Fixed Income in Focus:

Market opened the week with net liquidity of ₦2.8tn, supporting early buying across the curve. In Treasury Bills, flows were mixed, with demand skewed to the long end (21-Jan and 04-Feb) where early prints cleared at 15.95–16.00%. As the week progressed, mild profit-taking saw the T-bills backup by c.5–10bps, with executions printing around 16.00–16.05%. In FGN Bonds, activity was concentrated in the belly-to-long end (31s/34s/35s), with early executions at 16.45–16.55%. Into the close, sellers dominated and yields backed up by c.10–20bps, with prints firming around 16.65%. Conversely, OMO bills remained bullish, with demand concentrated in the Jan OMOs (12/19), rallying c.25bps as executions tightened to 16.10% into the close. With no primary market activity and only mild secondary flows, system liquidity closed positive at ₦4.3tn.

Nigerian Equities:

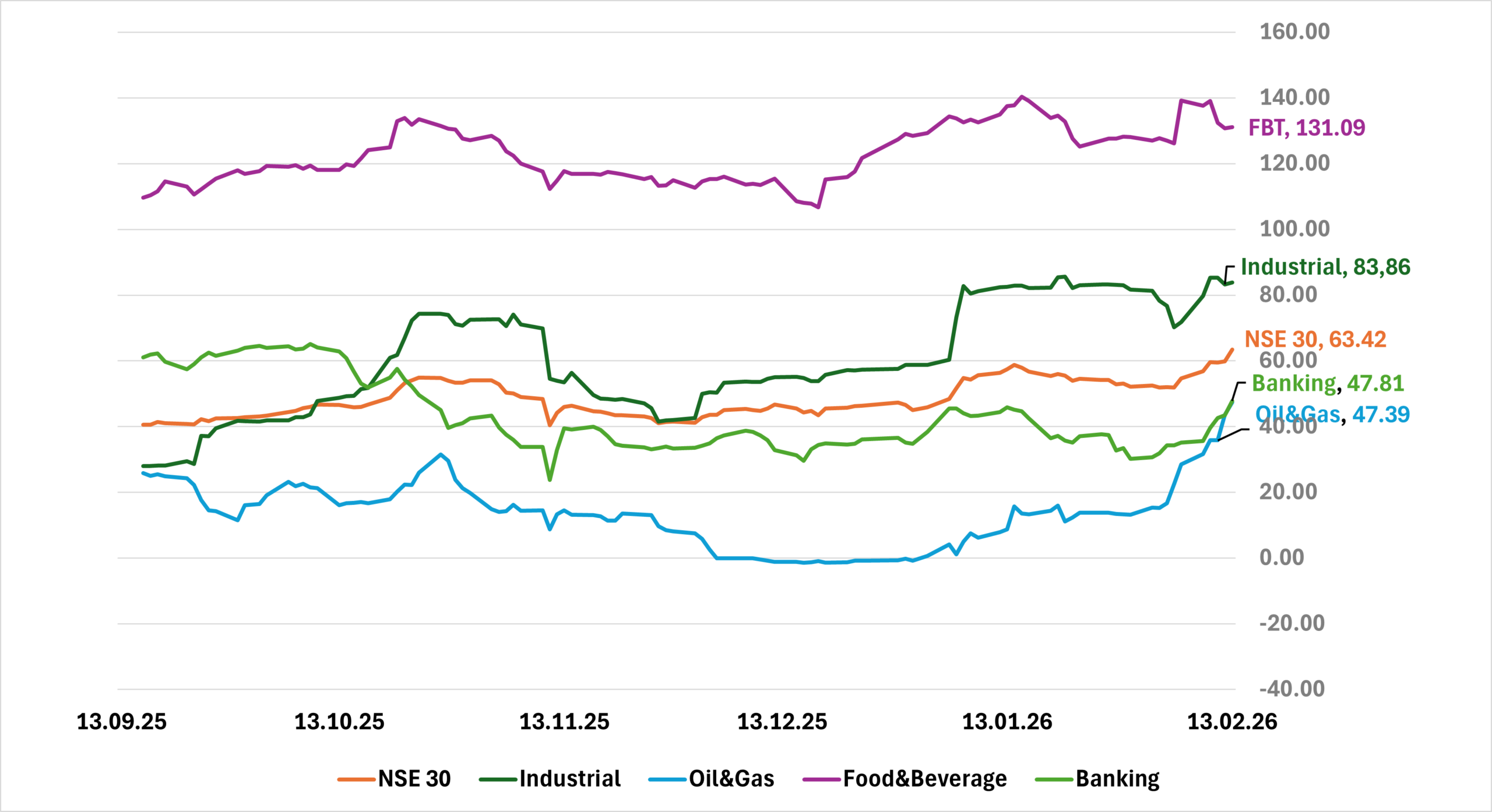

NGX ASI gained 6.16% WoW to 182,313.08, extending strong upside participation. Oil & Gas led with +11.40% followed by Banking +5.84% and Insurance lagged modestly +0.65%. Broad-based flows underpinning the move reflected heightened market activity and sustained buying interest across large caps. We expect flows to stay selective around liquid large caps as investors assess FY earnings momentum driven durability.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.45 | 16.65 | 20 |

