Fixed Income in Focus:

The market traded on a broadly bearish tone through the week, led by bond selling after the CBN bond issuance circular pointed to larger net issuance. Activity centred on the 2030s–2037s, where yields repriced higher by c. ▲41bps WoW despite intermittent retracement and the softer May CPI print. The move reflected a defensive risk tone, as supply concerns continued to outweigh the positive inflation surprise. In T-bills, focus was on the NTB auction, where supply was revised above the initial offer and the 364-day cleared at 17.34%, about 100bps above the previous level.

The repricing reset the short end higher, creating room for demand to re-emerge in secondary trading. Strong demand, reflected in a 2.08x BTC, supported interest in the newly issued 17-Jun bill, which traded below stop into the latter sessions. This underscored the split between defensive bonds and better-supported bills, while OMO activity remained subdued and liquidity closed robust at c. ₦3.98tn.

Nigerian Equities:

The ASI declined 3.59% WoW, extending the market’s pullback. Banking (-10.49%) led losses, followed by Insurance (-7.22%) and Industrials (-4.11%), while Oil & Gas (-1.06%) proved relatively resilient. The selloff was broad-based, with profit-taking and risk reduction across major sectors driving a sharp deterioration in market sentiment.

NTB Auction Result

| 91-day | 182-day | 364-day | |

| Sales (₦‘bn) | 129,320 | 70,169 | 1,291,443 |

| Stop Rates | 16.28% | 16.50% | 17.34% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 17.40 | 17.80 | (40) |

| May-33 | 17.40 | 17.80 | (40) |

| Feb-34 | 17.40 | 17.70 | (30) |

| Jan-35 | 17.50 | 17.95 | (45) |

| Apr-37 | 17.40 | 18.00 | (60) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 17-Jun-27 | 17.00 | 17.05 | 20.51 |

| 03-Apr-27 | 16.44 | 16.90 | 20.14 |

| 22-Jan-27 | 15.90 | 15.90 | 18.34 |

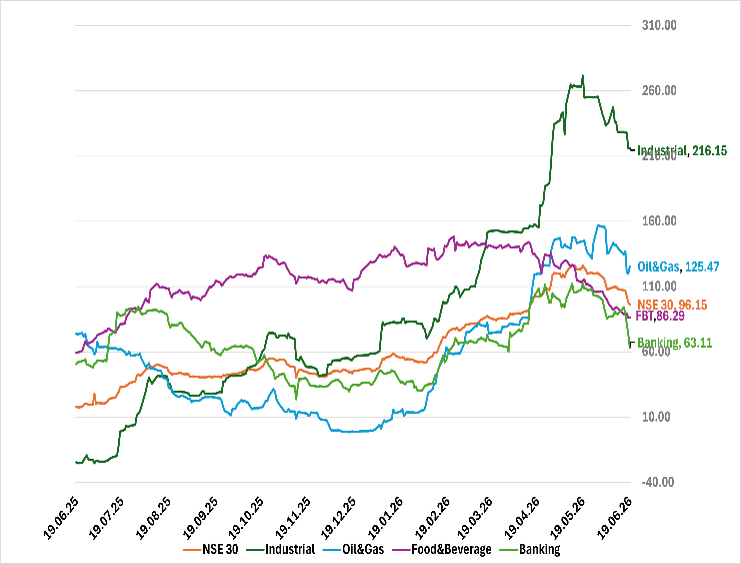

Indices Watch 1-Yr Performance %

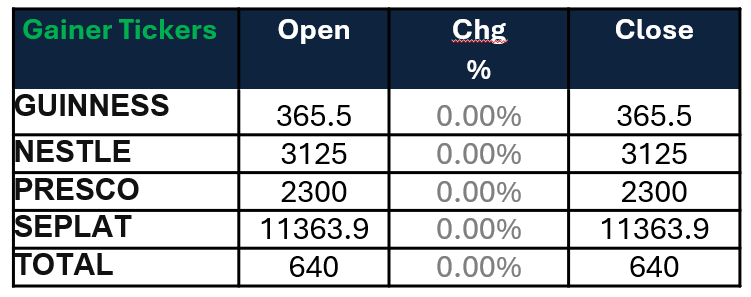

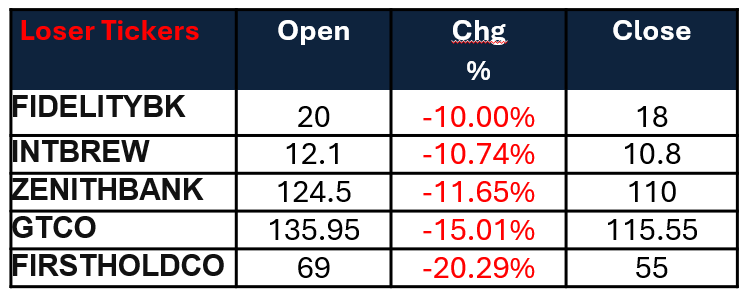

NSE 30 : Gainers and Losers

The Week Ahead…

The week is set against a scheduled FGN bond auction, with the DMO set to re-open ₦1.20tn across the 22.60% Jan-2035s and 16.25% Apr-2037s. This is supported by surplus system liquidity and expected inflows of c. ₦1.92tn, mainly from OMO maturities, FGN bond payments, and NTB maturities.

Activity is expected to hinge largely on the auction outcome, with sentiment skewed bearish given the size of supply, although robust liquidity may help support demand.For equities, following the sharp correction, we expect selective bargain hunting in fundamentally strong names, although sentiment may remain cautious in the near term phase.