Fixed Income in Focus:

The market opened in anticipation of the FGN bond auction, which cleared with aggressive demand c.4.9x cover and pushed marginal rates 16-35 bps below the previous auction. Secondary trading turned mixed thereafter, an early bullish tone in the mid-tenors (’32s/’33s) faded into a late-week bearish pullback as participants tested higher yield levels. In bills, activity centered on the 1-year 22-Oct NTB, which executed around 15.70% early before tightening to c.15.50% into the close. OMO trading showed a similar pattern, led by the 23-Jun and 30-Jun papers in a 18.95%–19.05% range, while the CBN’s late-week OMO sale saw muted interest given the short tenors on offer. Despite the robust activity liquidity remained ample at c. ₦2.4tn surplus.

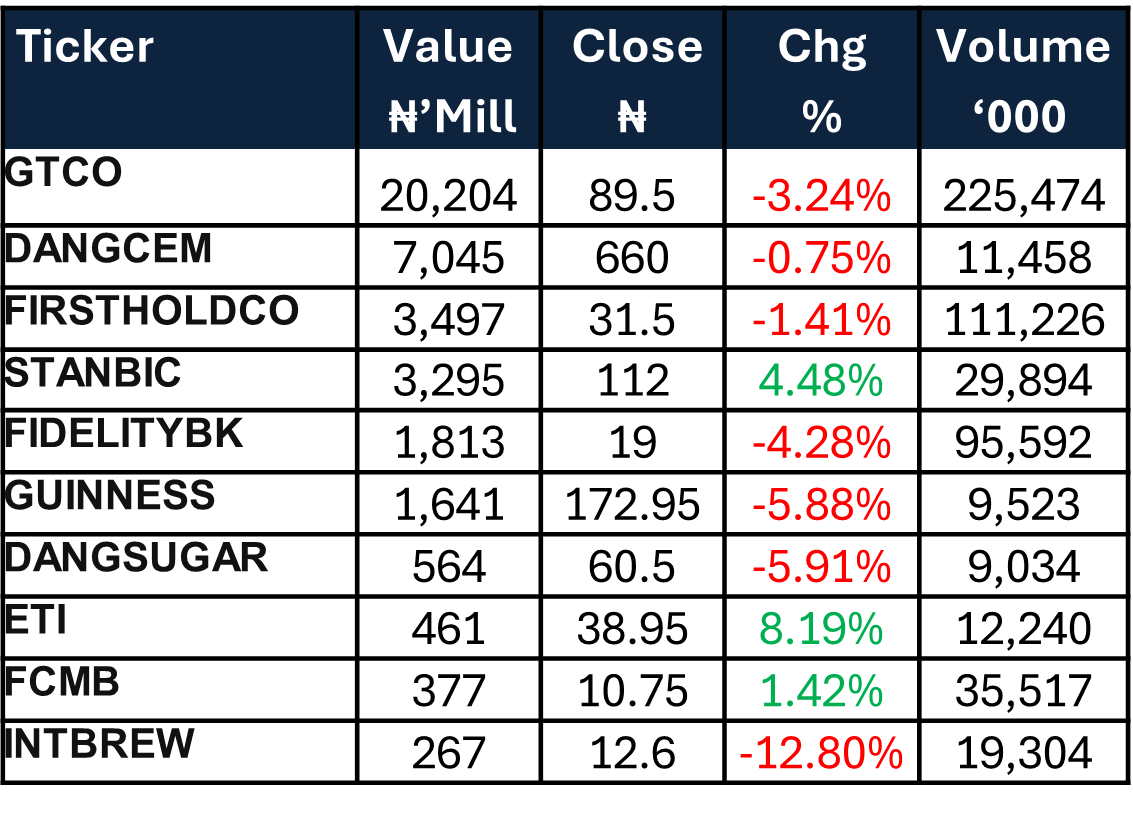

Nigerian Equities:

The ASI slipped 0.98% to close at 154,126.46, halting its recent winning streak with Insurance at 2.41% and Oil & Gas at 1.87% leading gains, while Banking -1.15% dragged sentiment. Trading remained concentrated in financials, (89% of total turnover), while industrials moderated after October’s rally. Month-to-date, the market gained 8%, We expect sentiment to stay cautious as more Q3 results are released.

NTB Auction Result

| 17.945% 2030 | 17.95% 2032 | |

| Sales (₦‘bn) | 87.798 | 225.973 |

| Marginal Rates | 15.832% | 15.85% |

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 16.15 | 15.90 | 25 |

| Feb-31 | 16.05 | 15.70 | 35 |

| Jun-32 | 16.10 | 15.75 | 35 |

| May-33 | 16.00 | 15.65 | 35 |

| Jun-53 | 15.00 | 14.80 | 20 |

| NTB | Bid | Ask | Effective Yield |

| % | % | % | |

| 22-Oct-26 | 15.70 | 15.50 | 18.24 |

| 08-Oct-26 | 15.50 | 15.65 | 18.25 |

| 19-Feb-26 | 16.15 | 16.10 | 16.91 |

Indices Watch 1-Yr Performance %

This Weeks Market Movers NGX

The Week Ahead…

The week opens ahead of the scheduled Treasury Bill auction, with the DMO set to issue ₦650 billion across tenors against about ₦662 billion in maturing bills mid-week, alongside an additional ₦1.4 trillion inflow from OMO maturities.

With no major domestic data on deck, activity should center on the auction and broader global risk sentiment. Given the recent global backdrop and the U.S. President’s statement to the Nigerian government, we expect a turbulent market open, with risks of FX pressure and caution from Foreign portfolio investors could skew markets slightly bearish, while we await clearer policy guidance.