Fixed Income in Focus:

The week opened on muted trading with system liquidity in surplus at ₦2.6tn as focus centered on the bond auction and early-week MPC print. The bond auction cleared bullish at 15.50–15.74% on a 3.37x cover across re-opened tenors, tightening a further c.45bps post-auction on surplus demand with execution at 15.10–15.20%. The MPC delivered a hawkish cut, prompting bonds to back up c.40bps into the close as easing expectations were re-calibrated. Treasury bills saw similar repricing following the early-week compression, with Feb (18/4) bills settling at 15.70%, backing up c.30bps ahead of anticipated supply. In OMO, the mid-week auction cleared on a 1.8x cover at 18.45–21.94%, closing firmer as liquidity remained ample at a ₦3.7tn.

Nigerian Equities:

The ASI declined 1.11% WoW to 192,826.78, reversing part of the prior week’s rally, Consumer Goods (-3.47%) led losses alongside Industrials (-0.69%). The MPC’s policy stance maintained tight monetary conditions which tempers aggressive equity positioning, particularly in rate-sensitive consumer names.

Bond Auction Result

| 17.95% Feb-2032s | 19.89% May- 2033s | 19.00% Feb- 2034s | |

| Sales (₦‘bn) | 188.14 | 208.63 | 127.51 |

| Marginal Rates | 15.74% | 15.74% | 15.50% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.00 | 15.75 | 25 |

| May-33 | 16.05 | 15.80 | 25 |

| Feb-34 | 16.05 | 15.60 | 45 |

| Jan-35 | 16.00 | 15.60 | 40 |

| Jun-53 | 14.10 | 14.00 | 10 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 18-Feb-27 | 15.65 | 15.70 | 18.52 |

