Discussion Point:

Nigeria’s $4.6bn balance-of-payments surplus eases short-term FX pressure, but persistent services and income outflows show that external stability remains fragile rather than structural.

Nigeria’s return to a $4.6bn balance-of-payments (BOP) surplus in Q3 2025 is a welcome development. According to the recent Central Bank of Nigeria press release, the surplus was supported by stronger export earnings, resilient diaspora remittances, renewed capital inflows, and an increase in external reserves toward $43bn. This matters because a balance-of-payments surplus means foreign currency inflows exceeded outflows during the quarter. This gives the FX market more liquidity, reduces immediate pressure on the naira, and allows the Central Bank to rebuild buffers rather than defend the currency aggressively as a result, market confidence improves.

But BOP numbers are not just about how much foreign exchange comes in. They are about how long it stays in the system. And once we look beneath the headline, the structure of Nigeria’s external accounts tells a more interesting story.

What Drove the Q3 Improvement

The composition of the goods account explains why the surplus strengthened in Q3. Crude oil exports increased to $8.45bn from $7.66bn in Q2, reflecting improved production, pricing and reinforcing oil’s continued role as Nigeria’s primary source of FX inflows. At the same time, exports of refined petroleum products rose sharply to $2.29bn, up from $1.59bn in the previous quarter. This increase is particularly important because it signals a gradual shift away from exporting only crude oil toward exporting higher-value refined products.

On the import side, refined petroleum product imports declined to $1.65bn, down 12.7% quarter-on-quarter, easing one of Nigeria’s most persistent sources of FX demand. This combination of higher refined product exports and lower refined fuel imports marks a meaningful change in trade dynamics, as the country gradually moves from being a net importer of refined petroleum products toward a net exporter. However, the broader picture remains uneven. Non-oil exports declined slightly, while non oil imports rose, underscoring that the improvement in the goods account is still concentrated in the energy segment rather than broadly diversified across the economy.

What the Numbers Are Showing Us

| Item | Q3 2025 ($ bn) | Q2 2025 ($ bn) | Change (%) |

|---|---|---|---|

| Crude Oil Export | 8.45 | 7.66 | 10.31 |

| Gas Exports | 2.31 | 3.31 | -30.21 |

| Refined Petroleum Product Exports | 2.29 | 1.59 | 44.03 |

| Non-oil Exports | 2.19 | 2.34 | – 6.41 |

| Crude Oil Imports | 1.58 | 1.04 | – 51.92 |

| Refined Petroleum Product imports | 1.65 | 1.89 | – 12.70 |

| Non-oil imports | 7.08 | 6.68 | – 5.99 |

Source: CBN Q3 BOP report

Why Goods Strength alone is not Enough

Exporting more refined products and importing less fuel strengthens the trade balance and improves FX inflows. However, this alone does not guarantee external stability. A clear case occurred in 2022, when higher oil prices and stronger goods exports temporarily improved Nigeria’s trade balance, yet FX pressure persisted as large services payments and income outflows continued. Despite positive goods trade, external conditions remained fragile because FX earned from exports quickly flowed back out through services imports and profit repatriation.

FX Quietly Leaks through Services and Income payment

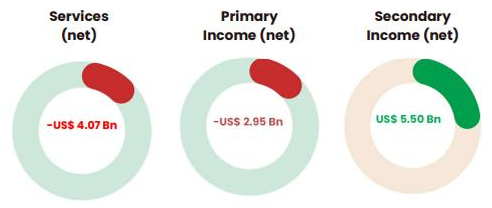

The surplus looks strong on the surface, but it remains fragile because a large amount of FX continues to leave the system through services and income payments. While Nigeria earns FX from exports, it also spends heavily on services that are paid for in foreign currency.

In Q3 2025, net payments for services increased to –$4.07bn, up from –$3.74bn in Q2. This means more FX was spent on items such as transportation, travel, insurance, technical services, and offshore support. At the same time, the primary income deficit widened to –$2.95bn, as foreign investors repatriated a larger share of profits and investment income. Together, these outflows explain why FX earned through trade does not stay in the economy for long, even during surplus periods.

