Our latest report unpacks Nigeria’s $21.5 billion financing plan, tracing its path from debt obligations to development opportunities. It highlights the strategies, risks, and potential impacts shaping the nation’s fiscal outlook.

Key Points

- The borrowing plan reflects a structural shift from costly Euro bonds to concessional, project-tied financing aimed at infrastructure and economic recovery.

- Nigeria’s debt remains moderate relative to peers, but investor confidence hinges on execution discipline, reform alignment, and transparent delivery.

Overview of the Borrowing Plan

On July 23, 2025, Nigeria’s Senate approved President Bola Tinubu’s external borrowing proposal amounting to over $21 billion, marking a significant fiscal step aimed at closing the budget deficit for the 2025 fiscal year. The borrowing package includes multiple currency components, reflecting diversified funding sources: €4 billion (approx. $4.7 billion), ¥15 billion (approx. $102 million), a $65 million grant, and up to $2 billion in dollar-denominated domestic borrowing. This move is part of Nigeria’s broader Medium-Term Expenditure Framework (MTEF), designed to support critical developmental goals while maintaining macroeconomic stability.

The funds are targeted toward vital sectors that drive economic transformation, including:

• Infrastructure: particularly large-scale transport projects

•Healthcare: investments in equipment, workforce, and facilities

•Education: school rehabilitation and teacher development

•Security: to stabilize regions affected by unrest

•Housing: with a focus on social housing schemes

A key highlight is the allocation of $3 billion for reviving the 2,044 km Eastern Rail Corridor, linking Port Harcourt to Maiduguri. This is expected to spur intra-regional trade and open up neglected economic zones, particularly in the North-East.By securing longer-term, concessional funding through bilateral and multilateral channels, the Tinubu administration aims to balance the need for development with debt sustainability.

What This Means for Markets

The approval of Nigeria’s external borrowing plan has immediate implications for financial markets, inflation expectations, and investor confidence. It underscores a trade-off between accessing affordable capital and managing exposure to foreign exchange and debt sustainability risk. To simplify this dynamic, the table below compares external vs. internal borrowing across three key dimensions:

| Factor | External Borrowing | Internal Borrowing |

|---|---|---|

| Interest Rates | Often lower due to concessional terms with longer repayment windows | Higher rates due to inflation, tight liquidity, and competition for local capital |

| FX Impact | Strengthens reserves in the short term, but introduces FX repayment risk long term | FX-neutral since Naira-denominated, but provides no buffer to stabilize the currency |

| Inflation Risk | Minimal direct impact on prices, as funds are externally sourced | Can stoke inflation if CBN monetizes deficits or local borrowing exceeds capacity |

Historical Comparison and Strategic Shift

Nigeria’s current $21.5 billion borrowing strategy marks a clear shift toward more disciplined, growth-oriented financing. Unlike the 2021 Eurobond issuance of $4 billion at yields of 6.125–8.25%, which raised servicing costs and heightened FX risk, the 2025–2026 plan prioritizes concessional loans from partners such as the World Bank, AfDB, JICA, and China Exim Bank. This pivot comes alongside recent successes in debt management, including the full repayment of the $3.4 billion IMF COVID-19 facility by April 2025 and the servicing of $1.4 billion in external debt in Q1 2025 much of it at low multilateral rates, reinforcing Nigeria’s commitment to fiscal discipline and creditworthiness.

This strategy offers:

•Lower interest rates and longer maturities

•Grace periods that ease near-term repayment pressure

•Reduced rollover and currency risk over time.

Compared to previous borrowing which often plugged fiscal gaps, the current plan is more targeted and developmental. Key allocations within the approved package include : $1.08 billion from the World Bank for stimulus and education and $652 million from China Exim Bank for priority transport infrastructure. By focusing on productivity-enhancing sectors rather than recurrent spending, this strategy positions Nigeria to unlock long-term economic value while keeping debt sustainable. In this sense, it is not only better structured than past approaches it is relatively good, provided execution remains disciplined.

