Fixed Income in Focus:

The fixed income market traded on a muted note through the week, with activity remaining largely selective across the curve. While bearish pressure was evident across parts of the mid-tenor segment following the release of the bond auction circular, the broader curve closed on a mixed note, with the 2030s and 2031s trading on a slight bullish tilt from week open to close, while the 2032s–2034s repriced higher in yield. The Treasury bills segment traded firmer, with demand skewed towards the long end, particularly across the Apr and May bills.

The OMO segment was largely quiet for most of the week, before activity picked up on Friday following the CBN’s early-session auction across the 32-day, 116-day and 137-day papers, clearing at 18.90%, 19.59% and 20.00%, respectively. Demand was strongest on the 137-day paper at 7.05x bid-to-cover, while overall auction bid-to-cover settled at 3.53x. The week closed around the April CPI print, which came in slightly below market expectations, driving mixed post-print flows across the curve. System liquidity remained broadly supportive, closing the week higher at ₦5.86trn.

Nigerian Equities:

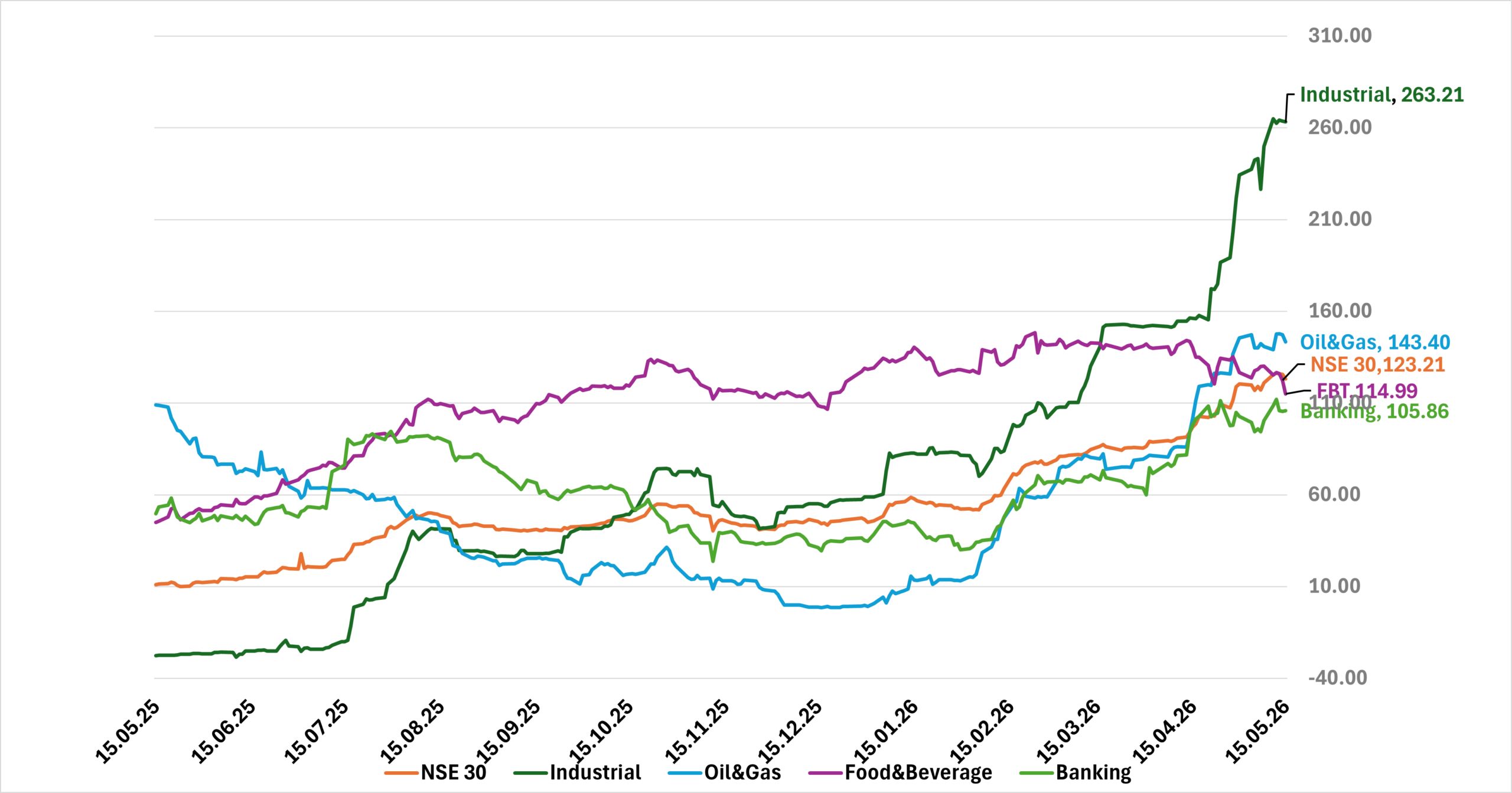

