Fixed Income in Focus:

The week opened quietly, with system liquidity anchored at a ₦4.02tn surplus amid a shortened trading week into year-end. OMO activity led the tone, with 168- and 210-day bills (02-Jun and 21-Jul) trading at 18.95–19.05% ahead of the CBN’s early-week OMO auction. The CBN reissued similar tenors (16-Jun and 28-Jul) and cleared at a 2.11x cover, with stop rates of 19.35% (168-day) and 19.41% (210-day); post-auction demand drove a bullish compression as bills traded down to 19.10–19.20% into the close. The bond market saw a modest uptick in activity despite sticky yields, with buying interest centered on mid-tenors (31s, 32s, 33s), while the Treasury bills market also witnessed significant demand in Nov and Dec bills, where rates compressed by c.30bps as liquidity remained supportive at c.₦3.35tn into the close.

Nigerian Equities:

The ASI rose 1.92% w/w, as gains were led by Insurance(+5.93%),Consumer(+3.44%),and Banking(+2.96%), reflecting rotation into beaten-down financials and consumer names. Market activity remained disciplined, with investors positioning ahead of FY earnings and clarity on macro policy direction. We expect momentum to stay selective and tilted toward financials.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 17.20 | 17.10 | 10 |

| Feb-31 | 17.15 | 17.05 | 10 |

| Jun-32 | 17.10 | 17.15 | -5 |

| May-33 | 17.05 | 17.00 | 5 |

| Jun-53 | 15.00 | 15.00 | – |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 17-Dec-26 | 16.80 | 16.30 | 19.30 |

