Fixed Income in Focus:

The fixed income market traded for a shortened three-day week due to the Eid el-Kabir public holiday, with overall activity moderate and participation largely selective across the curve.The week opened with focus on the Q1 2026 GDP print, which came in stronger at 3.89% YoY, signaling sustained economic resilience.

In the bond market, sentiment was mildly bullish, with demand initially concentrated around the 2035s and 2037s before extending across the belly of the curve.NTB activity remained selective, with interest anchored around the Apr/May maturities, while the OMO space was shaped by the CBN auction across 11-, 39-, and 102-day tenors, which cleared with strong demand, particularly on the longer tenor at 8.63x bid-to-cover. Overall, the week was defined by holiday-thinned activity, selective participation, supportive liquidity conditions, and a mildly bullish tone across the curve.

Nigerian Equities:

The NGX ASI and Market Capitalization appreciated by 0.27% WoW to close at 250,385.47 points and ₦160.509 trillion respectively.Total turnover declined to 2.398 billion shares worth ₦111.480 billion in 241,313 deals, from 3.875 billion shares worth ₦161.757 billion in 334,745 deals the prior week, largely due to the public holiday.On the sector front, NGX Oil/Gas (+2.53%) and NGX Insurance (+1.41%) led the gainers, while NGX Banking (-2.43%) and NGX Consumer Goods (-2.04%) led the losers.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 17.05 | 17.05 | – |

| May-33 | 17.00 | 16.95 | 5 |

| Feb-34 | 17.00 | 17.00 | – |

| Jan-35 | 17.05 | 16.92 | 13 |

| Apr-37 | 17.03 | 16.95 | 8 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 20-May-27 | 16.03 | 15.85 | 18.73 |

| 22-Apr-27 | 15.85 | 15.80 | 18.40 |

| 18-Mar-27 | 16.25 | 16.25 | 18.67 |

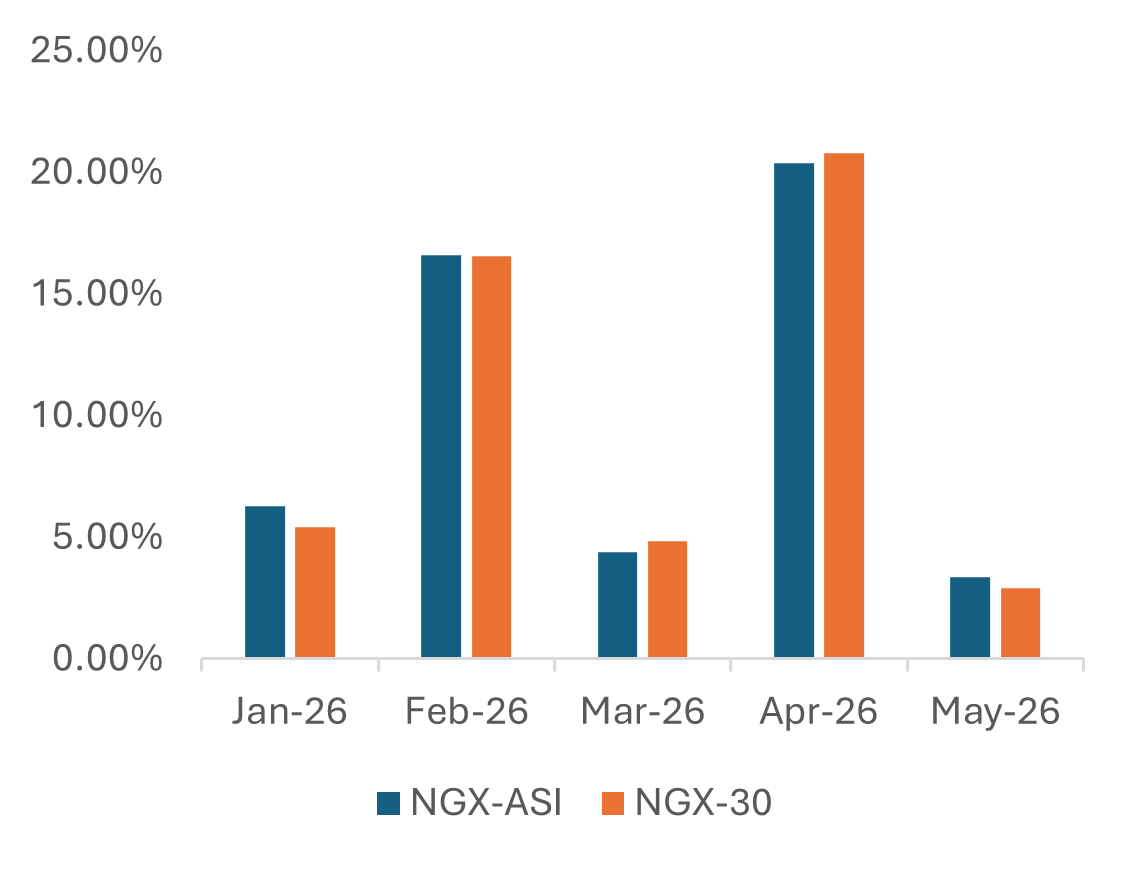

NGX-ASI vs NGX-30 Monthly Performance

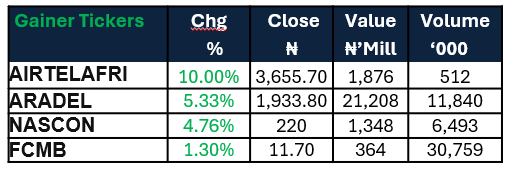

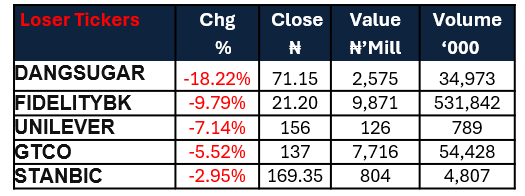

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens against a scheduled Treasury bills auction, with the DMO set to offer ₦700bn across tenors against c.₦465bn in maturities. Market direction will likely be shaped by the auction outcome, particularly given the net supply pressure. As such, we may see early profit-taking ahead of the mid-week auction, with broader activity expected to hinge on stop rates, subscription levels, and post-auction liquidity conditions.

On equities hand, as the market remains in a consolidation phase with mixed sentiment, we expect investors to continue taking profit in recently rallied stocks. With no major catalyst in sight, pockets of bargain hunting are beginning to emerge as investors seek positions in oversold stocks while anticipating the next catalyst.