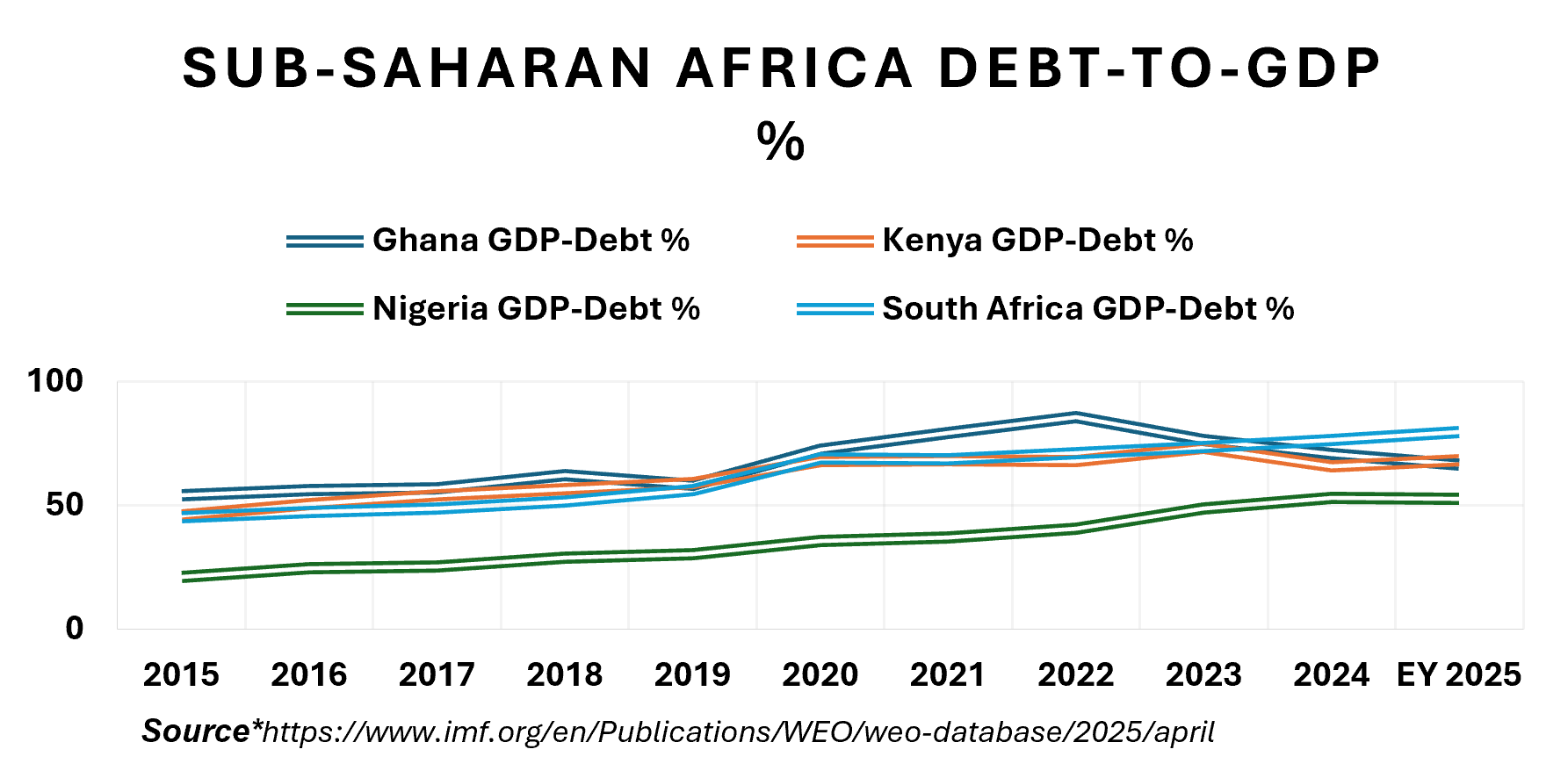

Debt Sustainability in Context

Nigeria’s debt-to-GDP ratio stood at approximately 39.4% as of Q1 2025, below the IMF’s 55% threshold for developing economies. However, debt-service-to-revenue remains a pressure point, with over 70% of government revenues consumed by interest payments in recent years. This raises investor concerns about fiscal headroom. Still, when compared to peer Sub-Saharan African economies, Nigeria’s debt stock appears relatively moderate:

What sets Nigeria apart is its substantial economic base and increasingly diversified revenue structure. In Q1 2025, Nigeria’s economy grew by 3.13% year-on-year, with the services sector expanding 4.33% and accounting for 57.15% of GDP . On the revenue front, tax collections surged in H1 2025, rising 43% year-on-year to N14.27 trillion, of which non-oil taxes alone increased 44.2% to N10.64 trillion. This non-oil revenue growth driven by tax reforms, better compliance, and expansion across mobile services, trade, and financial services, creates a stronger platform for debt servicing and helps lessen dependency on oil revenue. When paired with the shift toward concessional borrowing and targeted sectoral investment, these trends enhance the efficiency and sustainability of Nigeria’s debt profile, provided risks around execution remain managed.