Other Current Accounts Components in Q3 2025

Source: CBN Q3 BOP report

To make this relatable, think of Nigeria as a business that earns more revenue but outsources most of its operations. Sales increase, but shipping, insurance, consultants, software subscriptions, and logistics are all paid in foreign currency. Cash flows in and then flows straight back out.

The income account shows two very different types of FX flows. Primary income reflects returns earned by foreign investors operating in Nigeria, including profits, dividends, and interest payments. As confidence improves and capital flows return, these investors earn more and repatriate part of their earnings. In Q3 2025, this pushed the primary income balance further into deficit. This is a normal feature of an open economy, but it also means that FX inflows linked to investment activity tend to leave the system once profits are realized.

Secondary income, on the other hand, consists mainly of diaspora remittances. These are one-way transfers that do not create future repayment obligations. In Q3 2025, remittances delivered a $5.50bn surplus, once again acting as a stabilizing buffer for the current account. Nigerians abroad sending money home for school fees, rent, healthcare, and family support help anchor the external position because this FX is spent locally and does not flow back out in the form of profit or interest payments. Put simply: Nigeria earns FX, but services and income outflows determine how long that FX stays around.

Why This Matters for Equity Traders and Investors

For equity market participants, the structure of the BOP matters more than the headline surplus. FX stability driven by oil exports, remittances, and foreign inflows tends to be temporary. When inflows pick up, the naira usually stabilises and equity market sentiment improves. This was evident in 2023, when FX reforms and renewed foreign inflows briefly lifted market confidence and supported equity prices. However, the calm did not last, as ongoing demand for FX to pay for services quickly resurfaced and pressure on the currency returned. This is why periods of FX stability are often followed by renewed stress.

Second, not all equities benefit equally from a BOP surplus. Companies with heavy exposure to imported services like aviation, shipping, logistics-intensive manufacturing, and firms reliant on offshore technical support remain vulnerable to FX swings even during surplus periods. Margin expansion for these businesses remains conditional.

On the other hand, companies that replace imported services with local alternatives are better positioned over the long term. In Nigeria, this includes local logistics and construction firms such as Julius Berger, domestic insurance companies like AIICO, NEM and Custodian, and banks and payment platforms such as GTCO and Zenith Bank that handle transactions locally. In the digital space, telecom operators like MTN Nigeria and Airtel Africa also play an important role by providing local data and communication services. These companies help keep foreign exchange within the economy rather than sending it abroad. Over time, this makes their earnings more resilient and supports stronger valuations.

Third, the services deficit explains why foreign portfolio flows into Nigerian equities remain tactical. Capital comes in quickly when sentiment improves and exits just as quickly when uncertainty returns. For traders, this reinforces the importance of liquidity, timing, and disciplined exits rather than buy and-hold positioning based solely on macro headlines.

The Structural Fix Nigeria Needs

If Nigeria wants BOP surpluses to become durable rather than episodic, the services account must change. Countries with more resilient external positions did not achieve it through goods exports alone. India, for example, consistently runs large services surpluses through IT, business process outsourcing, and professional services, which offset its goods trade deficit (IMF Balance of Payments Statistics). Rwanda has deliberately built FX-earning capacity around logistics efficiency, tourism, and conference services, reducing reliance on volatile commodity cycles (World Bank Services Trade Indicators). Egypt has diversified FX sources across tourism, logistics, manufacturing, and services to reduce single-sector risk.

Nigeria’s challenge is not scale, it is structure. Reducing dependence on imported transport, insurance, digital infrastructure, and professional services would keep more FX onshore and make future surpluses more resilient.

Conclusion

Nigeria’s $4.6bn BOP surplus is real and positive, but it is not yet structural. Goods exports and remittances are doing the heavy lifting, while services and income outflows quietly drain FX as activity improves. Until Nigeria earns FX from services as deliberately as it spends on them, external stability will remain conditional.

For investors, the message is clear: trade the improvement, but price the structure.

Kindly find the Report Below

Thanks for reading.