The ASI advanced 2.27% WoW, extending the market’s bullish momentum. Industrials led gains (+4.66%),then banking (+2.82%) ,while Oil & Gas (-1.19%) lagged on continued profit-taking. The advance was supported by buying interest in large-cap industrial and banking names, while sentiment remained underpinned by earnings releases.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.80 | 16.77 | 3 |

| May-33 | 16.80 | 16.85 | (5) |

| Feb-34 | 16.65 | 16.65 | (20) |

| Jan-35 | 16.60 | 16.85 | (25) |

| Jun-53 | 14.82 | 14.85 | (3) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 06-May-27 | 15.90 | 15.75 | 18.59 |

| 22-Apr-27 | 15.90 | 15.80 | 18.53 |

| 18-Mar-27 | 16.10 | 16.10 | 18.27 |

Indices Watch 1-Yr Performance %

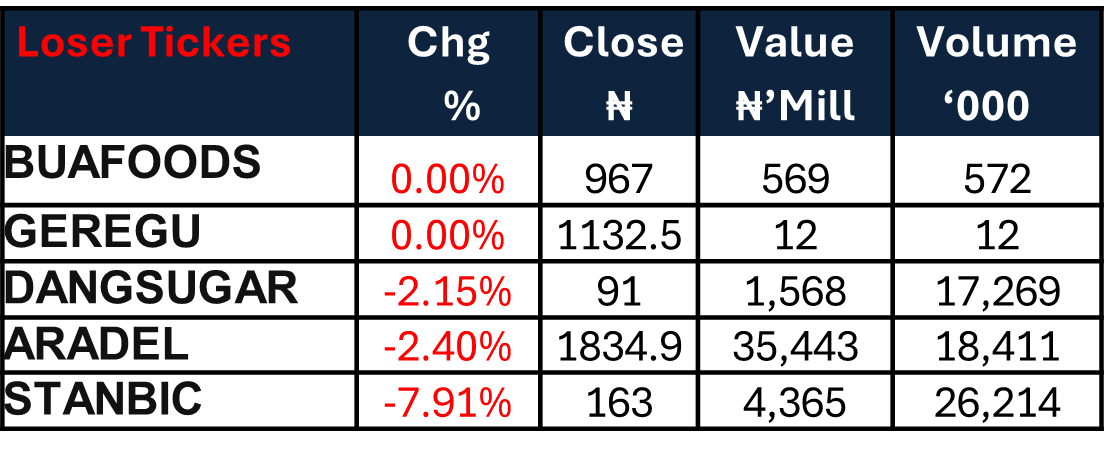

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens with the MPC meeting and scheduled bond auction in focus, as the DMO offers ₦600bn across the Jan 2035s and Apr 2037s. Liquidity should be supported by c.₦3.2tn in expected inflows from NGOMO/NTB maturities and coupon payments from the 8.50% Nov 2029s, 12.49% May 2029s and 19.75% FGNSK May 2032s, while activity is likely to be driven by MPC positioning, auction demand and possible CBN OMO issuance.

For equities, With the latest inflation print and MPC decision now in focus, market direction is likely to remain earnings- and policy-sensitive in the near term. Flows may continue toward fundamentally supported names.