Fixed Income in Focus:

The week opened on a bearish note as system liquidity printed at ₦–280bn, prompting a slight rebound in rates across the curve. Midweek, however, sentiment shifted following the June CPI release, which eased by 75bps to 22.22%, reinforcing dovish expectations ahead of next week’s MPC meeting. This drove renewed bullish positioning, with firm demand seen in the NTB market, particularly for the new 9 July and 19 February bills, and in bonds, where activity was concentrated around the 2031s and 2033s. OMO bills also traded during the week, though activity remained relatively measured amid tight liquidity conditions. Liquidity closed the week significantly weaker at ₦–659bn.

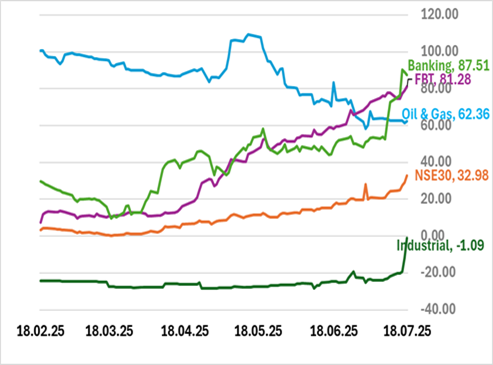

Nigerian Equities:

The All-Share Index continued its bull run to record a 2.57% gain this week. Strong buying interest prevailed though every sector with Banking, NSE30, and Oil & Gas indices leading the way registering 4.69%, 3.33%, and 2.45% respectively. Notably, trading volumes peaked for premium stocks on Thursday as investors rushed to grab value positions in MTNN, Access and GTCO. This likely solidifies a portfolio shift towards equities that should continue into another short trading week.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 16.90 | 16.75 | 15 |

| Feb-31 | 16.70 | 16.10 | 60 |

| May-33 | 16.50 | 15.95 | 55 |

| Jan-35 | 16.45 | – | – |

| Jun-53 | 15.70 | 15.80 | (10) |

| NTB | Bid | Ask | Effective Yield |

| % | % | % | |

| 09-Jul-26 | 15.45 | 15.30 | 17.96 |

| 19-Feb-26 | 16.70 | 16.40 | 18.14 |

| 08-Jan-26 | 16.50 | 16.25 | 17.59 |

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

The week opens with a key macro event, the MPC meeting scheduled for July 21–22th where investors are broadly positioning for a hold, with recent inflation data reinforcing a dovish outlook.

Inflows totalling ₦539bn are expected this week, including FGN bond coupons of ₦89bn (Jan 2042), ₦74bn (Jan 2026), ₦29bn (Jul 2030), and ₦21bn (Jul 2045). An additional ₦326bn in NTB maturities is due on July 24. These inflows should enhance liquidity and support firm demand across the curve. With no other major data due, focus will be on policy direction and post-MPC positioning.