Fixed Income in Focus:

The week opened on a risk-off footing amid renewed geopolitical tensions, prompting early profit-taking across instruments. Bond yields gapped 15–20bps higher at the open, with mid-tenor bonds trading in a range 15.95%–16.15% into the close. The T-bill curve repriced c.25–30bps higher ahead of the mid-week auction, which cleared bearish with strong long-end demand (364-day 2.66x bid-to-cover, +83bps vs previous stop). Post-auction activity remained muted, with the long end paper trading c.20bps below the stop.

In the OMO segment, the CBN conducted two consecutive auctions across 7/8-day, 98/99-day and 105/106-day bills, attracting moderate demand (1.19x and 1.63x bid-to-cover). Longer-dated bills cleared at 19.35% and 19.40% amid subdued secondary activity. System liquidity remained ample at ₦5.8tn, anchoring front-end demand despite the broader risk-off tone.

Nigerian Equities:

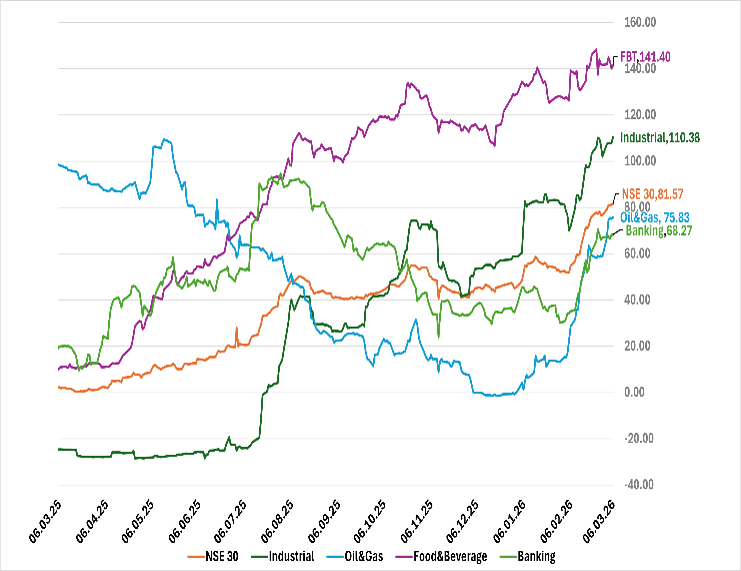

The ASI advanced 2.15% to 196,968.15, reversing the prior week’s pullback. Oil & Gas led gains (+9.43%),then Industrials (+3.89%), while Insurance (-1.88%) lagged. The advance was driven by renewed accumulation in energy names amid escalating Middle East tensions, alongside continued institutional positioning in large caps.

Bond Auction Result

| 91-day | 182-day | 364-day | |

| Sales (₦‘bn) | 64.269 | 91.434 | 856.034 |

| Marginal Rates | 15.95% | 16.65% | 16.73% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 15.75 | 16.15 | 40 |

| May-33 | 15.80 | 16.05 | 25 |

| Feb-34 | 15.60 | 16.05 | 45 |

| Jan-35 | 15.60 | 16.05 | 45 |

| Jun-53 | 14.00 | 14.10 | 10 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 04-Mar-27 | 16.35 | 16.40 | 19.58 |

| 18-Feb-27 | 15.70 | 16.40 | 19.43 |

| 04-Feb-26 | 15.35 | 16.20 | 19.01 |

Indices Watch 1-Yr Performance %

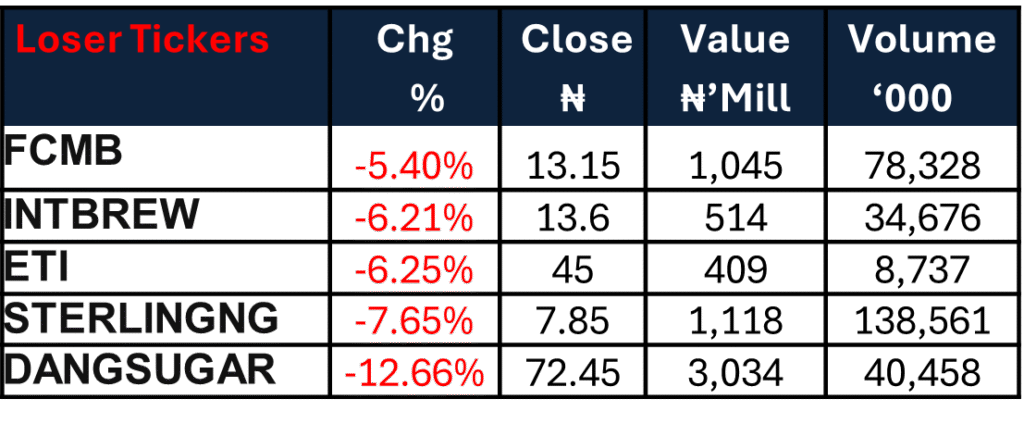

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens ahead of the mid-week T-bill auction, where the DMO is set to issue ₦850bn across tenors against ₦711bn in maturities. We also anticipate ₦688bn in OMO maturities, bringing total expected inflows to c.₦1.4tn this week. Market activity will likely be anchored on the auction print, the possibility of a CBN OMO auction, and broader global risk sentiment. Furthermore, with Brent approaching the $100/bbl., upstream energy names may continue to attract tactical flows given strong earnings visibility and FX-linked revenues. However, with the ASI nearing the 200,000-resistance level, further upside will likely depend on fresh earnings catalysts and sustained institutional liquidity.