Fixed Income in Focus:

The week opened with robust activity across the curve, supported by firm system liquidity of c.₦1.47tn. With no scheduled auctions, trading was driven by secondary market flows and mid-week CPI, which printed 15.15% (down 218bps vs Nov on the post-rebase series). The T-bill market started the week on a bullish footing, with strong demand compressing rates by c.40bps; the 07-Jan bill traded down into the 17.50–17.60% range into the close. Bonds followed suit, with yields compressing by at least c.25bps across the curve and mid-tenor prints as low as 17.40–17.50%. Late in the week, mild profit-taking and supply caution prompted a modest pullback, with yields edging higher into the close. OMO bills and T-bills opened near parity, but as T-bill yields compressed faster, OMOs lagged and held slightly firmer, led by the 04-Aug at 19.30%. By week-end, liquidity remained supportive, closing stronger at c.₦2.11tn.

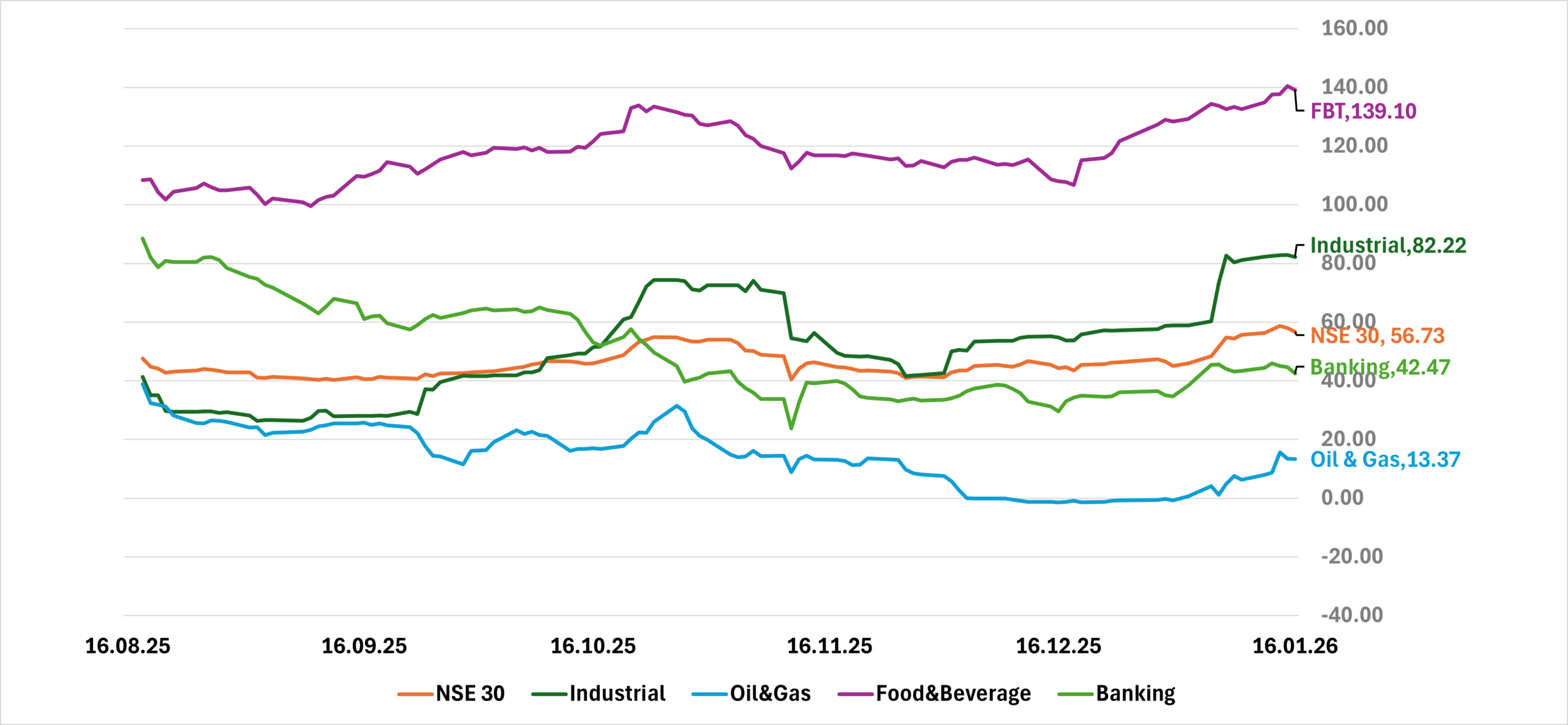

Nigerian Equities:

The ASI gained 2.36% to close at 166,129.50, extending the strong January rally. Led by Oil & Gas (+5.71%) and Banking (+3.45%) on renewed large-cap positioning.Nigeria’s SEC raised capital requirements for brokers, dealers, fund managers, and digital asset firms and Overall momentum remains bullish, though profit-taking risks are building at elevated index levels.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 17.60 | 16.95 | 65 |

| Feb-31 | 17.95 | 17.60 | 35 |

| Jun-32 | 17.95 | 17.70 | 25 |

| May-33 | 17.90 | 17.60 | 30 |

| Jun-53 | 15.50 | 15.00 | 50 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 07-Jan-27 | 17.90 | 17.60 | 21.22 |

| 17-Dec-26 | 17.15 | 16.40 | 19.29 |

| 19-Nov-26 | 16.90 | 17.10 | 19.95 |

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

The week is set against a scheduled Treasury Bill auction, with the DMO expected to issue ₦1.15tn across tenors. This is cushioned by an estimated ₦2.3tn in inflows from T-bill and OMO maturities, alongside coupon payments on the 12.149% Jul-34, 13.00% Jan-42, 12.50% Jan-26, and 10.00% Jul-30 FGN bonds.

We flag the likelihood of an OMO issuance to partly offset the size maturing, with the bond auction circular also likely to be released during the week. Overall, market direction should be driven by auction outcomes, secondary market flows, and any incremental supply signals.