Assessing Repayment Capacity

A small number of critical factors will shape Nigeria’s ability to meet obligations under its $21.5 billion financing plan. Oil production, the main source of FX and fiscal revenue, rose from 1.51 mbpd in June to about 1.78–1.80 mbpd in July, moving closer to the 2025 budget target of 2.06 mbpd. Brent prices, however, remain below the $75 assumption, trading in the mid- to high-$60s in August after peaking at $72 in July, with a recent dip to $65.8. Inflation eased to 22.22% in June from 22.97% in May but is still high enough to keep borrowing costs elevated.

Non-oil tax receipts have been robust, reaching ₦14.27 trillion in H1 2025 43% higher year-on-year and covering more than half the annual target helping to reduce reliance on oil revenues. Infrastructure delivery has been mixed, with visible progress on priority projects such as the Lagos–Calabar Coastal Highway, though most are still several years away from delivering their full economic and fiscal impact.

Structurally, expanding the use of concessional multilateral development bank (MDB) financing such as IBRD facilities with maturities of up to 35 years could ease annual debt-service pressures and create greater fiscal flexibility. The following scenario analysis examines how changes in these and other key drivers could alter Nigeria’s repayment capacity;

| Drivers | Best Case | Base Case | Worst Case | Scenario Insight |

|---|---|---|---|---|

| Oil Production (mbpd) | 1.90–2.06 mbpd (vs July 1.78–1.80); meets budget target on improved security/up time. | 1.65–1.85 Above June’s 1.51 but shy of target; moderate theft/outages persist. | ≤1.55 Reverts toward June lows on operational setbacks. | Higher output raises oil and FX inflows, easing DS/R. |

| Brent Price ($/bbl /Goldman Sachs 2026 focus) | $60 (+$4 upside —optimistic demand/supply risks) | $56 (Goldman Sachs forecast) | $50 (–$6 downside—recession/oversupply risk) | High prices boost revenue; in-line cover debt; low strain reserves, raise repayment risk |

| Inflation (YoY) | M19–20% Faster disinflation if policy holds. | 21–23% Slow glide-down matching recent prints. | ≥25% Renewed FX pass-through from weaker oil. | Lower inflation reduces borrowing costs; higher inflation erodes fiscal space. |

| Non-Oil Revenue (₦ tn) | ≥25.2 Meets FY target if H2 matches H1 pace | 23–25 Slightly under target, still strong y/y. | 21–23 Slows with weaker activity. | Strong non-oil revenue cuts oil reliance; weak performance raises vulnerability. |

| Debt Service / Revenue | Improves Lower DS/R on stronger oil/tax, easing rates. | Flat vs 2024–H1 2025 | Worsens Higher DS/R on weaker oil, higher costs. | Lower DS/R improves repayment capacity; higher DS/R signals fiscal strain. |

Data in the TABLE .2 above is sourced from : Goldman Sachs, U.S. Energy Information Administration (EIA), Reuters, Energy Now, Budget Office of the Federation, Organization of the Petroleum Exporting Countries (OPEC), National Bureau of Statistics (NBS), International Monetary Fund (IMF), The World Bank, Federal Ministry of Works & Housing, Federal Inland Revenue Service (FIRS), Debt Management Office (DMO), and the Infrastructure Concession Regulatory Commission (ICRC).

Conclusion

For foreign lenders, the outlook for Nigeria’s external debt servicing over the next 12–18 months will be shaped by macro factors and the timely delivery of priority infrastructure. Production has moved closer to budget levels and non-oil revenues are ahead of target, but inflation is still high and project timelines remain uneven. The question is whether current and planned projects are advancing quickly enough, and with the right priorities, to deliver the growth and revenue gains the government is counting on.

Repayment risk will depend as much on delivery performance as on broader economic conditions. Lenders can protect themselves by focusing on structure using long-term concessional funding, linking disbursements to clear milestones, and securing FX inflows for repayment. Those who align lending terms with these realities will be best positioned to manage risk and support a financing strategy that remains sustainable.

Kindly find the Report Below

Thanks for reading.