Fixed Income in Focus:

The week opened with net liquidity of ₦3.9tn, setting the stage for a bullish bond auction that drew broad-based demand across tenors, with a 2.5x cover. Post-auction, the bond market rallied, with reopened mid-tenors (5–10yr) executing around 16.55–16.80% by close. The Treasury Bill market remained firm, with the 21-Jan issue trading c.90bps lower week-on-week. Mid-week, the CBN conducted an OMO auction that drew strong participation (9.9x cover) on longer tenors (208- and 348-day), clearing at 17.20–25.00%. A second OMO the following day was also well bid (4.3x cover), with the long end (354-day) clearing at 17.25%. Post-auction, demand clustered in the 348/354-day bills (12- and 19-Jan OMO), trading 17.10–17.15% into the close.

Nigerian Equities:

The NGX ASI edged lower by 0.09% WoW to close at 165,370.40. Insurance led gains (+0.81%), while Banking underperformed (-0.63%), dragging overall market performance. Market activity reflected mild profit-taking in financial heavyweights. First Bank unaudited FY results highlighting significant impairment charges and governance concerns, likely to weigh on banking sentiment.

Bond Auction Result

| 18.50% Feb 2031 | 19.00% Feb 2034 | 22.60% Jan 2035 | |

| Sales (₦‘bn) | 398.19 | 576.33 | 570.16 |

| Stop Rates | 17.62% | 17.50% | 17.52% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-34 | 17.15 | 16.80 | 35 |

| Feb-31 | 17.20 | 16.70 | 50 |

| Jan-35 | 17.20 | 16.75 | 45 |

| May-33 | 17.30 | 16.65 | 65 |

| Jun-53 | 15.00 | 14.60 | 40 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 21-Jan-27 | 17.20 | 16.45 | 19.57 |

