Fixed Income in Focus:

The week opened quietly amid shortened trading days(Mon-Wed) due to the seasonal holidays, with system liquidity ample at ₦2.15tn. The CBN conducted an early-week OMO auction which closed with a strong 2.88x total cover, as stop rates on the 162-day and 211-day OMO bills printed at 19.38% and 19.42%, respectively. Post-auction, bullish sentiment followed, with OMO rates compressing to and settling in the 19.05 –19.15% range. The T-bill market extended its bullish run, with December bills seeing executions at 16.65 –16.95% into the close. Meanwhile, bond market activity remained muted, with only pockets of demand in the mid-tenor papers (31s, 32s, and 33s). By the close, system liquidity held firm at ₦3.89tn.

Nigerian Equities:

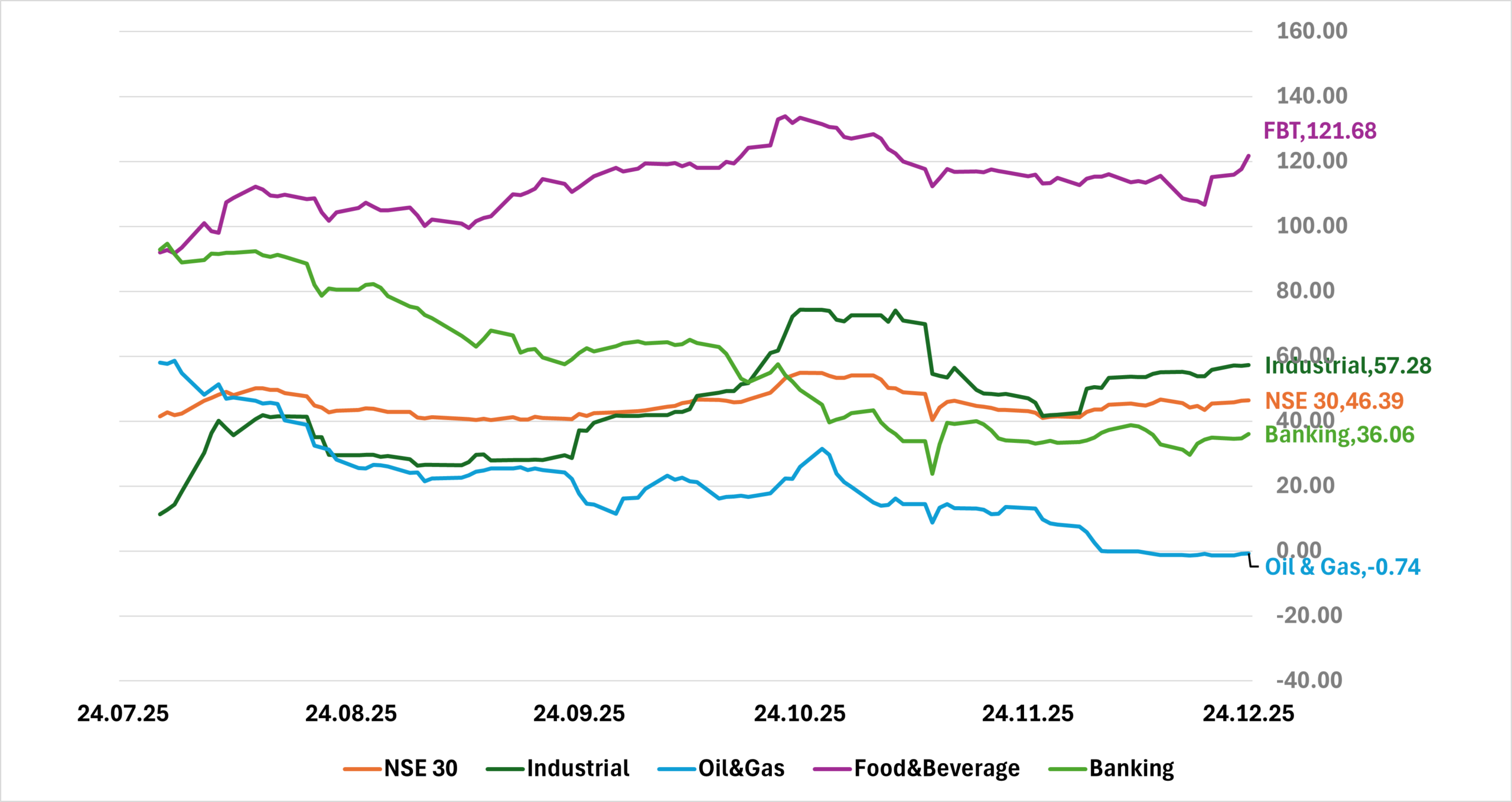

The ASI rose 0.97% to 153,539.83, extending the year-end rebound. Gains were driven by Consumer goods (+3.34%) and Banking (+2.93%), reflecting renewed positioning in consumer and financial heavyweights. Insurance declined (-2.13%) on profit-taking. Overall sentiment remained positive but selective into the holiday-shortened week.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 17.20 | 17.20 | – |

