Fixed Income in Focus:

The week opened quietly following the Easter public holiday, with mixed activity across the curve as system liquidity remained supportive at ₦6.2tn, underpinning early demand. In the T-bills segment, interest was skewed to the long end ahead of the auction, which subsequently cleared bullish, with the 364-day bill recording a 5.27x cover and pricing 23.1bps through prior levels. Post-auction, unmet demand drove a further 25–35bps compression, with yields settling around 15.80% by the close.

In the bond space, sentiment was similarly constructive, with flows concentrated in the mid-tenors and yields holding within a 5–10bps range of the week’s open, maintaining a slight bullish tilt as attention turns to next week’s inflation print. Towards the close, the CBN conducted an OMO auction clearing 19.91% and 19.89% (138/68-day), with demand skewed to the long end, while post-auction trading remained slightly bullish, supported by firm liquidity at c.₦4.8tn by close.

Nigerian Equities:

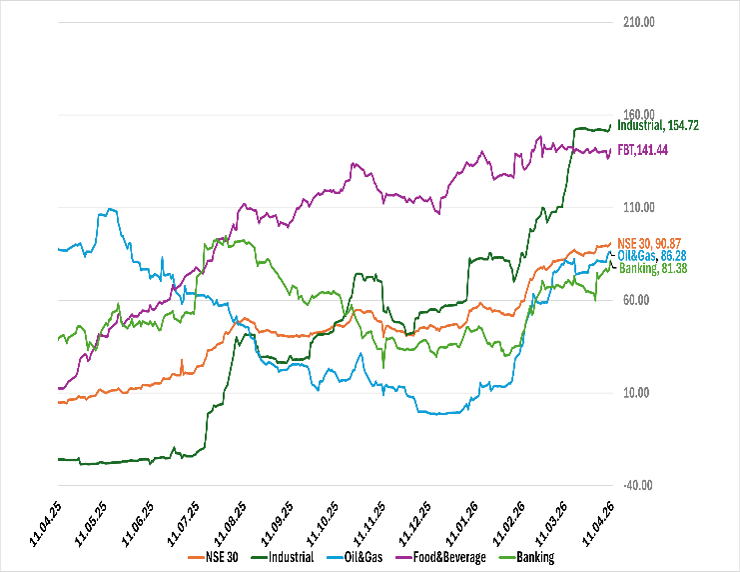

The ASI advanced 1.03% WoW, with gains broad-based. Banking led (+5.10%), followed by Oil & Gas (+2.67%), while Insurance (-3.65%) lagged. The market was driven by renewed demand in financial heavyweights, with support from Oil&Gas and improved risk appetite. Price action suggests continued selective accumulation in liquid names

NTB Auction Result

| 91-day | 182-day | 364-day | |

| Sales (₦‘bn) | 94.823 | 87.049 | 549.504 |

| Stop Rates | 15.95% | 16.19% | 16.199% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.40 | 16.30 | 10 |

| May-33 | 16.40 | 16.34 | 6 |

| Feb-34 | 16.25 | 16.15 | 10 |

| Jan-35 | 16.30 | 16.20 | 10 |

| Jun-53 | 15.00 | 15.00 | – |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 08-Apr-27 | 15.95 | 15.80 | 18.73 |

| 25-Mar-27 | 16.05 | 15.85 | 18.66 |

| 18-Mar-27 | 16.10 | 15.85 | 18.60 |

Indices Watch 1-Yr Performance %

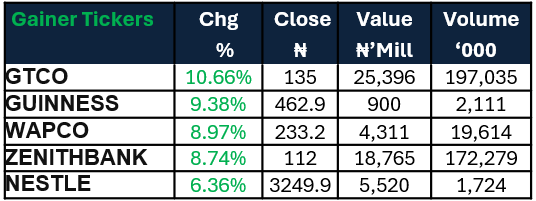

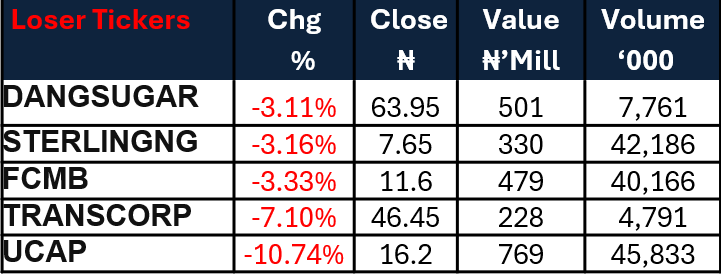

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens with focus on the March CPI print, where a higher reading is expected amid global tensions and a risk-off backdrop. We anticipate c.₦1.46tn in inflows from 15.75% Oct 2033s and 19.3% Apr 2029s coupons alongside OMO maturities, providing liquidity support, with activity likely to be driven by the inflation outcome and secondary market demand dynamics.

For equities, we expect banking names to remain supported by dividend positioning and corporate action flows, with the upcoming inflation print likely to shape near-term market direction.Early positioning ahead of Q1 earnings should sustain selective demand in financial and energy names.