Fixed Income in Focus:

The week opened with surplus liquidity of ₦2.58tn ahead of the early-week FGN bond auction (2030s and 2032s re-openings), which cleared +130bps above previous marginal rates but below forecast, printing 1.56x and 1.48x cover. Monday’s inflation print showed a continued disinflation trend, with November headline CPI easing 160bps to 14.45%, supporting early-week sentiment. Post-auction, the modest uptick in stop rates sparked a mild bullish rally in mid-tenor bonds that held into the close. Mid-week, the NTB auction cleared bullish on the long end (-44bps vs previous stops) on a c.0.99x cover, with post-auction demand focused on the new issue and December bills, tightening by at least 25bps. In OMO, trading focused on 9 Jun and 14 Jul papers, with executions at 18.60–18.80%, while liquidity remained supportive at ₦3.28tn.

Nigerian Equities:

The ASI rose 1.76% to 152,057.38, extending year-end gains as risk appetite improved. Banking (+2.75%) and Consumer Goods (+4.51%) led the rally, driven. Market strength was supported by FirstHoldCo, alongside consumer large caps.We expect sentiment to remain constructive against 2026 but selective, with flows favouring liquid large-caps ahead of year-end positioning.

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 100.013 | 22.067 | 581.994 |

| Stop Rates | 15.50% | 15.95% | 17.51% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 17.40 | 17.20 | 20 |

| Feb-31 | 17.40 | 17.15 | 25 |

| Jun-32 | 17.25 | 17.10 | 15 |

| May-33 | 17.15 | 17.05 | 10 |

| Jun-53 | 15.00 | 15.00 | – |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 17-Dec-26 | 17.25 | 16.80 | 20.15 |