| 07-Jan-27 | 17.00 | 16.50 | 19.50 |

| 19-Nov-26 | 16.65 | 16.30 | 18.73 |

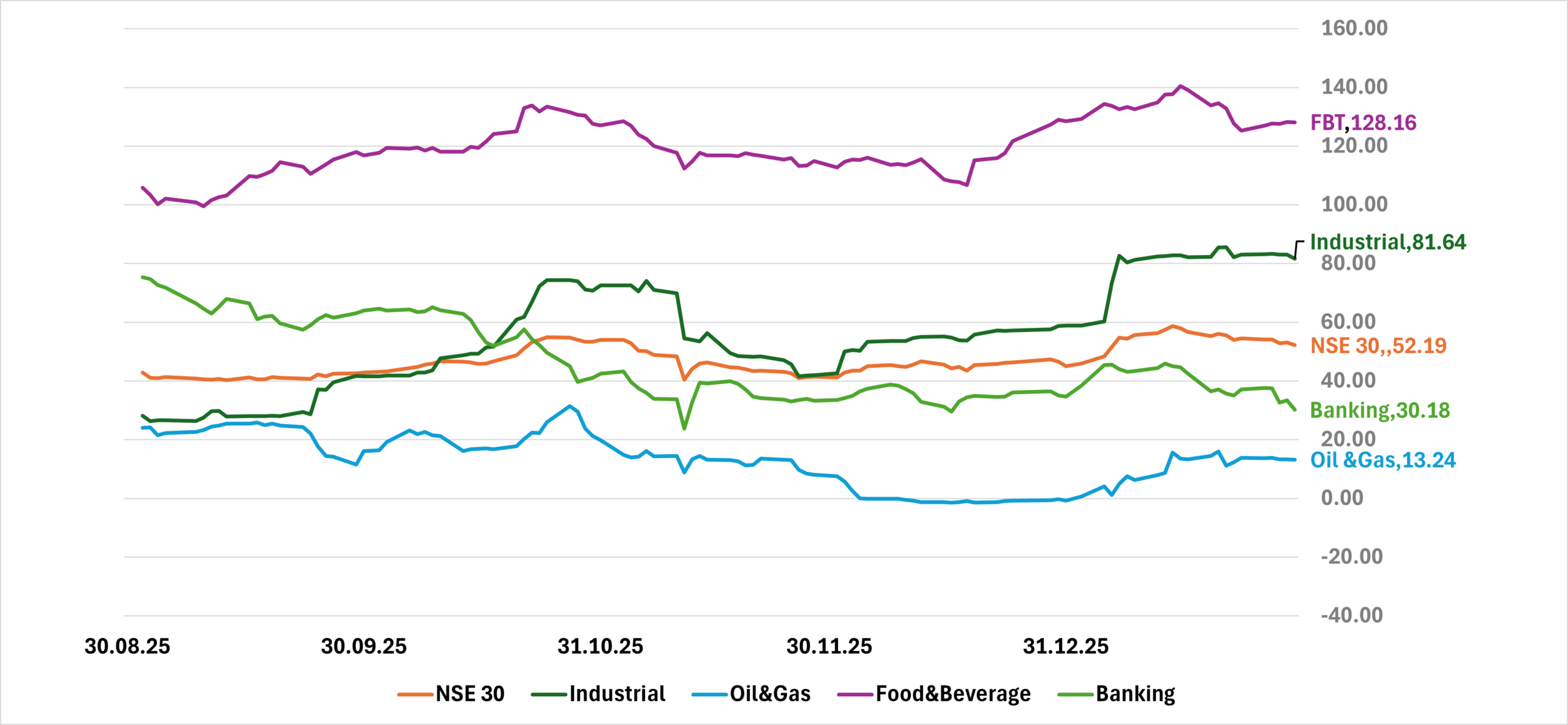

Indices Watch 1-Yr Performance %

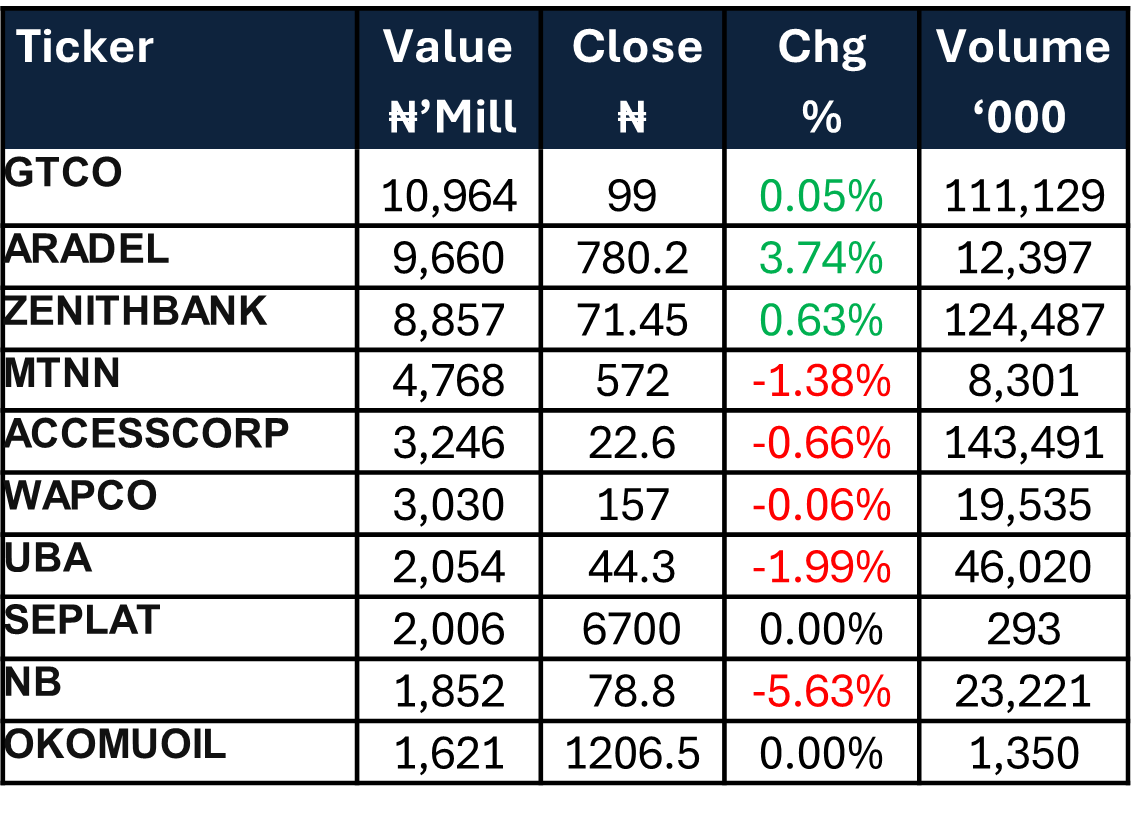

This Weeks Market Movers NGX

The Week Ahead…

The week is set against a scheduled FGN Treasury bill auction, where the DMO plans to issue ₦1.15tn across tenors against ₦668bn in bill maturities, implying a net supply overhang. We also expect an additional ₦402.9bn inflow from maturing OMO bills, which should provide incremental system liquidity and help cushion the supply pressure. With no key macroeconomic data in focus, market direction is likely to be driven primarily by the auction outcome.

We expect demand to remain resilient, supporting a bullish print that could extend into secondary market trading. Near-term relief is possible as some investors lock in gains ahead of the next auction.