Fixed Income in Focus:

The week opened on a bearish tone as caution persisted amid the ongoing Middle East tensions. In the fixed income space, despite surplus liquidity, yields backed up early in the week. Bonds traded bearish by c.10bps with activity focused on the mid-tenor. Towards week-end, we saw a mild rally ahead of next week’s inflation print. Treasury bills saw similar activity, with the mid-week auction clearing slightly bullish(1bp lower vs previous stops). Demand was centered on the long end (4.28x cover), with the 1yr-bill rallying c.30bps into the close.

The OMO space saw an early-week auction with moderate demand on the mid- to long-end (0.75x and 2.3x cover on Jun-16 and Jun-30), clearing at 19.35% and 19.69% respectively, with no sale on the short end. Post-auction trading remained muted into the close. Liquidity held firm throughout the week, closing at a surplus of c.₦6.6tn

Nigerian Equities:

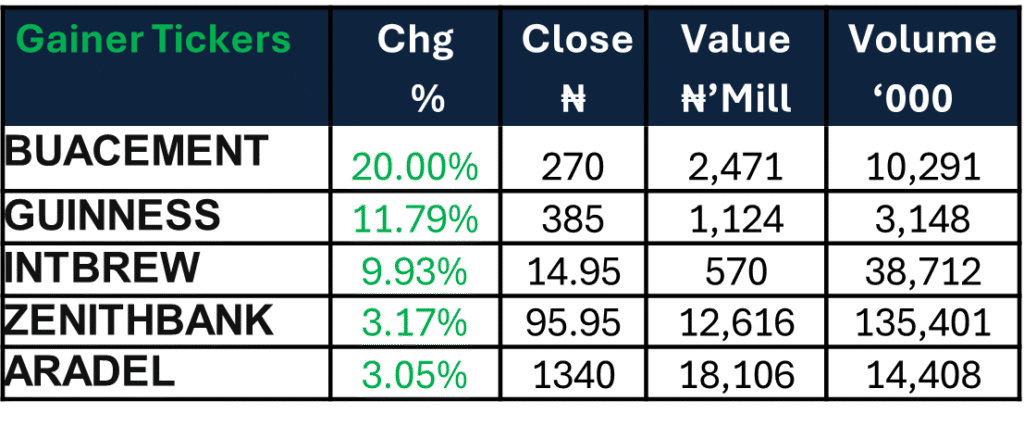

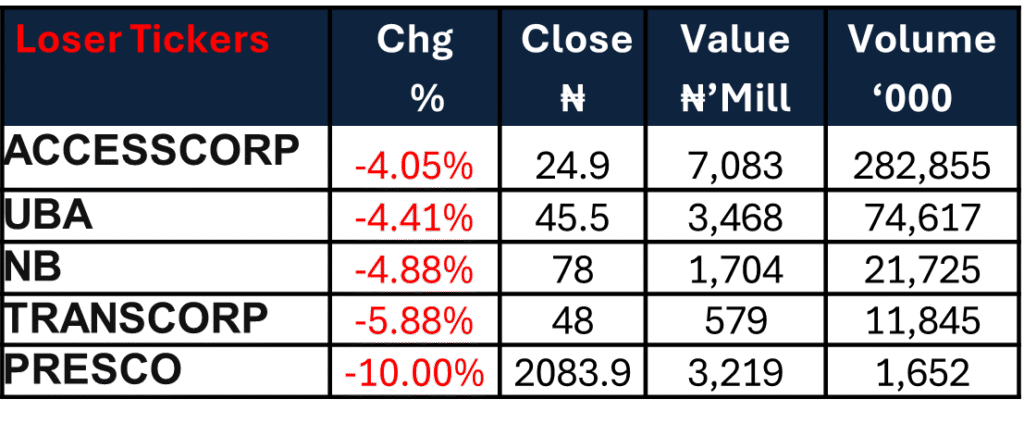

The ASI gained 0.73% WoW to close at 198,407.30, extending the market’s advance. Industrial Goods led sector performance (+5.73%), followed by Oil & Gas (+1.50%), while Insurance (-4.59%) lagged. The move was supported by strong price appreciation in BUA Cement, INTBREW and ARADEL alongside gains in select consumer and healthcare counters.

Bond Auction Result

| 91-day | 182-day | 364-day | |

| Sales (₦‘bn) | 130.741 | 71.368 | 731.811 |

| Stop Rates | 15.95% | 16.65% | 16.72% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.15 | 16.00 | 15 |

| May-33 | 16.05 | 16.00 | 5 |

| Feb-34 | 16.05 | 15.95 | 10 |

| Jan-35 | 16.05 | 15.95 | 10 |

| Jun-53 | 14.10 | 14.10 | – |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 11-Mar-27 | 16.50 | 16.40 | 19.58 |

| 04-Mar-27 | 16.40 | 16.30 | 19.36 |

| 18-Feb-27 | 16.20 | 16.30 | 19.29 |

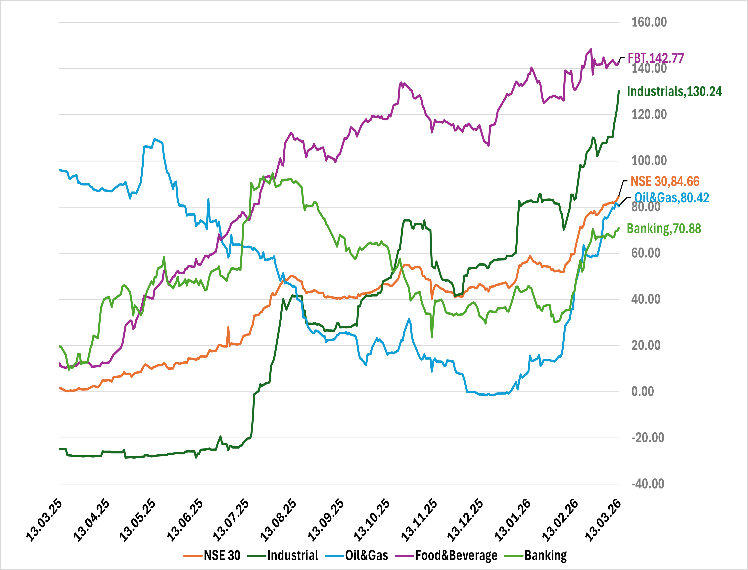

Indices Watch 1-Yr Performance %

NSE 30 : Gainers and Losers

The Week Ahead…

The week is set against a macro backdrop of the February CPI print and the mid-week NTB auction, where the DMO plans to issue ₦1.05tn across tenors against ₦579bn maturing. Liquidity will be further supported by c.₦1.2tn inflows from OMO maturities and FGN bonds (16.2884% Mar-27, 12.40% Mar-36, 19.94% Mar-27, 21.00% Mar-28), alongside the redemption of FGN 21.00% Mar-26. We expect the tone of the week to be driven by the inflation print and auction outcome.

On the equities end, Following the strong YTD rally, positioning may turn more tactical as investors reassess stretched valuations, while breadth points to near-term consolidation and rotation away from weaker financial and insurance names.