Fixed Income in Focus:

The fixed income market traded with a broadly bearish tone over the week, shaped by the bond and OMO auctions as well as the 305th MPC decision, which printed unchanged across key policy parameters. At the bond auction, the 2035s and 2037s cleared at 17.00% and 17.04% respectively, setting the tone for secondary market repricing, especially across the mid-tenors, where the 2031s–2035s backed up through the week.

NTB activity remained selective, with demand concentrated at the long end, particularly the 20-May bill. In the OMO space, the late-week auction saw strong demand across both tenors, with the 33-day and 138-day bills clearing at 21.57% and 19.97% respectively, before secondary market activity turned mildly bullish into the close.

Overall, the week was defined by auction-led repricing, stable policy signals, selective participation, and softer liquidity into Friday.

Nigerian Equities:

The NGX All-Share Index fell 0.25% to close at 249,712.37 points, while market capitalization declined 0.23% to ₦160.077 trillion. Banking and Consumer Goods gained 1.11% and 0.24% respectively, while Insurance lost 1.77%. The decline was driven by profit-taking and portfolio rebalancing ahead of key market catalysts, particularly the listing of Dangote Refinery.

NTB Auction Result

| 91-day | 182-day | 364-day | |

| Sales (₦‘bn) | 64,466 | 78,589 | 683,289 |

| Stop Rates | 15.95% | 16.14% | 16.149% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.90 | 17.05 | (15) |

| May-33 | 16.90 | 17.00 | (10) |

| Feb-34 | 16.85 | 17.00 | (15) |

| Jan-35 | 16.85 | 17.05 | (20) |

| Apr-37 | 16.70 | 17.03 | (33) |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 20-May-27 | 15.90 | 16.03 | 19.05 |

| 22-Apr-27 | 15.80 | 15.85 | 18.53 |

| 08-Apr-27 | 16.00 | 15.80 | 18.33 |

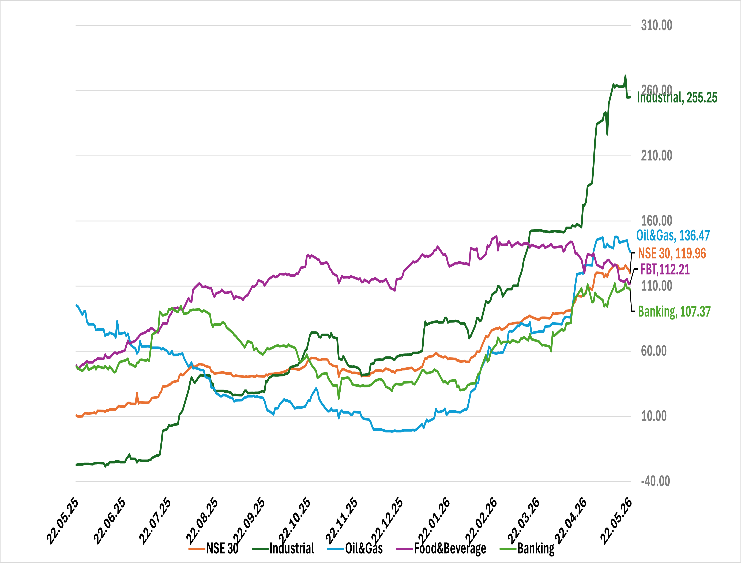

Indices Watch 1-Yr Performance %

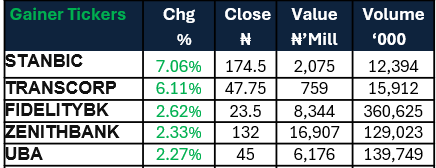

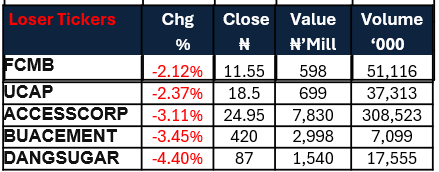

NSE 30 : Gainers and Losers

The Week Ahead…

The week opens with no scheduled macro events or primary market auctions, but with expected inflows of c.₦2.01tn, led by OMO maturities, alongside coupon inflows from the 19.75% May 2032s and 15.00% Nov 2028s. In the absence of fresh supply, the market could trade slightly bullish, supported by improved system liquidity. However, given the sizable OMO maturity, a CBN OMO auction is likely as the Bank may look to mop up excess liquidity.

In equities side, we expect trading volume to remain concentrated in Banking and Oil & Gas stocks as institutional investors gradually position ahead of key market catalysts, particularly the anticipated listing of Dangote Refinery.