| 04-Feb-27 | 15.40 | 15.70 | 18.39 |

| 19-Nov-26 | 15.60 | 15.85 | 17.89 |

Indices Watch 1-Yr Performance %

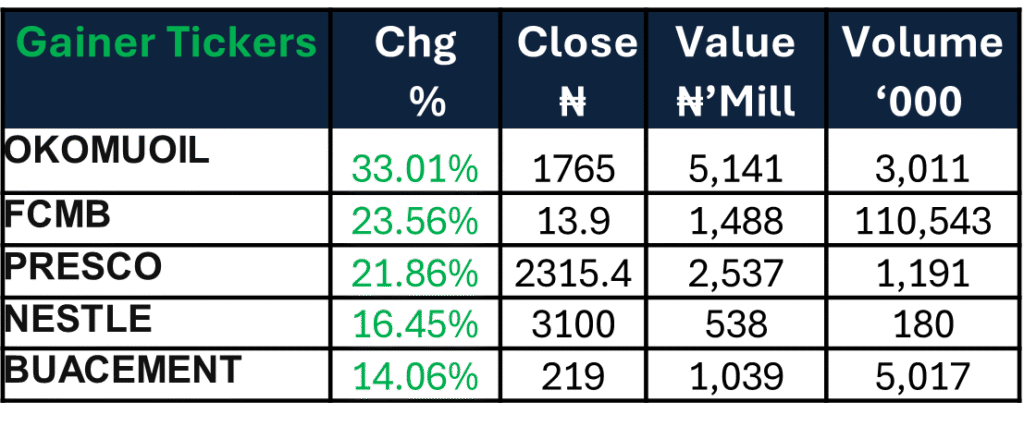

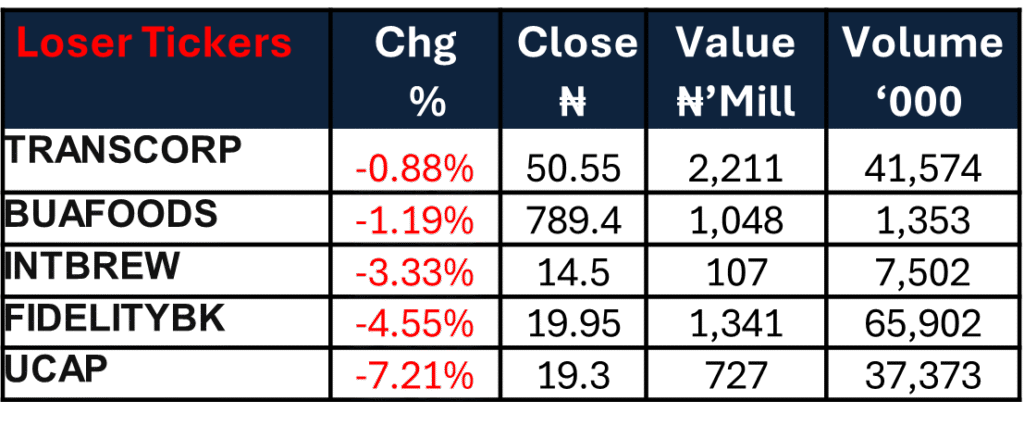

NSE 30 : Gainers and Losers

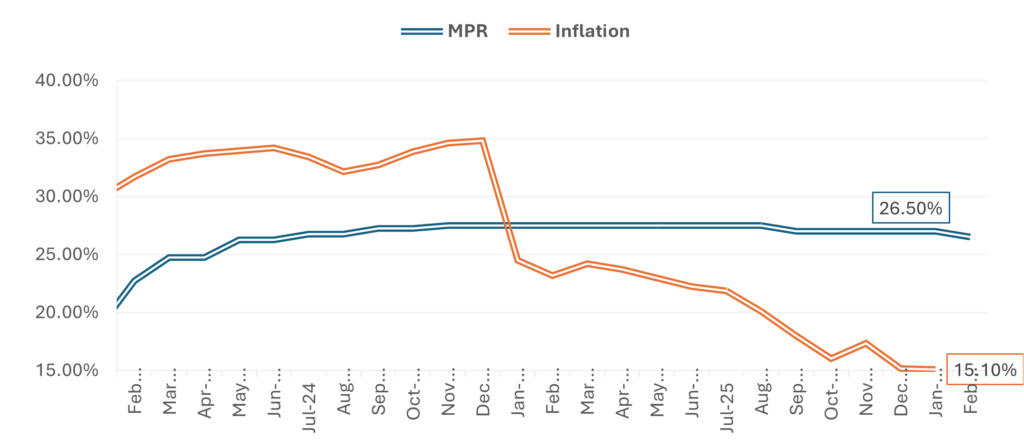

Monetary Policy Rate Expectation

N/B: Figures used in representing this data have been updated using the rebased CPI numbers

MPC Policy View:

At the 304th Monetary Policy Committee (MPC) Meeting held on February 23rd–24th, 2026, the Committee decided to reduce the Monetary Policy Rate (MPR) by 50 basis points to 26.50%. Other parameters were retained as follows: the Cash Reserve Ratio (CRR) for commercial banks at 45%, the CRR for merchant banks at 16%, the 75% CRR on non-TSA public sector deposits remained in place, the Liquidity Ratio at 30%, and the Asymmetric Corridor around the MPR held at +50/-450 basis points. Nigeria’s headline inflation continued its disinflation trend, easing to 15.10% in January 2026 from 15.15% in December 2025, extending its eleventh consecutive monthly decline and reinforcing expectations of further policy easing.

Markets entered the February 304th MPC meeting anticipating around a 100bps rate cut amid sustained softening inflation into early 2026, but the actual 50bps reduction fell short of those expectations, signaling a relatively cautious tone from the Committee. Having priced in a larger easing earlier, markets reacted with profit-taking following the announcement, with equities shedding value in the immediate aftermath as investors re-calibrated expectations for the pace and trajectory of monetary easing going forward.

The Week Ahead…

The week opens ahead of a scheduled FGN Treasury bills auction, with the DMO set to issue ₦1.05tn across tenors against c.₦799bn in maturing paper. Amid rising global tensions, we could see flight-to-safety flows away from emerging market assets, exerting pressure on the domestic space. Direction this week will likely hinge on the interplay between global risk sentiment and the outcome of the mid-week auction.