| May-33 | 16.50 | 16.70 | 20 |

| Feb-34 | 16.50 | 16.65 | 15 |

| Jan-35 | 16.50 | 16.65 | 15 |

| Jun-53 | 14.40 | 14.50 | 10 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 04-Feb-27 | 16.05 | 16.05 | 19.01 |

| 21-Jan-27 | 16.00 | 16.00 | 18.70 |

| 07-Jan-27 | 16.05 | 15.95 | 18.60 |

Indices Watch 1-Yr Performance %

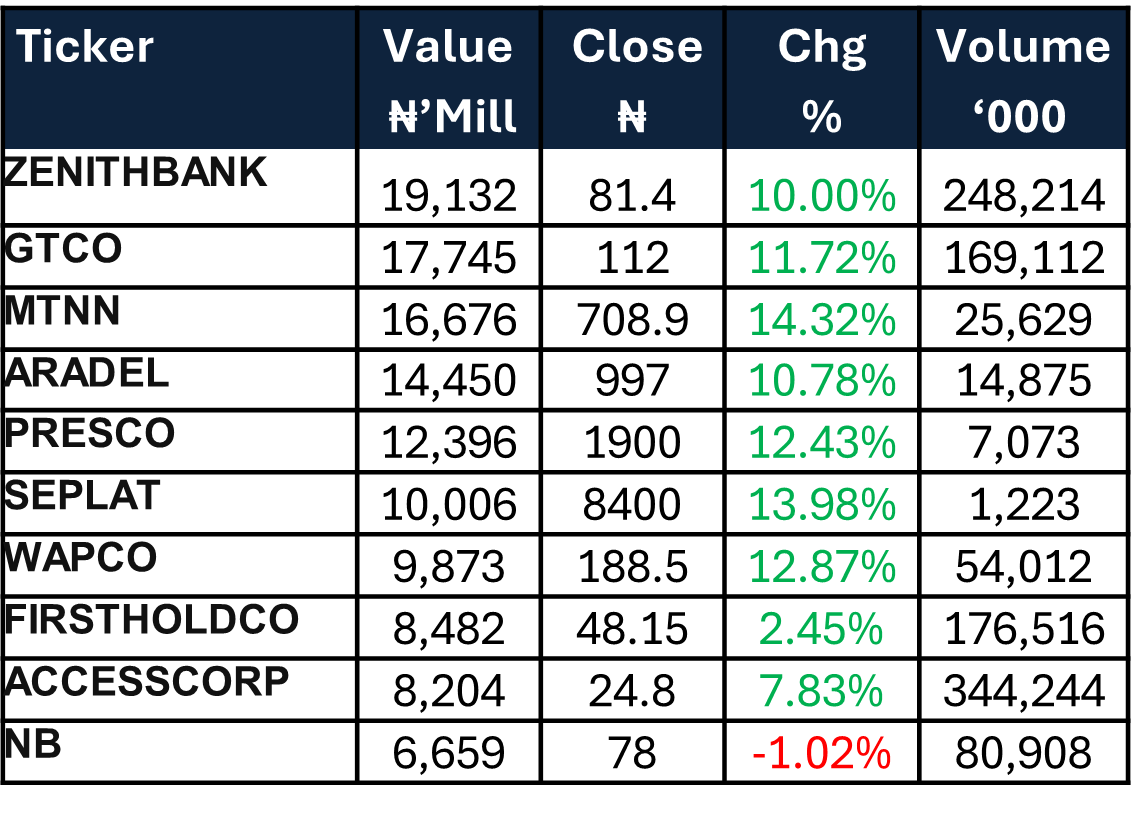

This Weeks Market Movers NGX

The Week Ahead…

The week is set against two key catalysts: the January CPI print and a primary market Treasury Bill auction, where the DMO is scheduled to issue ₦1.15tn across tenors against c.₦766bn in maturities.

We expect the early tone to be anchored by the inflation outcome, with secondary flows remaining cautious as participants position around the data and the liquidity signal. Into the mid-week auction, profit-taking is likely to emerge, pushing yields modestly higher and keeping price action largely positioning-led, with CPI remaining the key directional driver through the auction window.