| Feb-31 | 17.15 | 17.15 | – |

| Jun-32 | 17.10 | 17.10 | – |

| May-33 | 17.05 | 17.05 | – |

| Jun-53 | 15.00 | 15.00 | – |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 17-Dec-26 | 16.80 | 16.70 | 19.93 |

| 10-Dec-26 | 16.70 | 16.60 | 19.71 |

| 03-Dec-26 | 16.60 | 16.60 | 19.64 |

Indices Watch 1-Yr Performance %

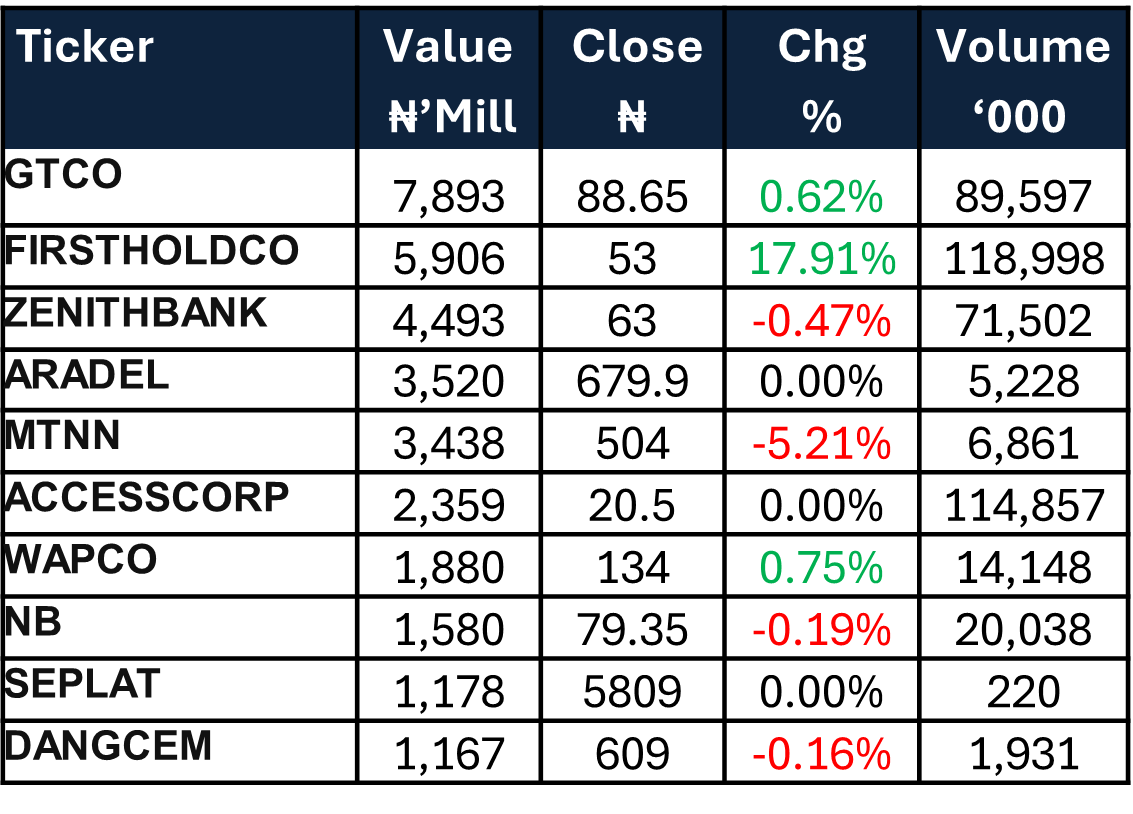

This Weeks Market Movers NGX

The Week Ahead…

The week is set against a quiet macroeconomic trading calendar and no scheduled auctions. On the liquidity front, we expect an inflow of c.₦424bn from 13.00% FGNSK-31s coupon payments alongside maturities in 15.74% FGNSK-25s and OMO bills; however, with the year drawing to a close, we anticipate lighter flows and muted risk appetite as participants square books.

Overall activity should remain subdued as the market awaits clearer forward guidance, digests the 2026 budget, and looks into next week’s restart of more typical trading conditions.