equities:

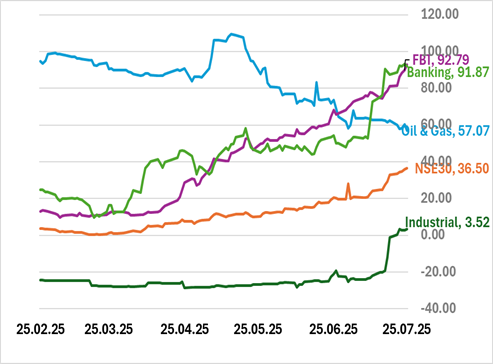

The All-Share Index appreciated 2.18% this week owing to large demand for Industrial, Consumer Goods, and NSE30 stocks with the respective indices gaining 4.66%, 2.81%, and 2.03% each. Half-year results have begun to trickle out with Industrial heavy weights BUACEMENT, LAFARGE, and WAPCO posting tremendous gains. We expect the bull run to continue ahead of further results releases from breweries and consumer goods.

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 13.107 | 5.104 | 271.788 |

| Stop Rates | 15.00% | 15.50% | 15.88% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 16.30 | 16.15 | 15 |

| Feb-31 | 16.95 | 16.00 | (5) |

| May-33 | 16.90 | 15.95 | (5) |

| Jan-35 | 16.05 | 16.00 | 5 |

| Jun-53 | 15.60 | 15.55 | 5 |

| NTB | Bid | Ask | Effective Yield |

| % | % | % | |

| 23-Jul-26 | 15.20 | 15.75 | 18.66 |

| 05-Mar-26 | 16.80 | 16.75 | 18.64 |

| 23-Apr-26 | 16.40 | 16.15 | 18.34 |

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

Monetary Policy Rate Expectation

MPC Policy View:

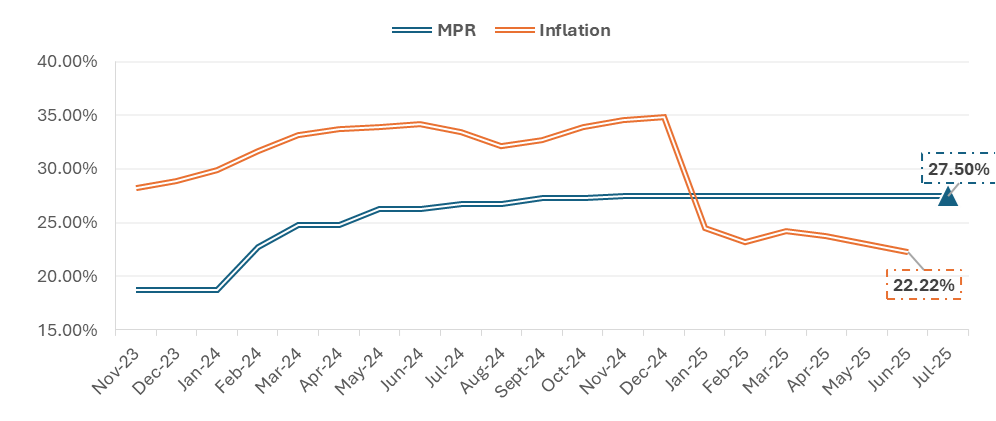

As at the 301st Monetary Policy Committee (MPC) Meeting held on July 22nd 2025, the Committee decided to maintain the Monetary Policy Rate (MPR) at 27.50% and other parameters, the Cash Reserve Ratio (CRR) for commercial banks, Asymmetric Corridor and Liquidity Ratio to remain at 50%, +500/-100 bps, and 30% respectively.

Since April’s height of 23.71%, headline inflation has declined for two consecutive months, dropping to 22.97% in May and further to 22.22% in June 2025. Though headline inflation is easing, underlying pressures persist as food inflation was 21.97%, while core inflation remained elevated at 22.76%, signaling continued broad-based inflationary momentum as Month-on-Month inflation increased by 1.68% from May to June.

We expect the MPC to hold benchmark rates at current levels, in line with recent guidance. CBN Governor Olayemi Cardoso has reiterated that there are no plans to cut rates in the near term, emphasizing the focus on anchoring inflation expectations. While headline inflation is moderating, persistent core inflation suggests that a cautious stance will remain until disinflation is broader and more sustained.

The Week Ahead…

The new week opens on a relatively constructive note, anchored by Monday’s bond auction where the DMO will reopen the April 2029 and June 2032 papers with planned issuance of ₦20 billion and ₦60 billion respectively.

Market tone is expected to remain firm, supported by healthy system liquidity, a ₦41 billion coupon inflow from the January 2035 bond. These dynamics may bolster demand at the auction and guide trading sentiment through the week.