| 10-Dec-26 | 16.65 | 16.70 | 19.93 |

| 03-Dec-26 | 16.85 | 16.60 | 19.71 |

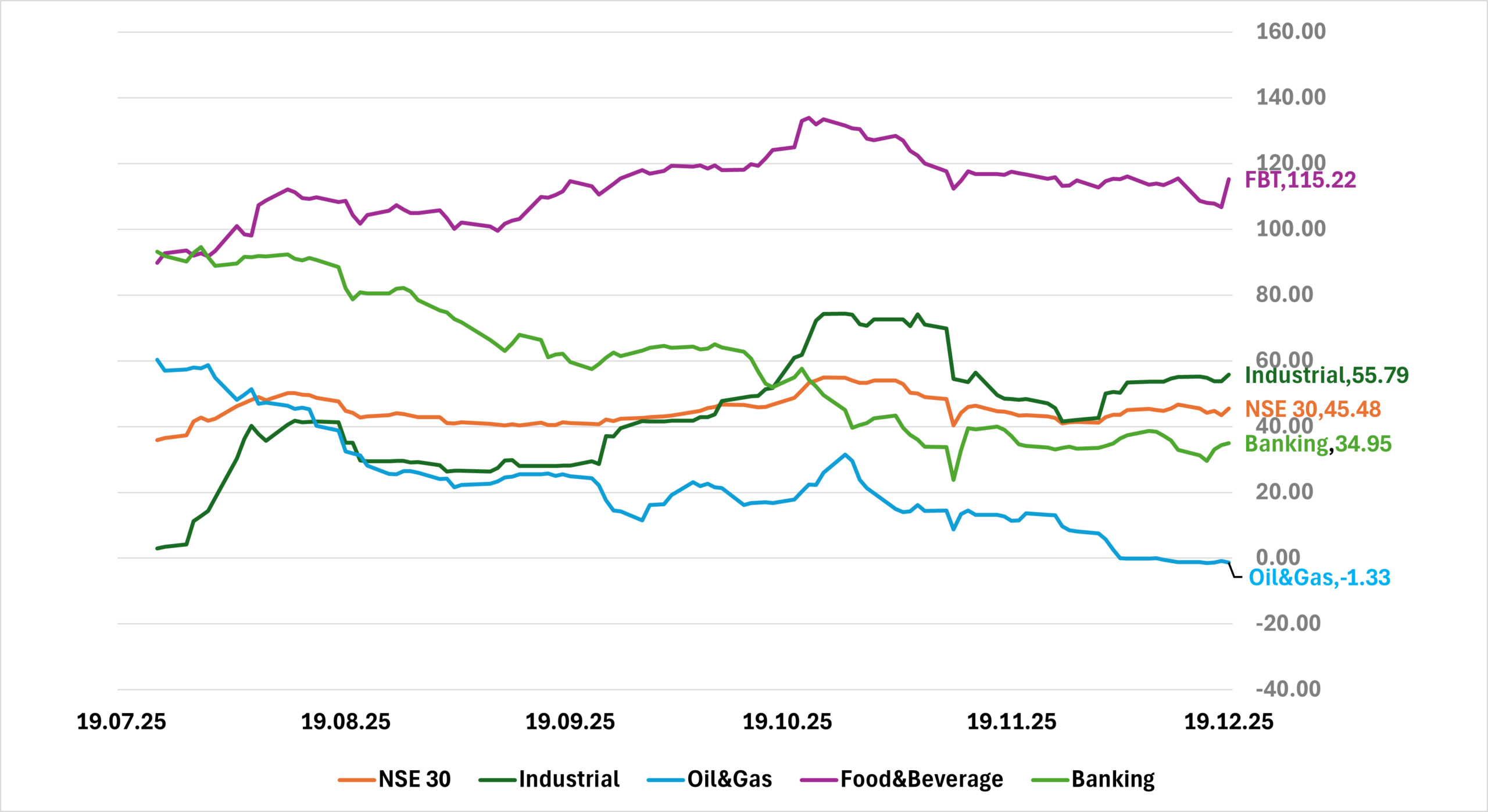

Indices Watch 1-Yr Performance %

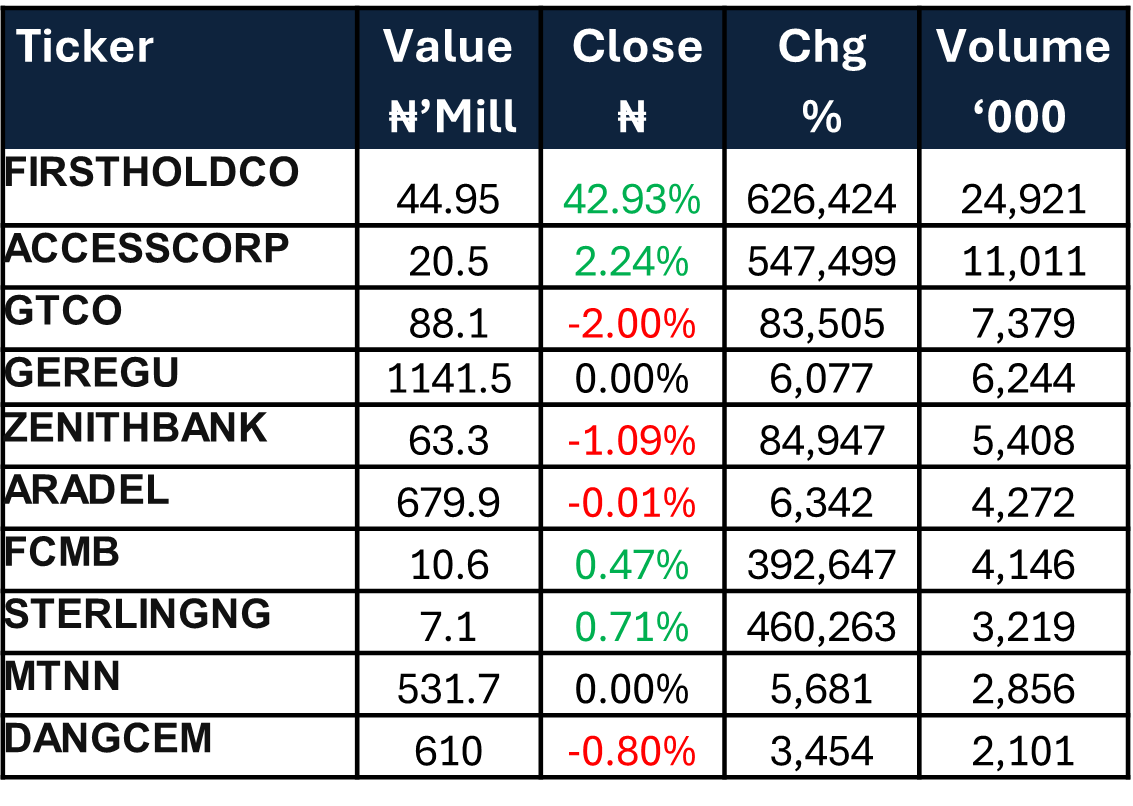

This Weeks Market Movers NGX

The Week Ahead…

The week is set against a quiet macro calendar and no scheduled auctions, keeping attention on liquidity conditions and positioning flows. We expect inflows of ₦467bn from NGOMO maturities and coupon payments on the FGN 2033s, 38s and 53s, which should keep system liquidity supportive. That said, the size of the inflows leaves open the possibility of an OMO auction, which could absorb part of the excess liquidity.

Activity is likely to remain subdued due to the shortened trading week. We anticipate some early-week repositioning and year-end book-closing, with price action largely driven by two-way flows rather than fresh supply catalysts.