Fixed Income in Focus:

Markets opened the week with system liquidity firm at ₦596bn and bullish activity evident across the curve. The Treasury bills space saw muted participation ahead of the mid-week auction, which cleared bullish (-137bps vs. previous auction) with heavy demand on the 364-day bill (5.5x cover). Post-auction unmet demand spilled into the secondary market, with the 04-Feb bill trading 143bps below the auction print, while mild profit-taking later pulled yields back by c.50bps by close. The bond market opened with evenly distributed demand and then turned increasingly bullish, driving yields lower by c.30bps, led by the mid-to-long end, before meeting resistance into the close, while OMO bills (12-Jan/19-Jan) traded 16.45%–16.65%. Liquidity remained firm, closing at ₦2.34tn.

Nigerian Equities:

NGX ASI advanced 3.84% WoW to 171,727.49,Oil & Gas led gains (+10.88%), followed by Industrials (+4.36%), while Insurance (-2.33%) lagged. The rally was flow-led into heavyweights, with SEPLAT, DANGCEM, MTNN and ACCESSCORP driving price action in line with sector leadership. We expect follow-through to stay concentrated in the same liquid large-cap names, while Insurance lags.

NTB Auction Result

| 91 Days | 182 Days | 364 Days | |

| Sales (₦‘bn) | 63.214 | 80.610 | 808.784 |

| Stop Rates | 15.84% | 16.65% | 16.987% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Feb-31 | 16.70 | 16.40 | 30 |

| May-33 | 16.65 | 16.65 | – |

| Feb-34 | 16.80 | 16.60 | 20 |

| Jan-35 | 16.75 | 16.65 | 10 |

| Jun-53 | 14.60 | 14.40 | 20 |

| NTB | Open | Close | Effective Yield |

| % | % | % | |

| 04-Feb-27 | 16.20 | 16.05 | 19.08 |

| 21-Jan-27 | 16.25 | 16.00 | 18.87 |

| 07-Jan-27 | 16.20 | 16.05 | 18.80 |

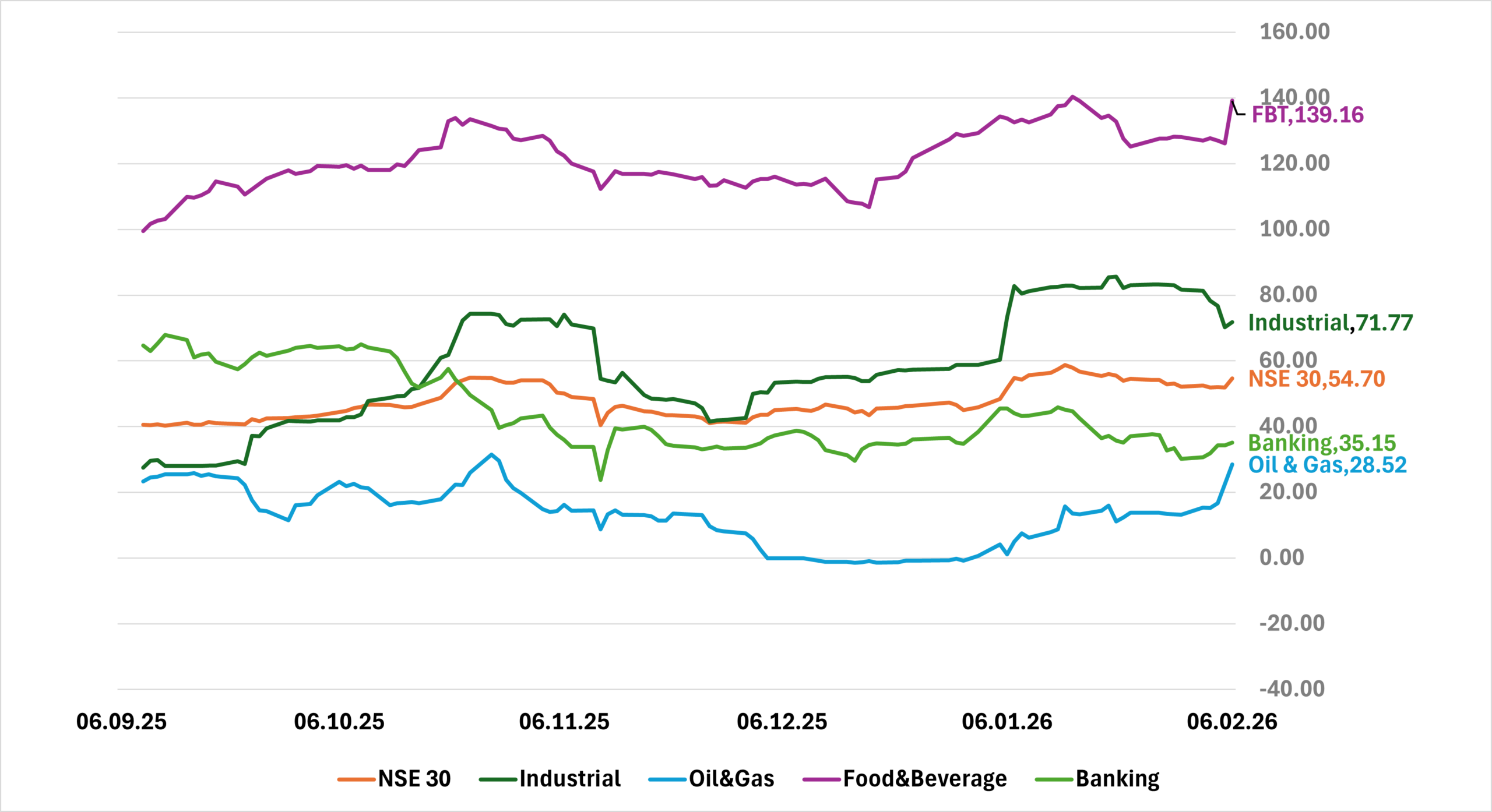

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

The market opens with no key macroeconomic data releases and no scheduled auctions, leaving liquidity as the main driver. We anticipate a ₦668bn inflow from maturing OMO bills, which should keep system liquidity supportive early in the week. Given the size of the inflow and the current liquidity position, an early- to mid-week CBN OMO auction remains likely as policymakers may seek to re-absorb excess liquidity.

Secondary market trading will therefore be shaped by the timing and outcome of any OMO issuance, alongside sustained demand for mid-to-long tenor bonds and the 364-day bill.