Fixed Income in Focus:

The market opened the week steady, with demand concentrated on the mid-to-long segment of the curve. The Treasury Bills market traded on a subdued tone, as the last issued 364-day bill held steady at a range 17.15 -17.25% throughout the week. The bond market began bullish, with strong demand for the 2029s, 2031s, 2032s, and 2033s, supported by ample liquidity and early positioning ahead of policy news. Toward the end of the week, profit-taking set in, pushing mid-tenor yields slightly higher and narrowing spreads from the week’s open. The OMO segment also saw robust activity, with the 17 March bill opening mid-week at 21.60% before rallying 170bps to close at 19.90%. Liquidity conditions remained firm, aided by mid-week inflows, and closed the week at around ₦2tn.

Nigerian Equities:

The ASI gained 1.13% to close at 140,545.69, halting a four-week decline , performance was broadly positive, led by Insurance and Oil & Gas with, 2.45% and 2.38% respectfully, alongside Banking at 1.68%. Sentiment was lifted by renewed interest in large cap stocks and regulatory-driven gains in select financial and insurance names. We expect flows to remain selective, with positioning focused on liquid financials and energy counters.

FI Weekly Snapshot

| FGN Bond | Open (Yield) | Close (Yield) | Chg WoW |

| % | % | (Bps) | |

| Apr-29 | 17.40 | 16.60 | 80 |

| Feb-31 | 17.25 | 16.68 | 57 |

| May-33 | 17.30 | 16.70 | 60 |

| Jan-35 | 17.08 | 16.65 | 43 |

| Jun-53 | 15.83 | 16.00 | (17) |

| NTB’s & OMO | Bid | Ask | Effective Yield |

| % | % | % | |

| 03-Sep-26 | 17.40 | 17.20 | 20.66 |

| 25-Dec-25 | 17.50 | 17.15 | 18.02 |

| 17-Mar-26 | 21.60 | 19.90 | 22.13 |

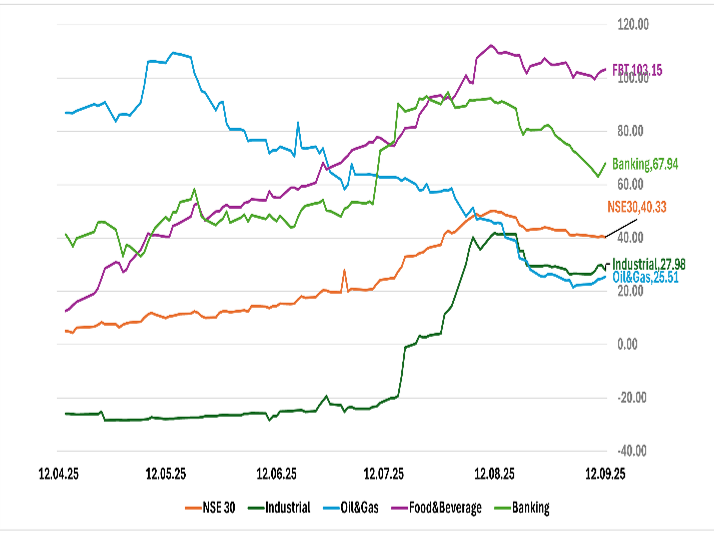

Indices Watch 1-Yr Performance %

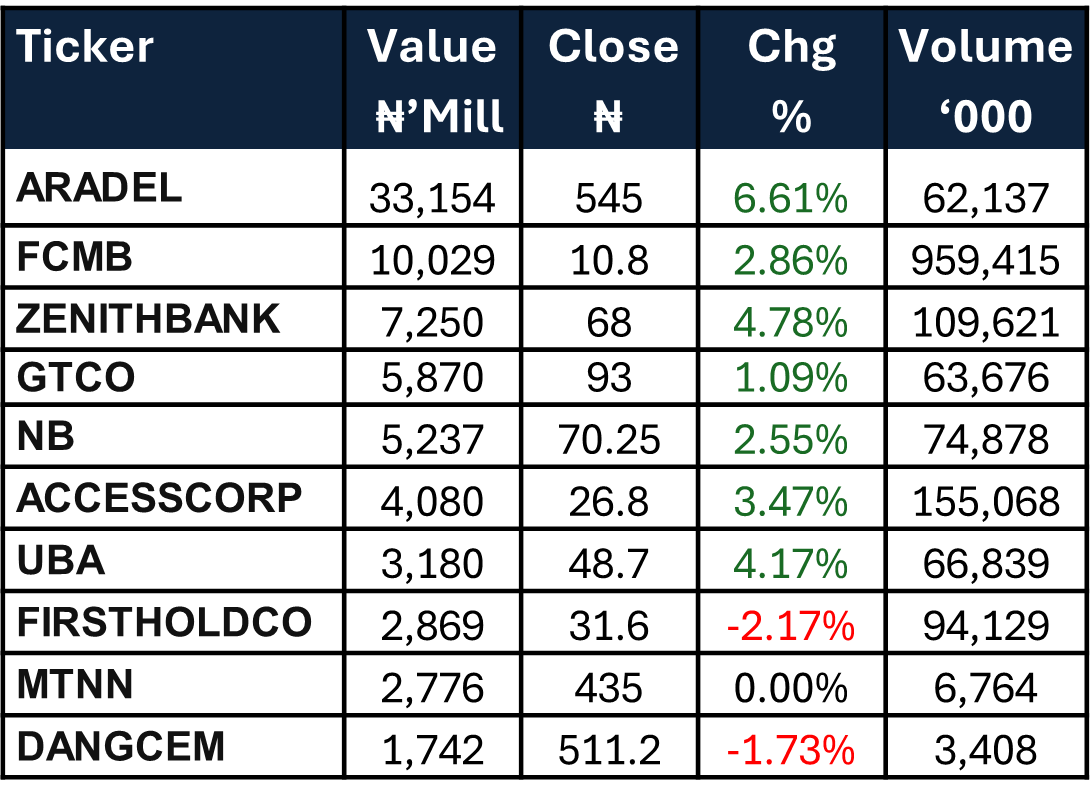

This Weeks Market Movers NGX

The Week Ahead…

The week opens with key macro releases, the Q2 GDP report and the August CPI print alongside a scheduled NTB auction, where the DMO, on behalf of the FGN, is set to issue ₦290bn against ₦78bn in maturities. Liquidity will be further supported by early-week OMO maturities and mid-week coupon payments on the FGN 17-Mar-2027 and FGN 18-Mar-2036 bonds, bringing total expected inflows to about ₦425bn.

Market focus will be on the macro data to guide positioning ahead of the mid-week auction, where FGN’s financing needs could prompt an oversell, supported by ample liquidity.