Fixed Income in Focus:

The week opened with active bond and OMO auctions, drawing strong interest across the curve. The DMO’s over allotment, the first in over a month, dampened demand for domestic debt and drove more profit taking activities in the secondary market. Bearish activity persisted towards the close of the week as we saw a rebound in yields across the yield curve. The 17-Feb OMO cleared at a yield of 27.36%, traded as low as 25.90% before closing the week at 26.60%. Despite the primary market issuance on bonds and OMOs, the week closed with an ample liquidity, at ₦1.5 trillion.

Nigerian Equities:

The All-Share Index hits all-time high of 141,263.05, gaining 5.07% this week. Trading activity spiked amid positive H1 results. Large PAT gains from cement manufacturers caused a surge in demand leaving the sector 10.12% higher. Majority of premium stocks met H1 expectations driving a further 5.13% of appreciation for NSE30. We expect further digestion of results to guide activity this week with a hint of profit taking.

Bond Auction Result

| 19.30%2029 | 17.95%2032 | |

| Sales (₦‘bn) | 13.43 | 172.50 |

| Marginal Rates % | 15.69 | 15.90 |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 16.15 | 16.50 | (35) |

| Feb-31 | 16.00 | 16.65 | (65) |

| May-33 | 15.95 | 16.65 | (70) |

| Jan-35 | 15.80 | 16.30 | (50) |

| Jun-53 | 15.60 | 15.80 | (20) |

| NTB | Bid | Ask | Effective Yield |

| % | % | % | |

| 23-Jul-26 | 15.20 | 15.90 | 18.80 |

| 04-Jun-26 | 15.95 | 16.30 | 18.87 |

| 23-Apr-26 | 16.50 | 16.75 | 18.59 |

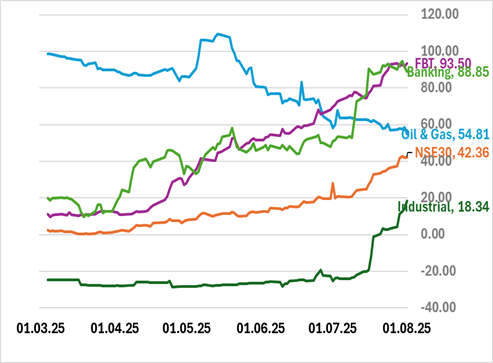

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

The market expects an NTB auction this week, where the DMO on behalf of the FG plans to issue ₦220 billion across tenors, against ₦258 billion in maturities. We expect rates to close higher than the previous discount rates given the recent pull-back in the secondary markets.

With no major macro data expected, Fund Managers may also remain cautious ahead of early-month positioning and signals from the monetary authorities. We think new levels in both the primary and secondary markets will be tested this week and create potential for new buyers to add risk to their positions.