Fixed Income in Focus:

The market opened the week subdued, with system liquidity firm at ₦4.68tn, as CBN conducted short-dated OMO auctions (8/99-day and 7/105-day), clearing at 22.39% and 19.48% on c.3.8x cover. The T-bills market rallied into the mid-week auction, with demand skewed to the long end as the 365-day (18-Feb) bill cleared c.100bps below the previous print on a strong 5.09x cover. Post-auction, the new 1-year bill opened c.55bps below its stop and traded moderately into the close, with flows settling at 15.45%–15.65%. Bonds remained firm, as mid-tenor (31s/32s/33s/34s/35s) demand drove c.60bps of compression from the open on positioning ahead of a constructive bond auction, with flows settling around 16.05%–16.15% while liquidity closed net surplus at ₦2.15tn.

Nigerian Equities:

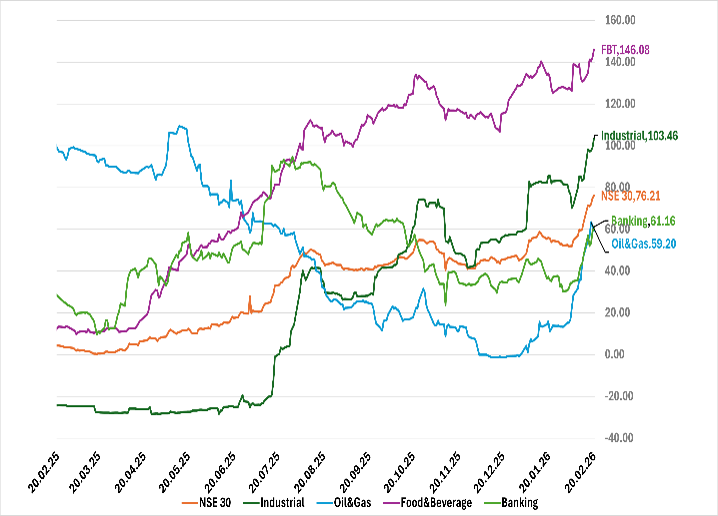

The ASI advanced 6.95% WoW to 194,989.77, with broad-based strength across sectors. Industrials led (+10.10%), followed by Oil & Gas (+8.66%) and Food & Beverage (+6.10%), and Insurance (+4.73%) trailed but remained positive. The rally was liquidity and PENCOM news sentiment driven , anchored by large-cap participation across energy, industrial and financial names.

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 105.050 | 80.610 | 1,710.296 |

| Stop Rates | 15.80% | 16.65% | 15.90% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.65 | 16.00 | 60 |

| May-33 | 16.70 | 16.05 | 65 |

| Feb-34 | 16.65 | 16.05 | 60 |

| Jan-35 | 16.65 | 16.00 | 65 |

| Jun-53 | 14.50 | 14.10 | 40 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 18-Feb-27 | 15.35 | 15.65 | 18.52 |

| 04-Feb-27 | 16.05 | 15.40 | 18.04 |

| 19-Nov-27 | 15.35 | 15.60 | 17.64 |

Indices Watch 1-Yr Performance %

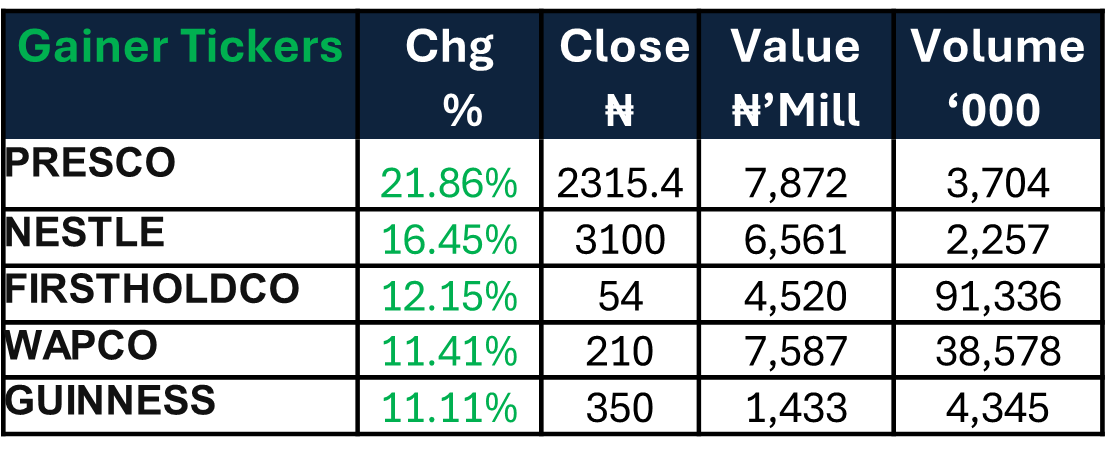

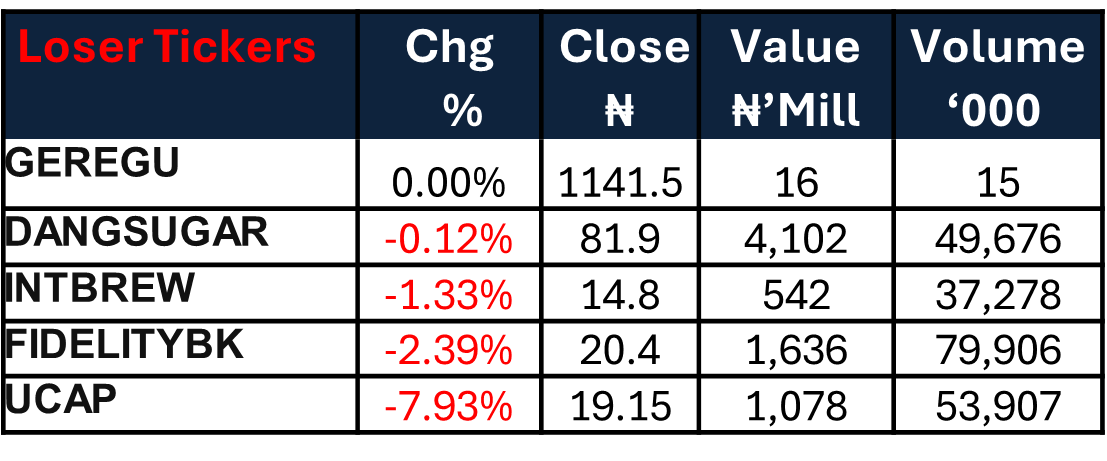

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens with the FGN bond auction in view, where the DMO plans to reopen ₦800bn across the 17.95% Jun-2032s, 19.89% May-2033s and 19.00% Feb-2034s. Liquidity should stay supported by c.₦1.3tn in coupon inflows (Feb-31s, Feb-34s, Feb-28s and Aug-30s) alongside incoming OMO maturities. Set against the 304th MPC, this week’s tone should be driven by the Committee’s outcome and the auction clearing print.

On the equities end, after a near 7% weekly surge and three-week cumulative rally, we expect near-term consolidation with selective rotation, particularly within liquid industrial and energy names.