| 03-Dec-26 | 16.60 | 16.30 | 19.16 |

| 19-Nov-26 | 16.60 | 16.30 | 19.02 |

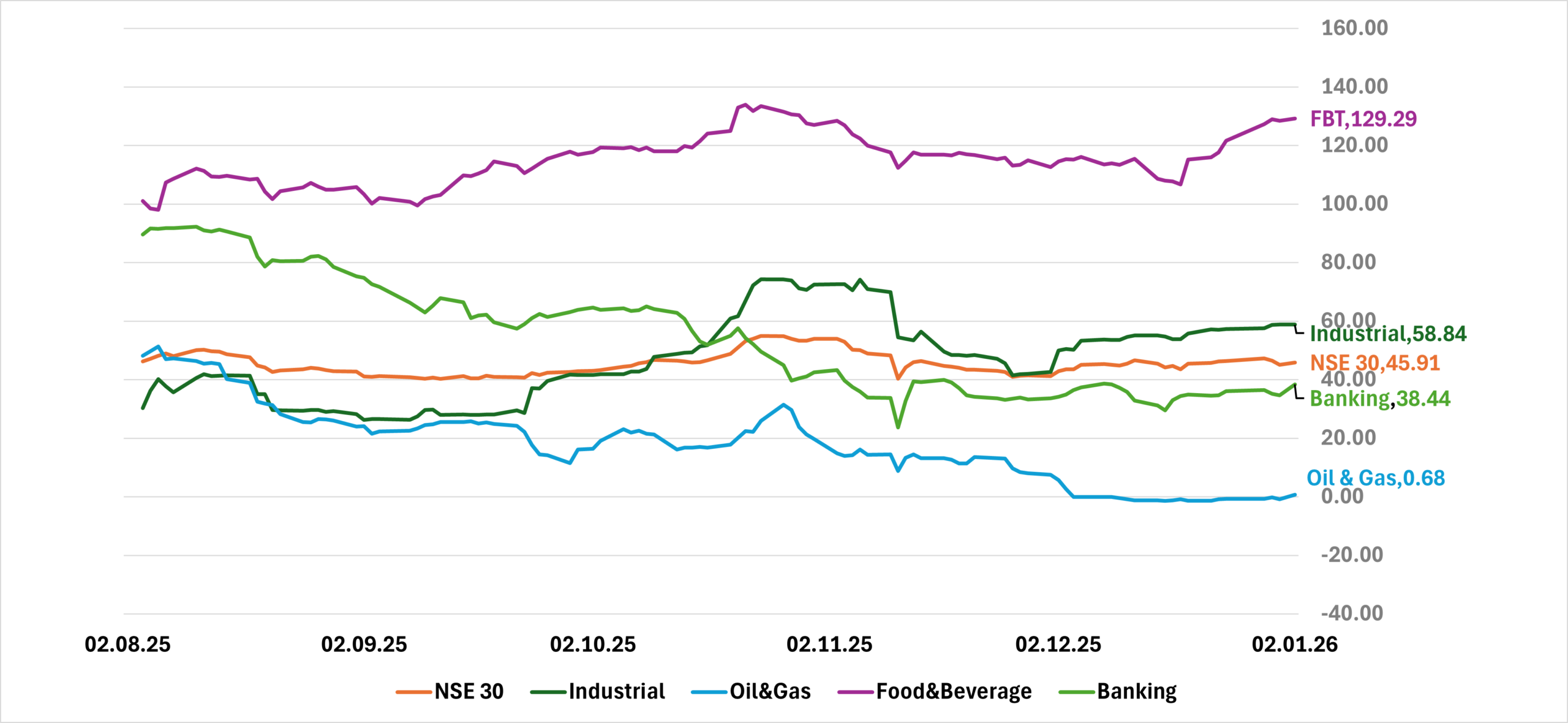

Indices Watch 1-Yr Performance %

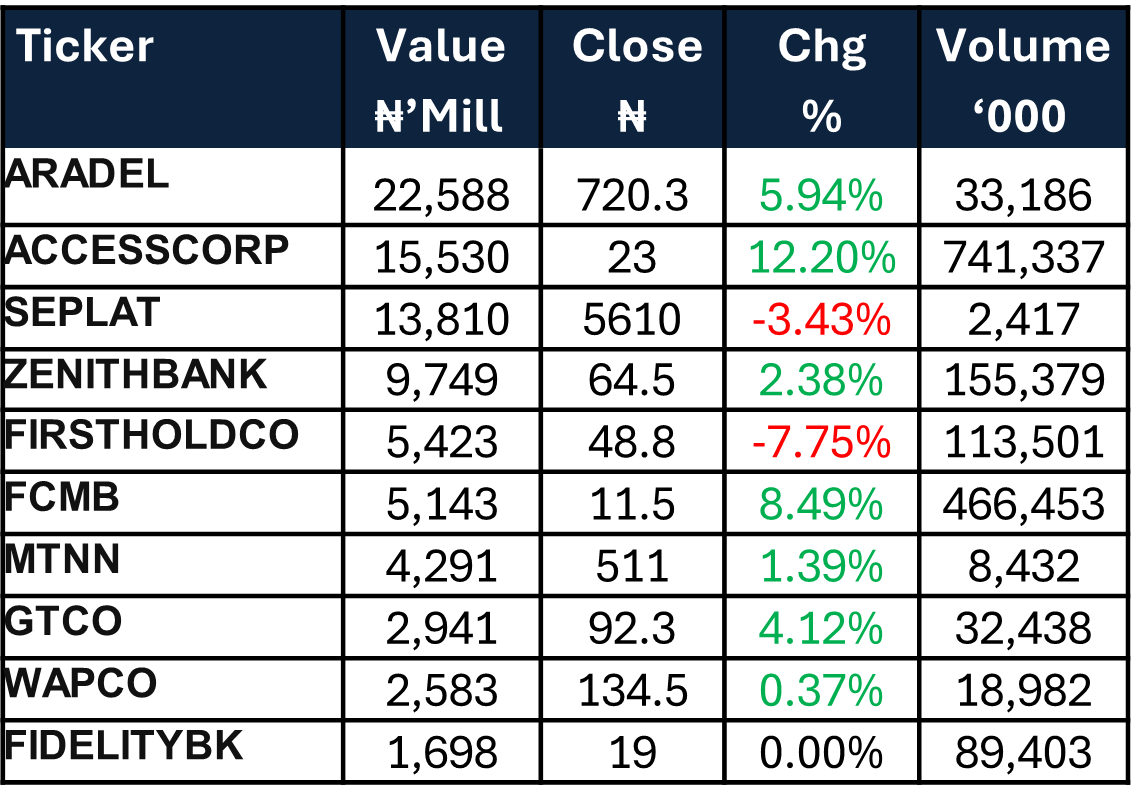

This Weeks Market Movers NGX

The Week Ahead…

The week is set against a quiet macroeconomic calendar, with no guidance yet on the Q1 auction calendar. We expect liquidity inflows of c. ₦864bn from NG OMO and T-bill maturities, keeping system liquidity comfortable and supportive of bid appetite.This backdrop raises the likelihood of a mid-week Treasury bill and/or OMO auction, as the CBN may seek to mop up excess liquidity.

Overall, we expect a more active week into the new year, with flows and pricing largely guided by auction supply, stop rates, and the liquidity environment.